Six times a year, the Monetary Policy Committee of the Reserve Bank of India publishes a statement that moves trillions of rupees across Indian markets in the hours that follow. For most salaried Indian households, the MPC statement determines the trajectory of home-loan EMIs, fixed-deposit rates, debt-fund returns, and indirectly equity-market sentiment. Yet the statement itself is rarely written for a salaried audience; it is a dense document combining the policy rate decision, the inflation outlook, the growth outlook, the stance, and the vote split, with a separate set of regulatory announcements often appended. A working rbi mpc decoder india framework converts the 20-page statement into the five or six numbers that actually matter for a household’s financial plan.

This guide walks through the structure of an MPC statement section by section, the specific numbers and phrases to highlight on a 10-minute read, and how to interpret the vote split and any dissent at the committee level. The aim is to make MPC days more useful and less anxiety-inducing for salaried investors who do not need to trade the announcement but do need to understand what it means for their household.

What the MPC Does and Why It Matters to a Household

The Monetary Policy Committee, set up under the RBI Act, 1934 (as amended by the Finance Act, 2016), is the six-member body responsible for setting India’s policy interest rate.

The composition of the MPC

The MPC has six members in two groups, with each member having one vote.

- Three members from the RBI: the Governor, the Deputy Governor in charge of monetary policy, and one other RBI official.

- Three external members appointed by the Government of India for fixed terms.

- The Governor has a casting vote in the event of a tie.

- Decisions are taken by majority, with individual member voting records published.

The policy rate

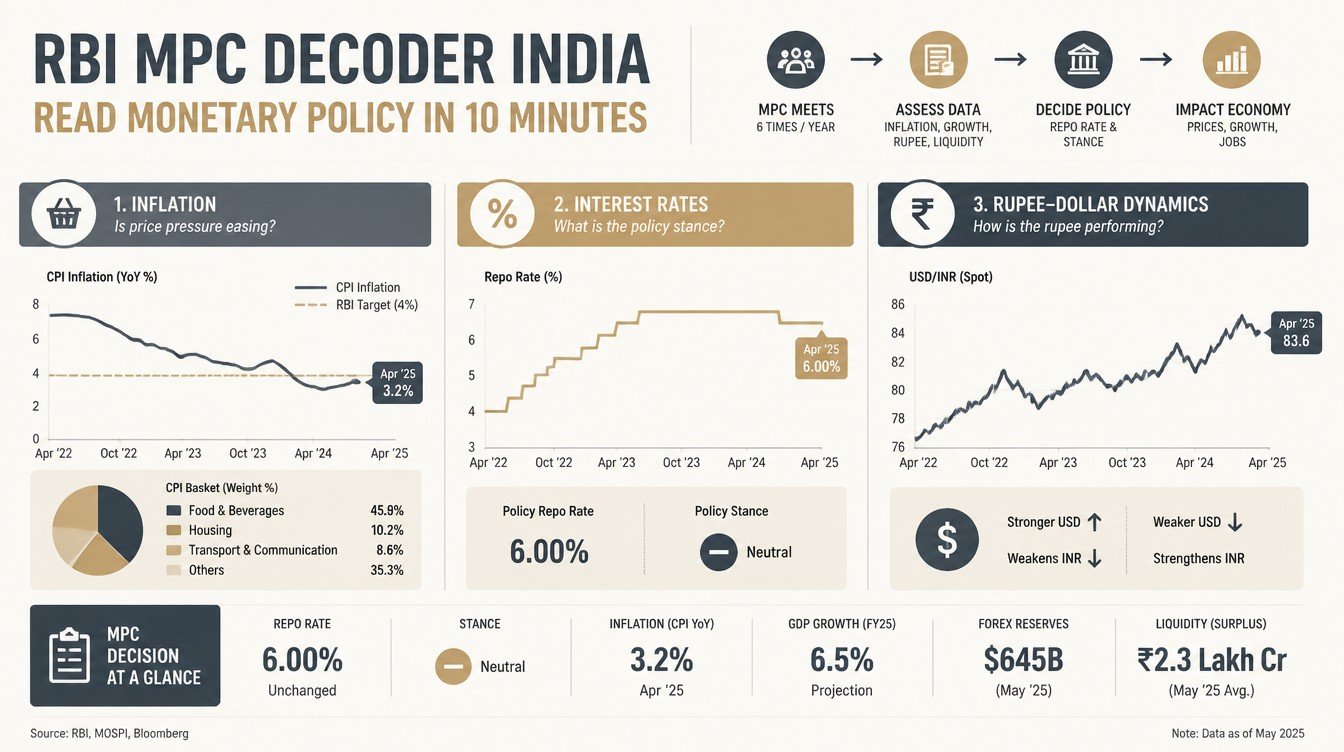

The main policy rate the MPC sets is the repo rate, the rate at which the RBI lends to banks against eligible collateral. Other rates in the corridor (the standing deposit facility rate, the marginal standing facility rate) are typically set at fixed spreads around the repo, though the spreads can be adjusted.

The transmission to households

The repo rate is the input that ultimately drives household-level rates. Floating-rate home loans benchmarked to the repo rate (under the EBLR framework introduced in 2019) reset within months of any repo change. Fixed-deposit rates, savings-account rates, and personal-loan rates respond with some lag, depending on the bank’s deposit and lending mix. Debt-fund NAVs respond more immediately because their portfolio bonds are marked to market.

The inflation-targeting mandate

The MPC operates under an inflation-targeting mandate, with a target of 4 percent CPI inflation and a tolerance band of plus or minus 2 percentage points. The mandate is the primary frame within which MPC decisions are explained; growth, currency, and financial stability concerns are also considered but secondary to the inflation target.

The Five Sections of an MPC Statement

An MPC statement typically has the same five sections in the same order. Knowing where to look in each section saves time.

Section 1: The policy decision

The first paragraphs announce the policy decision: a hold, a cut, or a hike of the repo rate in basis points. The vote split (e.g., 4 to 2, 5 to 1, 6 to 0) is usually disclosed in the same paragraph or shortly after. The decision is the single most important sentence in the statement.

Section 2: The stance

The stance is the MPC’s forward guidance about likely future actions. Common stances include “accommodative” (likely to cut), “neutral” (no clear bias), “calibrated tightening” (likely to hike), “withdrawal of accommodation” (transition from cutting to neutral or hiking), and similar. The stance is often the most market-moving phrase after the rate decision itself.

Section 3: The inflation outlook

The MPC provides quarterly CPI inflation projections for the current and next financial year. Comparing the new projections to the previous statement’s projections reveals the MPC’s revised view. Upward revisions of inflation projections typically lead to a hawkish stance; downward revisions to a dovish stance.

Section 4: The growth outlook

The MPC publishes its real GDP growth projection for the current financial year, with quarterly breakdowns and the risks called out. Growth projections that are revised downward can soften an otherwise hawkish inflation stance; upward revisions can harden it.

Section 5: Regulatory announcements

The last part of the statement usually includes announcements unrelated to the rate decision: changes in liquidity-management tools, new banking regulations, updates to UPI or payment-system frameworks, fintech-sector measures, and similar. These can have material impact on specific sectors even when the rate decision itself is unchanged.

What to Highlight in a 10-Minute Read

For a salaried investor who does not need to trade the announcement, the five-question checklist below captures the essentials.

Question 1: Did the policy rate change?

The repo rate as a number, the change in basis points (or no change), and the new effective date. Anchor the comparison against the previous repo rate. A change of 25 basis points is a typical small adjustment; 50 basis points is a more significant signal; 100 basis points or more is reserved for major policy shifts.

Question 2: What is the stance?

The exact phrase used (accommodative, neutral, withdrawal of accommodation, calibrated tightening) and any modifier in front. Compare to the previous stance; a change in stance is often more market-moving than a rate change without a stance change.

Question 3: How did the inflation forecast move?

The CPI inflation forecast for the current financial year and the upcoming quarters, compared to the projections in the previous statement. A 20 basis point revision either way is small; a 50+ basis point revision signals a meaningful change in the MPC’s view.

Question 4: How did the growth forecast move?

The real GDP growth forecast for the current financial year, compared to the previous projection. Growth revisions sometimes get less attention than inflation revisions but can be equally important for the equity market response.

Question 5: What is the vote split?

The number of members voting for the decision versus the number dissenting. A unanimous 6-0 vote signals strong committee consensus and reduces the likelihood of a reversal in the near future. A 4-2 or 3-3 vote signals divergent views and a higher probability of a different decision next meeting.

Reading the Vote Split and Dissents

The individual voting record and any dissenting statements are often the most informative part of the MPC release for understanding what comes next.

The unanimous decision

A 6-0 unanimous vote suggests strong committee consensus on both the decision and the view of the economy. The next meeting is more likely to extend the same direction unless macro data surprises materially.

The narrow majority

A 4-2 split signals that two members had a different view on the rate, the stance, or both. The minority’s dissenting statement (published separately) provides the alternative reasoning. If the minority view is gaining traction across meetings, the MPC may be approaching a policy reversal.

The dissent on stance vs rate

Sometimes the dissent is on the stance language rather than the rate decision itself. A vote where members agree on holding the rate but disagree on whether to call the stance “accommodative” or “neutral” reveals the committee’s evolving forward bias.

External vs internal member dissent

The three external members are often the more independent voices on the committee. Dissent from one or two external members has been a recurring pattern in past MPC cycles. The market typically reads external dissent as a stronger signal of dispersion than RBI-internal dissent.

The Indicative MPC Day Checklist for Salaried Investors

The table below summarises what to look at, why, and what it means for the household.

| What to find | Where in the statement | Why it matters for the household |

|---|---|---|

| New repo rate and change in basis points | First paragraph | Sets the direction for EBLR-linked home loan EMIs and FD rates |

| Policy stance | Early in the statement, often the second numbered point | Forward guidance on the next 3 to 6 months |

| CPI inflation forecast for full year | Inflation outlook section | Anchors expectation of future rate moves |

| GDP growth forecast for full year | Growth outlook section | Equity-market sentiment driver; affects sector rotation |

| Vote split (decision and stance) | End of decision section | Signals likelihood of direction change at next meeting |

| Regulatory announcements | End of the statement | Banking, UPI, fintech, NBFC-sector specifics |

The 60-minute post-MPC follow-up

After the initial read, the market reaction in the next 60 minutes (debt-market yields, bank stock prices, currency move) provides additional context. The market sometimes reads the statement differently from what the words alone seem to say; the price response is the consensus interpretation.

The bank-by-bank EBLR update

Within a few weeks of any repo-rate change, banks update their External Benchmark Lending Rates (EBLRs) for floating-rate retail loans. Existing home-loan borrowers should expect a corresponding change in their EMI or tenure (depending on the loan’s chosen reset mechanism). The bank’s net-banking screen or a written communication usually confirms the change.

How MPC Decisions Affect Different Household Decisions

A clear cause-and-effect view helps the household translate the MPC statement into specific actions.

For home-loan borrowers

Floating-rate home loans benchmarked to the repo rate respond directly to MPC decisions. A 25 basis point cut lowers the EMI (or shortens the tenure) on a Rs.50,00,000 (50 lakh) loan by a small but real amount. A 25 basis point hike does the reverse. Borrowers should look at the new EMI within 2 to 3 months of any repo change and decide whether to accept the EMI change or the tenure change as the reset mode.

For FD investors

Fixed-deposit rates typically lag the policy rate by 2 to 6 months. After a series of rate cuts, FD rates fall but not by the full cut amount immediately. After hikes, FD rates rise with a similar lag. The implication for an investor with maturing FDs is to lock in slightly earlier than the rate reset is expected, particularly in a cutting cycle.

For debt-fund investors

Debt-mutual-fund NAVs respond more immediately because their portfolios are marked to market. A rate cut produces a small NAV increase (bond prices rise as yields fall) for funds with longer-duration portfolios; a rate hike produces a small NAV decline. Investors should match the fund’s duration to the household’s expected hold period rather than chase short-term NAV moves.

For equity investors

Equity-market response to MPC decisions is more nuanced. Rate cuts typically support equity valuations through lower discount rates and improved corporate-borrowing terms. Rate hikes do the reverse. Sector-level responses vary: banks often gain from rising rates (better net interest margins), rate-sensitive sectors like real estate and autos prefer falling rates. The household’s equity SIP should continue regardless of any single MPC decision.

Common Mistakes Households Make on MPC Days

The same handful of mistakes appear in retail responses to MPC announcements across cycles.

Reacting to the announcement intraday

Trying to trade equity or debt mutual funds in the hours after an MPC announcement is rarely productive for a salaried investor. The market has typically priced in the most likely outcome before the announcement and reacts to the surprise component within minutes. Retail orders placed an hour after the announcement participate at the post-news price.

Misreading “no change” as no signal

A “no change” decision is itself a signal, particularly when expectations were biased toward a change. The stance language and the vote split provide the additional information even when the rate itself is unchanged. Many of the most market-moving MPC days have been “no change” decisions with hawkish or dovish stance shifts.

Over-fitting to a single MPC’s forecast

The MPC’s inflation and growth forecasts are point estimates at a moment in time. The forecasts are revised at every meeting based on new data. Building long-term financial decisions around a single MPC’s specific forecast number is over-fitting; the more useful signal is the direction of revisions across two or three successive meetings.

Switching debt funds based on one MPC

Some retail investors switch debt funds (shorter duration to longer duration or vice versa) based on a single MPC announcement. The transaction costs, exit loads, and capital-gains tax often exceed the expected return improvement. Debt-fund duration should be aligned to the household’s hold period, not to MPC trading.

FAQ

How often does the MPC meet?

The Monetary Policy Committee meets at least four times a year under the RBI Act, but in practice meets every two months, producing six meetings per year. The exact dates are announced in advance on the RBI website. Each meeting concludes with the publication of the policy statement and the resolution, followed by a press conference by the Governor.

What is the difference between the repo rate and the EBLR for my home loan?

The repo rate is the rate at which the RBI lends to banks. The EBLR (External Benchmark Lending Rate) is the bank-specific lending rate for retail loans, typically set as the repo rate plus a bank-specific spread plus the borrower-specific credit risk premium. When the MPC changes the repo rate, the EBLR moves in lockstep within a defined reset cycle (usually quarterly). The bank’s spread and the borrower’s risk premium do not change with each MPC decision; only the repo component does.

If the repo rate is cut, will my FD rate fall immediately?

Not immediately. Bank deposit rates typically respond with a lag of 2 to 6 months after a repo-rate change, depending on the bank’s deposit mix and asset-liability management. The lag is shorter for banks with significant new lending coming online and longer for banks with stable deposit franchises. Existing FDs continue at their booked rates until maturity; only renewals are affected.

What does “withdrawal of accommodation” stance mean?

“Withdrawal of accommodation” is a stance language signalling that the MPC is reducing the supportive bias of monetary policy without necessarily moving to active tightening. It is typically used in transitions from a cutting cycle to a hold or hiking cycle. The phrase suggests the next move is more likely to be a hike than a cut, all else equal.

Should I time my home-loan part-prepayment around MPC days?

Generally no. The part-prepayment decision should be based on the household’s surplus cash flow, the loan’s effective interest rate, and the alternative use of the capital, not on any single MPC announcement. A part-prepayment made the day after a 25 basis point cut saves a marginal amount relative to one made a month earlier; the operational cost of timing the decision is not worth the small saving. The disciplined annual or quarterly part-prepayment rhythm beats any attempt to time MPCs.

Related guides on this topic are coming to learnfinedge.com soon.