The Union Budget 2026 formally introduced a staggered ITR filing calendar for FY 2025-26, with different due dates for salaried individuals, non-audit business filers, audit cases and transfer pricing cases. For salaried tax-resident Indians, that change matters more than the headlines suggest, because each missed window translates directly into Section 234F late fees, Section 234A interest and, in worst cases, a forced detour through the ITR-U updated-return route. The itr filing fy 2025-26 ay 2026-27 calendar is no longer a single July deadline. It is a sequence of four staggered dates, plus a belated cutoff in December and an ITR-U safety net that stretches to 31 March 2031.

This pillar guide walks through every deadline that applies to FY 2025-26 income, the documents that should be ready before the e-filing portal opens up, the worked penalty math for missed returns, and a clean filing checklist for salaried filers. Every section anchors back to the dates announced by the Income Tax Department and Ministry of Finance and stays cautious where official notifications are still pending.

Why the itr filing fy 2025-26 ay 2026-27 calendar changed

For more than two decades, 31 July was the single most cited tax date in India. Budget 2026 broke that convention by spacing out due dates based on the complexity of the return.

The shift from single deadline to staggered windows

The intent behind the change is simple. Salaried filers with TDS-driven returns are usually ready first, because Form 16 and AIS data settle by June. Audit cases are ready last, because statutory audits typically conclude in late September. A single 31 July deadline forced every taxpayer category into the same processing peak, leading to portal congestion and late-night fixes.

Categories defined by ITR form, not by income

The category that decides the deadline is the ITR form, not the income amount. A salaried filer with Rs.40,00,000 (40 lakh) of income still uses ITR-1 or ITR-2 and lands on the July 31 schedule. A self-employed consultant with Rs.6,00,000 of income who files ITR-3 lands on the August 31 or October 31 schedule depending on audit applicability.

Where to confirm your own deadline

The safest place to confirm the deadline is the e-filing portal at incometax.gov.in, which now shows the applicable due date inside the pre-filled return summary. The CBDT also issues advisories closer to the season, and major outlets like ClearTax mirror those advisories with worked examples.

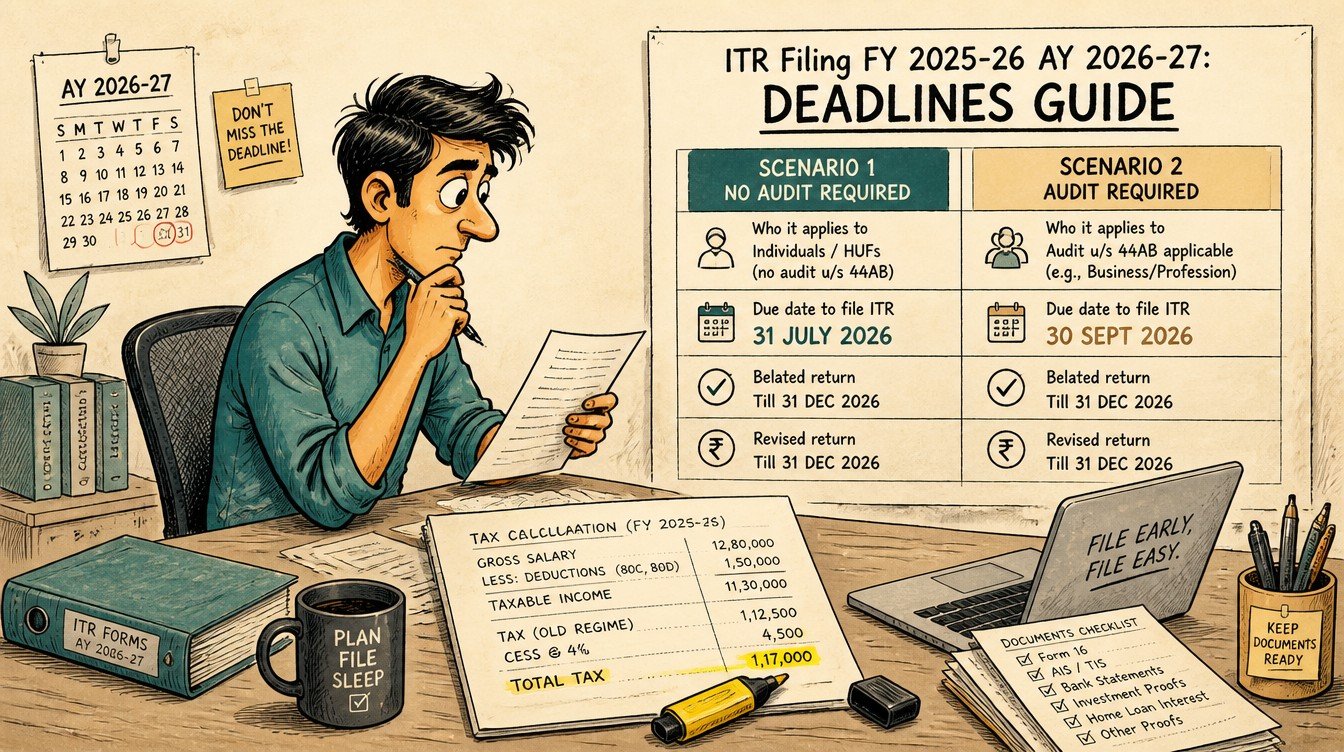

Category-wise deadlines for FY 2025-26

The table below summarises the staggered deadlines announced for FY 2025-26 income.

| Taxpayer category | Typical ITR form | Due date for FY 2025-26 |

|---|---|---|

| Salaried individuals, pensioners, ordinary investors (no audit, no business) | ITR-1, ITR-2 | 31 July 2026 |

| Non-audit business and professional filers (presumptive or regular but below audit threshold) | ITR-3, ITR-4 | 31 August 2026 |

| Audit cases under Section 44AB | ITR-3, ITR-5, ITR-6 | 31 October 2026 |

| Transfer pricing cases (international or specified domestic transactions) | ITR-3, ITR-6 with Form 3CEB | 30 November 2026 |

| Belated and revised returns (any category) | Same form, with revised flag | 31 March 2027 |

Salaried filer track (31 July 2026)

This is the largest cohort. Most filers in this bucket are running on TDS-deducted salary, with bank interest, dividends and possibly capital gains layered on top. Form 16, AIS and TIS data are usually complete by the end of June, which leaves four to five weeks of comfortable filing time before the 31 July 2026 window closes.

Non-audit business track (31 August 2026)

Freelancers, professionals, and small businesses below the Section 44AB audit threshold get one extra month. Most presumptive filers under Section 44AD or 44ADA file in this window. Make sure GST returns and Form 26AS are reconciled before submission, since mismatches in this cohort trigger the bulk of CPC notices.

Audit and transfer pricing tracks (31 October and 30 November 2026)

These two tracks depend on third parties (auditors and transfer pricing professionals). The deadlines are calibrated to give auditors enough time after the 30 September audit-report cutoff. Missing the audit deadline carries a separate penalty under Section 271B, on top of the regular Section 234F fee.

Revised return and ITR-U: the safety nets

Filing a return is not a one-shot event. The Income Tax Act provides two distinct correction routes once the original return is submitted.

Revised return under Section 139(5)

A revised return can be filed if a genuine mistake or omission is discovered after the original filing. For FY 2025-26, the deadline for revised returns has been extended to 31 March 2027. The revised return overwrites the original; only the most recent submitted version is treated as the return on record.

ITR-U updated return: a 4-year extended window

The Finance Act 2025 extended the ITR-U window from 24 months to 48 months from the end of the relevant assessment year. For FY 2025-26 (AY 2026-27), that pushes the absolute last date for an updated return out to 31 March 2031. ITR-U is meant for adding missed income or correcting under-reported income, not for claiming a fresh refund or reducing a previously reported tax liability.

When each route applies

The order to keep in mind is straightforward. If the original due date has not yet passed, file a revised return. If 31 March 2027 has passed but five-and-a-half years have not yet expired from the end of FY 2025-26, ITR-U is the available route, with an additional tax that scales sharply over time.

Belated return penalty math under Section 234F

A belated return is one filed after the original due date but before 31 December 2026. The first cost is a flat Section 234F late filing fee.

Section 234F late fee

For total income above Rs.5,00,000 (5 lakh), the Section 234F fee is Rs.5,000. For total income up to Rs.5,00,000, the fee is capped at Rs.1,000. There is no late fee if income is below the basic exemption limit and a return is not otherwise required.

Section 234A interest on unpaid tax

If self-assessment tax is still pending when the return is filed late, Section 234A interest applies at 1% per month or part of a month on the unpaid tax, from the day after the original due date until the date of actual payment. This compounds the cost of delay.

Refund delay and other knock-on effects

A belated return also forfeits the right to carry forward most losses (except house property loss) and delays any refund by several weeks. For investors with capital losses to set off in later years, missing the original deadline can be an expensive structural mistake even if the tax outflow is small.

What changes in the new ITR forms for AY 2026-27

The CBDT has been steadily expanding the disclosure schedules. For AY 2026-27, salaried filers should expect a few new fields.

Expanded crypto and VDA reporting

Schedule VDA is now richer, with each transaction summarised by purchase date, sale date, cost basis and consideration. From 1 April 2026, registered Indian exchanges are also required to share data with the IT Department, which means Schedule VDA mismatches will be visible in AIS faster than before.

Pre-filled foreign income and asset fields

Schedules FA and FSI carry pre-filled data for many resident filers, sourced from common reporting standard exchanges. Salaried filers with ESOPs from foreign parent companies should expect this section to populate automatically, and should reconcile against their own broker statements before submission.

Old vs new regime selection inside the form

The new regime is the default. Salaried filers without business income can still choose the old regime by selecting the toggle inside the form. Filers with business income who exit the new regime can only re-enter once, so the regime choice for business income should be made deliberately.

Documents and data to assemble before filing

The single biggest cause of last-week filing chaos is missing source documents. A pre-built checklist solves most of it.

Income side

- Form 16 from each employer for the year

- Form 16A for TDS on interest, dividends, professional fees

- AIS and TIS downloaded from the compliance portal

- Capital gains statements from brokers and AMCs

- Bank, post office and corporate FD interest certificates

- Rental income receipts, with tenant PAN if rent above Rs.1,00,000 per year

Deduction and exemption side

- Rent receipts and rent agreement, for HRA claims in the old regime

- Section 80C investment proofs (PPF, ELSS, life insurance, EPF, principal on home loan)

- Section 80D health insurance premium receipts

- Section 80CCD(1B) NPS Tier-1 deposit proof for the additional Rs.50,000 deduction

- Home loan interest certificate from the lender

Bank and identity side

- PAN and Aadhaar (already linked)

- Bank account number and IFSC of the refund account

- Last year’s acknowledgement and any pending CPC notices

Filing checklist for salaried filers (step by step)

The walkthrough below assumes a tax-resident salaried filer with one or two employers, some interest income, and standard deductions. It is a practical sequence rather than a portal screenshot tour.

Step 1: Reconcile Form 16, Form 26AS and AIS

Before opening the e-filing portal, place Form 16, Form 26AS and AIS side by side. Salary, TDS, interest and dividend numbers should match. If AIS shows transactions you do not recognise, raise a feedback inside the AIS portal first.

Step 2: Pick the right ITR form

A salaried filer with income up to Rs.50,00,000 (50 lakh), no capital gains beyond LTCG of Rs.1,25,000, one house property, and no business income usually files ITR-1. The moment capital gains, multiple properties, or foreign assets enter the picture, the form is ITR-2.

Step 3: Compare new vs old regime before submission

The e-filing portal includes a regime comparison utility. Run both regimes once with the actual deductions claimed. Differences of even a few thousand rupees are worth chasing in the year of regime choice.

Step 4: Pay self-assessment tax if needed

If TDS has not fully covered the liability, pay the balance through the e-pay tax facility on the portal. Note the BSR code, challan serial number and date, and enter them in the tax-paid schedule.

Step 5: Submit and e-verify within 30 days

Submission alone is not enough. The return must be e-verified through Aadhaar OTP, net banking, or another approved channel within 30 days. An unverified return is treated as not filed, and the late-fee clock continues to tick.

Common mistakes that trigger CPC notices

Most CPC notices in the salaried cohort come from a small set of repeated mistakes.

Mismatched TDS or salary numbers

The figure in Form 16 must reconcile with the salary income reported in the return. Even a Rs.500 mismatch between TDS in Form 16 and Form 26AS can trigger an automated 143(1) intimation.

Ignoring AIS and TIS prompts

Bank interest, dividend payouts and broker capital gains now flow into AIS. Returns that report only Form 16 income while AIS shows additional inflows are the single most common notice trigger.

Picking the wrong ITR form

Filing ITR-1 when capital gains or foreign assets exist creates a defective return notice under Section 139(9). The return then has to be re-filed in the correct form, and the original date of filing is preserved only if the defect is cured in time.

Advanced situations: ESOPs, foreign income and dual employers

Even within the salaried bracket, a few edge cases need extra attention.

Foreign ESOPs and RSUs

Vested foreign stock counts as salary income at vest and as capital gains at sale. Both legs should be reported in the same year for the same instrument, and Schedule FA needs the holding details at the end of the calendar year.

Dual employment in the same year

If you changed jobs mid-year, both Form 16s have to be aggregated. The old employer will not have given credit for the new employer’s TDS, which often leaves a residual tax liability at year-end. Pay this self-assessment tax before submission to avoid Section 234B and 234C interest.

Capital gains alongside salary

Once equity or mutual-fund LTCG cross Rs.1,25,000 in the year, ITR-2 is mandatory. The reporting also has to split between listed equity, debt mutual funds, and other capital assets, since the post-Budget 2024 rate structure differs across them.

How the portal handles late filing in practice

The e-filing portal does not block a late return outright, but it changes the experience in a few visible ways.

Late fee added at submission

Once the original due date passes, the portal automatically computes the Section 234F fee at the time of return submission. It must be paid before the return can be e-verified.

Refund timelines stretch

CPC has been processing on-time refunds in two to six weeks. Belated returns are processed in a separate queue and often take six to ten weeks. For larger refunds, filing on time is the simplest cash-flow optimisation available.

Loss carry-forward is forfeited

Capital losses, business losses, and most other losses cannot be carried forward if the return is belated. House property loss is the only loss category that survives a belated return. For F&O traders and equity investors with bad years, this is the single biggest reason to file by the original due date.

Frequently asked questions

Is 31 July still the ITR deadline for salaried Indians in FY 2025-26?

Yes. The staggered system did not delay the salaried deadline. Individuals filing ITR-1 or ITR-2 with no audit requirement continue to file by 31 July 2026 for FY 2025-26.

What is the absolute last date to fix an FY 2025-26 return?

The revised return route is open until 31 March 2027. After that, the ITR-U updated return is available, with additional tax that escalates over four years, all the way up to 31 March 2031.

Can a belated return still claim a refund?

Yes, a belated return can still claim a refund, subject to processing. What it cannot do is carry forward most categories of losses, which is often the more expensive consequence.

Does the staggered deadline change Section 234A interest?

No. Section 234A interest at 1% per month applies from the day after the applicable original due date, so the interest start date shifts in sync with the staggered category.

What happens if 31 July 2026 falls on a weekend or holiday?

The Income Tax Department typically clarifies through a press release whether the deadline is administratively extended. In recent years, the portal has accepted returns through the day announced by the CBDT advisory, which is the document to rely on.

Related guides covering the new vs old regime decision, ITR-U mechanics, belated return penalty math, and the salaried-filer ITR form picker are forthcoming on this site.