A term-life insurance plan is the single most important protection instrument in most salaried Indian households, and yet it is also the product where the largest mistakes are made and the largest claim rejections originate. The right policy at the right sum assured at the right premium, bought with full and honest disclosure, becomes a Rs.1,00,00,000+ (1 crore plus) financial safety net for the family that costs Rs.10,000 to Rs.25,000 a year. The wrong policy bought hurriedly with incomplete disclosure can fail the family at the moment they need it most. A disciplined term insurance buying checklist 2026 walks the buyer through 12 verifications in a defined order, each of which prevents a known class of problem.

This guide lays out the 12 checks in order, explains the common disclosure errors that trigger claim rejections, and covers the specific handling for smokers, NRIs, and buyers with pre-existing conditions. The framework applies to individual term-life policies in India under IRDAI regulation.

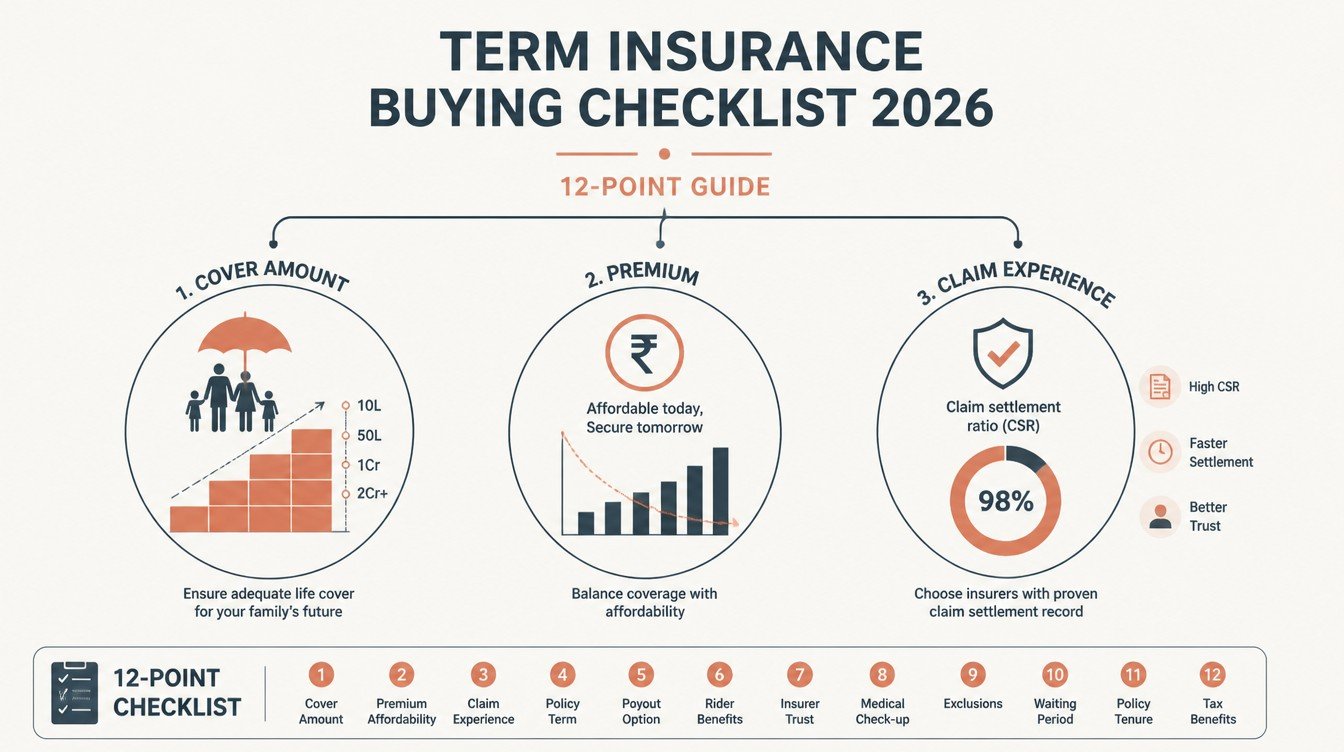

The 12-Point Checklist: Sum Assured and Term First

The order of the 12 checks matters because each builds on the previous one. The first four checks settle the sum assured, the term, the payment structure, and the basic claim-ratio screen, before any product-level comparison begins.

Check 1: Compute the right sum assured

The first step is to calculate the right sum assured for the household, not to compare policies. A common rule of thumb is 10 to 15 times annual gross income for an earning adult with dependents, adjusted for existing assets and outstanding liabilities. For a Rs.18,00,000 (18 lakh) earner with a Rs.40,00,000 (40 lakh) home loan, a sum assured of Rs.2,50,00,000 to Rs.3,00,00,000 (2.5 to 3 crore) is a reasonable starting point. The number drives every subsequent comparison.

Check 2: Choose the right policy term

The policy term should extend at least to the earning years’ end plus a buffer. A 35-year-old expecting to retire at 60 should pick a policy term of at least 25 years, ideally 30. Shorter terms produce a coverage gap in the late earning years when the household’s dependence on the income may still be high. Longer terms produce small premium increments and are usually better value.

Check 3: Pick the right premium-payment structure

The two main options are regular premium (paid each year through the policy term) and limited premium (paid for a defined shorter period like 10 or 15 years, with the policy continuing for the full term). Limited premium produces a higher annual outflow but a lower lifetime premium total. For households with strong current income but uncertain long-term income, limited premium provides predictable closure of the premium obligation.

Check 4: Compare claim-settlement ratios

The claim-settlement ratio (CSR) is the percentage of claims an insurer settles relative to total claims received in a year. IRDAI publishes annual CSR data for all life insurers. Insurers with CSRs consistently above the industry median across the last 3 to 5 years are structurally preferable to those with lower or more volatile ratios. The CSR is necessary but not sufficient; combine it with the next check.

Claim Ratios and Underwriting Disclosure

Checks 5 to 8 move from the macro shape of the policy to the underwriting and the rider menu. These are where the actual product-level comparison happens.

Check 5: Compare claim-amount-settlement ratios

The claim-amount-settlement ratio measures the amount settled as a percentage of total claims by amount, not just by count. This metric reveals whether insurers are paying out the small claims fully but contesting the large ones, or whether they are settling proportionately across claim sizes. An insurer with a high claim-count CSR but a meaningfully lower claim-amount ratio is showing a structural pattern that the buyer should weigh.

Check 6: Read the medical-disclosure requirements

Every term-insurance proposal requires medical and lifestyle disclosure. The proposal form lists the questions on past hospitalisations, diagnosed conditions, ongoing medications, family history of certain diseases, alcohol consumption, tobacco use, and certain occupations. Read each question carefully and answer each one honestly. The proposal form is the foundation of the contract.

Check 7: Plan for the medical underwriting step

For higher sum-assured policies (typically above Rs.50,00,000 to Rs.1,00,00,000), insurers usually require a medical examination at the proposal stage: blood tests, urine tests, ECG, sometimes a treadmill test, and a physical examination. The exam is conducted at home or at a designated diagnostic centre, paid for by the insurer. Cooperate fully; the results form part of the underwriting basis and become part of the contract record.

Riders and Their Role in the Stack

Riders are add-on covers that extend the basic term policy. Picking the right two and skipping the rest produces the best premium-to-protection ratio.

Check 8: Choose the right riders carefully

Common term-insurance riders include accidental death benefit, critical illness cover, permanent disability cover, and waiver of premium on disability. Riders increase the premium incrementally. The two most useful for typical Indian households are critical illness (which provides a lumpsum on diagnosis of specified critical illnesses) and waiver of premium on permanent disability. Accidental-death riders are often less valuable because the underlying term cover already pays on accidental death.

Nominee, Free-Look, Payout, and Documentation

The last four checks cover the operational layer that determines whether the policy actually works for the family when it is needed.

Check 9: Verify nominee details carefully

The nominee is the person who receives the policy proceeds on the insured’s death. The nominee should be a close family member (spouse, parent, child) and the relationship and bank-account details should be accurate. For minor nominees, an appointee is also required. The nominee designation is one of the most consequential 30 seconds in the entire policy application; verify it twice before submission.

Check 10: Understand the free-look period

IRDAI rules give the policyholder a free-look period of 15 days (or 30 days for policies sourced through distance marketing) from policy issuance to review the terms and cancel for a refund of premium net of certain charges. Read the policy document carefully during the free-look window and verify that what was promised at the proposal stage matches what is in the bond. Cancel within the free-look if there is a material discrepancy.

Check 11: Plan the policy-payout structure

Many insurers offer the payout in lumpsum, monthly income, or a hybrid (part lumpsum, part monthly income for a defined period). The right structure depends on the family’s financial sophistication. For families that have a competent financial planner or executor, lumpsum is often the cleanest. For families without strong financial-management capability, a structured monthly-income payout reduces the risk of the lumpsum being mismanaged.

Check 12: Document the policy and inform the family

The final check is the most mundane and the most missed. The policy document, the proposal form copy, the medical-examination report, and the receipt should all be filed in one place known to the spouse or nominee. The nominee should be told the insurer’s name and the policy number. A policy that the family cannot find when it is needed is no different from a policy that does not exist.

Common Disclosure Errors That Trigger Claim Rejections

The vast majority of contested term-insurance claims in India trace back to a small set of disclosure errors at the proposal stage.

Tobacco use non-disclosure

The single most common disclosure error is non-disclosure of tobacco or smoking use. Smoker premium rates are typically 1.5 to 2 times non-smoker rates for the same age and sum assured. The temptation to declare non-smoker for the lower premium is strong and consistently leads to claim rejection if death is shown to be tobacco-related and the autopsy or medical history flags the use. Declare every form of tobacco use (cigarettes, beedis, chewable tobacco, gutka, vaping) accurately.

Alcohol consumption misrepresentation

Excessive alcohol consumption is another commonly under-disclosed category. The proposal form usually asks about frequency and quantity. Honest answers may lead to a small loading or specific exclusion; dishonest answers can lead to repudiation on liver-disease or alcohol-related death claims.

Diagnosed conditions hidden

Hypertension, diabetes, hyperlipidaemia, hypothyroidism, asthma, and similar lifestyle conditions are sometimes hidden because the proposer believes they are “minor” or “well-controlled”. Insurers price these into the premium when disclosed; they reject the claim when undisclosed and later linked to the cause of death. Disclose every diagnosed condition with the year of diagnosis and current treatment.

Income misrepresentation

Some buyers inflate income at the proposal stage to qualify for a higher sum assured. Insurers cross-check income against Form 16, ITR documents, and salary slips. Inflated income leads either to policy issuance at a lower sum assured than requested, to specific exclusions, or to claim issues later. Use the actual documented income.

Family medical history

The proposal form usually asks about family history of certain diseases (cancer, diabetes, heart disease, mental illness) in immediate relatives. Hiding family history that is later established can attract repudiation arguments. Disclose what is asked, honestly.

The five-question quick test before signing

A final disclosure self-check before submitting any proposal runs through five questions.

- Have I disclosed every form of tobacco use, even occasional?

- Have I disclosed alcohol consumption frequency and quantity honestly?

- Have I listed every diagnosed condition with year of diagnosis and current treatment?

- Does the income figure on the form match the latest Form 16 or ITR?

- Have I answered the family-medical-history questions accurately for all immediate relatives?

Handling Special Cases: Smoker, NRI, Pre-Existing Conditions

Three buyer categories deserve specific handling within the 12-point framework.

The smoker buyer

Smokers should disclose tobacco use upfront, accept the higher premium (typically 1.5 to 2 times non-smoker rates), and look at “smoker” or “tobacco user” specific products from major insurers. Most insurers re-classify the buyer as non-smoker after a defined period of cessation (often 12 to 24 months of declared abstinence, sometimes with a fresh medical test). Reclassification produces material premium reduction at renewal.

The NRI buyer

NRIs (Non-Resident Indians) can buy Indian term-life insurance subject to specific KYC requirements and underwriting considerations. The proposal can usually be filed online during a visit to India or remotely with video-medical exam. Premium can be paid from an NRE or NRO account. Disclosure of country of residence, occupation, and any country-of-residence health checks is important. NRIs returning to India should inform the insurer of the change of residency at the appropriate time.

The buyer with pre-existing conditions

Buyers with diagnosed pre-existing conditions (diabetes, hypertension, post-cardiac event, post-cancer treatment) can usually still buy term insurance, with one of three outcomes: standard premium with no special treatment, premium loading proportionate to the condition, or specific exclusions (e.g., death from the disclosed condition excluded for a defined period). Reading and accepting the exact wording of any loading or exclusion at the proposal stage is essential.

The combined approach for complex cases

For buyers who fall into more than one special category (a smoker NRI with diagnosed hypertension, for example), working with a licensed broker who specialises in life insurance often produces better outcomes than applying directly. The broker can pre-qualify the case with multiple insurers and identify which one is likely to underwrite favourably, reducing the risk of policy rejection that itself attaches to the buyer’s record.

Putting It All Together: The Premium-Comparison Table

The table below summarises the dimensions to compare across term-insurance products. Actual numbers vary by insurer, age, sum assured, and health status; the buyer should request quotes from at least three insurers using the same inputs.

| Dimension | What to compare | What “good” looks like |

|---|---|---|

| Annual premium | Same sum assured, term, payment structure across insurers | Lowest premium consistent with strong CSR |

| Claim-settlement ratio (count) | 3-year average from IRDAI data | Above industry median, ideally 95 percent or higher |

| Claim-amount settlement ratio | 3-year average if disclosed | In line with the count-based CSR |

| Policy term flexibility | Maximum term offered, options for limited-pay | Up to age 80 to 85 if available; flexible pay periods |

| Riders available | Critical illness, accidental death, waiver on disability | Critical illness and waiver of premium on disability |

| Medical exam requirement | For the proposed sum assured and age | Comprehensive exam at insurer’s cost |

| Policy revival window | If a premium is missed, how long is revival possible | At least 2 to 5 years, with medical re-underwriting as needed |

| Free-look period | Days from issuance for cancellation | 15 days (or 30 days for distance marketing) |

The comparison-to-decision flow

Once the comparison table is populated for three insurers, the decision usually narrows to one or two finalists. The deciding factor between two equally strong choices is often the medical underwriting experience (which insurer responded faster, which one offered the cleanest terms after the medical exam, which one’s customer service felt more reliable). Pricing differences in the last 5 to 10 percent are not worth the risk of a less reliable claim experience.

What not to optimise for

Do not optimise for the lowest possible premium at the cost of CSR. Do not buy the cheapest policy from an insurer with low claim ratios because the household never expects to claim. The 1 in 1,000 scenario the policy exists for is exactly the moment when CSR matters most.

FAQ

How much sum assured do I actually need for my family?

A common rule of thumb is 10 to 15 times annual gross income for an earning adult with dependents, adjusted for any large existing assets (which reduce the need) and large outstanding liabilities like a home loan (which increase the need). For a household with multiple earners, each earning member needs their own term policy sized to replace their income. The right number is the amount that allows the family to maintain its current standard of living for the remaining number of earning years, after clearing all outstanding loans.

Is the cheapest term plan always the best?

No. The headline premium is one of several factors; the claim-settlement ratio, the insurer’s reputation, the policy term flexibility, the rider menu, and the claim process all matter. A plan that is 10 percent cheaper but has a materially lower CSR is a worse buy. Compare on the combined picture, not just the premium.

Should I declare every illness I have ever had?

Declare everything the proposal form asks about, completely and accurately. The form typically asks about hospitalisations, diagnosed conditions, ongoing medications, and surgical history, often with a look-back window of 5 to 10 years. Disclose every item in the look-back period. For older issues that the form does not specifically ask about, follow the spirit of the form: disclose anything material that could be considered relevant. The default rule is over-disclose rather than under-disclose.

What happens if my insurer asks for a medical exam?

Cooperate fully. The exam is at the insurer’s cost and is conducted by an authorised diagnostic vendor. Results form part of the contract record. If the exam reveals a previously undiagnosed condition (say, a borderline hypertension or hyperlipidaemia not previously known), the insurer may load the premium, exclude the specific condition, or in rare cases decline the policy. The disclosure and the exam are aligned with the principle of utmost good faith that governs insurance contracts.

Can I increase the sum assured later if my income grows?

Term-insurance sum assured cannot be increased on the same policy after issuance. The standard practice is to buy an additional term policy when the household income or liability profile grows materially. Buying in tranches (a first policy of Rs.1,00,00,000 at age 28, a second policy of Rs.1,50,00,000 at age 35 after marriage, a third policy of Rs.50,00,000 at age 40 after a home purchase) is a common Indian household strategy and is often cleaner than waiting and buying a single very large policy later.

Related guides on this topic are coming to learnfinedge.com soon.