The yield on the Government of India 10-year benchmark bond hovering around 7 percent in 2026 is not just a number on a market dashboard; it is the reference point that quietly anchors every other fixed-income decision in the country. Bank deposit rates, corporate bond yields, mutual-fund debt returns, home-loan EBLRs, and even equity-valuation discounts all reference, directly or indirectly, the G-Sec curve. For a salaried Indian investor evaluating the fixed-income sleeve of the household portfolio, a working understanding of gsec yield india 2026 dynamics is now as important as understanding equity SIPs and tax saving. Market-linked instruments carry market risk; read scheme-related documents carefully before investing.

This guide walks through what the G-Sec yield curve looks like in 2026, how a retail investor can access G-Secs directly, the choice between direct G-Sec ownership and a bond mutual fund as the route, and the practical implications for the household’s debt allocation. The framework applies to a salaried investor with at least a 5 to 10 year fixed-income horizon, not to short-term cash management.

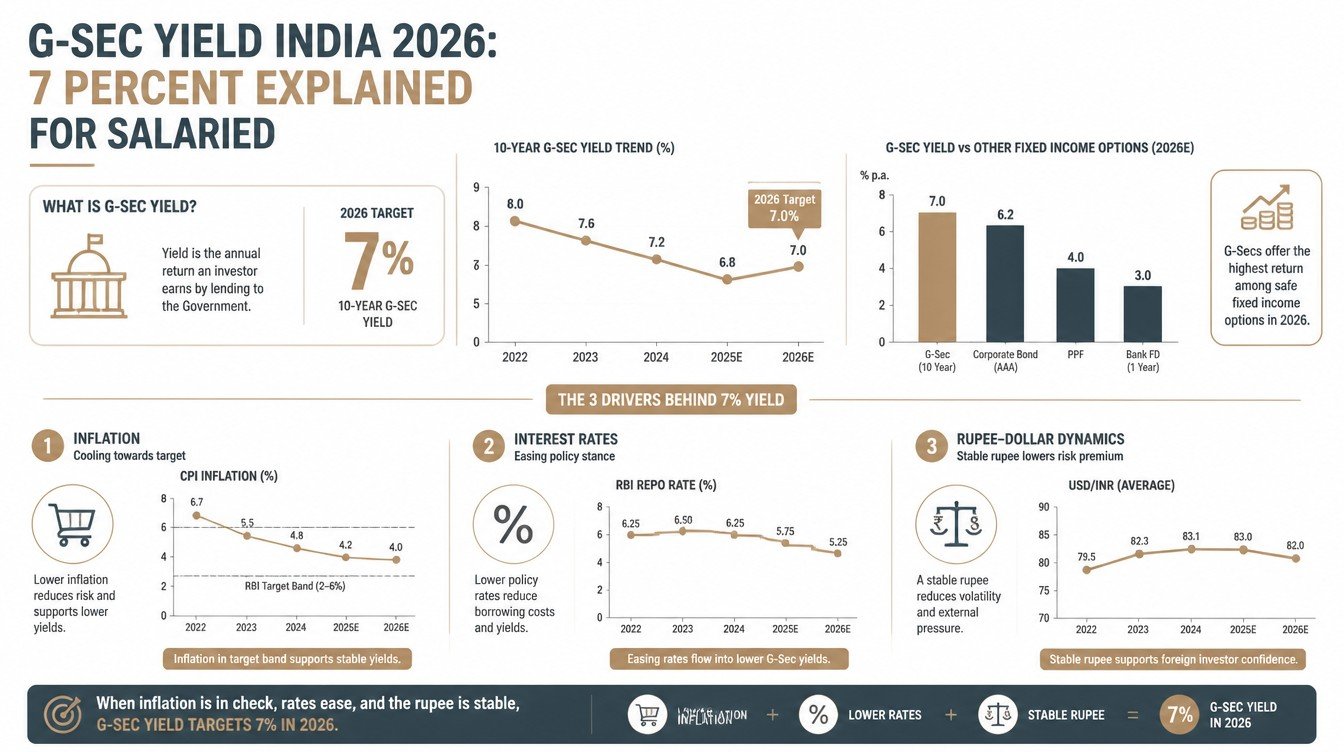

Gsec Yield India 2026: Why 7 Percent Matters

A G-Sec yield is the annualised return an investor receives by holding a Government of India bond to maturity, assuming the coupons are reinvested at the same rate.

The risk-free benchmark

G-Secs are sovereign bonds backed by the full faith and credit of the Government of India and are considered the lowest-credit-risk fixed-income instruments available to Indian investors. The yield on these bonds is the closest analog India has to a “risk-free rate” used in global finance textbooks. Every other domestic interest rate is structurally above the G-Sec yield, with the spread reflecting credit risk, liquidity, and other factors.

The 10-year benchmark

The 10-year G-Sec is the most widely tracked benchmark on the Indian curve. The yield on the latest-issued 10-year G-Sec (the “on-the-run” 10-year) is the standard reference for headlines and market commentary. As of 2026, that yield has been trading around 7 percent (give or take 25 to 75 basis points depending on the market environment), reflecting the RBI’s policy stance, inflation expectations, and the supply-demand balance for government debt.

The transmission to households

The 10-year G-Sec yield is the input from which bank lending rates, corporate bond yields, and debt-fund return expectations are built. A 100 basis point rise in the G-Sec yield typically pushes home-loan EBLRs higher by a similar amount (with a lag), pushes bond-fund NAVs down (the inverse-price-yield relationship), and tightens corporate borrowing costs. The reverse applies on the way down.

Why 7 percent is psychologically important

A 7 percent G-Sec yield is meaningfully above the typical 6 to 6.5 percent that prevailed in some calmer recent periods, but below the 8 to 9 percent levels that characterised earlier high-inflation phases. The current level reflects a moderating-inflation, growth-supportive policy stance with structural fiscal constraints. For salaried investors, the 7 percent level makes G-Sec ownership genuinely attractive in real terms after expected inflation.

The Yield Curve Snapshot

The yield curve plots G-Sec yields across maturities, from very short-term Treasury bills to long-dated bonds.

The indicative shape of the 2026 curve

| Maturity | Indicative yield range | Typical use case |

|---|---|---|

| 91-day Treasury bill | Around the RBI repo rate, often a touch below | Cash management for short-term needs |

| 1-year G-Sec or T-bill | Slightly above the repo | Bridging finance, short-term parking |

| 3-year G-Sec | Mid 6 percent range, depending on cycle | Targeted goals 3 to 4 years away |

| 5-year G-Sec | Upper 6 percent range | Medium-horizon income |

| 10-year G-Sec (benchmark) | Around 7 percent | Core fixed-income allocation |

| 30-year G-Sec | Slightly above the 10-year, sometimes flat | Long-horizon income, retirement planning |

The implications of the curve shape

A normal-shaped curve (yields rising with maturity) signals a market expectation of continued positive growth and stable-to-modestly-rising inflation. A flat curve signals a market expecting near-term policy tightening followed by easing. An inverted curve (long yields below short yields) is rare in India but is internationally a recession signal. The 2026 Indian curve has been broadly normal in shape, with modest steepness between the 5- and 10-year tenors.

What moves the curve

The short end of the curve (up to 1 to 2 years) is anchored by the RBI’s policy rate and liquidity-management operations. The middle of the curve (3 to 7 years) reflects expectations about the RBI’s policy path. The long end (10 to 30 years) reflects long-term inflation expectations, fiscal credibility, and global yield levels via international investor flows.

How the curve interacts with household decisions

For a household with a specific time-bound goal (a child’s college fund, a home down payment, retirement), the maturity on the curve closest to the goal’s horizon is the most relevant. Buying a G-Sec maturing in the target year locks in the current yield to maturity for the household, regardless of subsequent yield movements.

Direct Retail Access to G-Secs

One of the most important changes for Indian retail investors in recent years has been the formal opening of direct access to G-Secs through the RBI’s Retail Direct platform.

The RBI Retail Direct portal

The RBI Retail Direct scheme, launched in 2021, allows individual investors to open a Retail Direct Gilt Account directly with the RBI and bid for G-Secs (Treasury bills, dated securities, sovereign gold bonds, state development loans) in primary auctions. The account is opened online with PAN, Aadhaar, and bank details, with no minimum balance requirement.

The primary-auction route

The RBI conducts G-Sec auctions on a defined calendar. The retail investor’s path through a typical primary-auction bid runs through a few simple steps.

- Open or log into the Retail Direct account and check the upcoming auction calendar.

- Select the security (T-bill, dated G-Sec, SDL, or SGB) and the bid amount, with minimum bids typically from Rs.10,000.

- Submit the non-competitive bid before the cut-off time on the auction day.

- Funds are debited from the linked bank account on settlement; units are credited to the Retail Direct Gilt Account.

- Coupon interest is credited to the bank account on the scheduled coupon date; face value is credited at maturity.

The secondary-market route

Retail Direct also allows secondary-market transactions through the RBI’s NDS-OM platform interface. The secondary market is less liquid for very small ticket sizes than the primary auction, but does provide an exit route before maturity for investors who need it.

The operational reality

Direct G-Sec ownership through Retail Direct is operationally cleaner than it has ever been in India, but still requires some learning relative to the simpler experience of bank FDs or mutual funds. The auction calendar, the bid-cycle timing, and the secondary-market mechanics all benefit from familiarity over the first few transactions. The cost is a small operational ceiling on the first few bids; the benefit is the zero-intermediary access to sovereign-credit returns.

G-Sec Direct vs Bond Mutual Fund: The Comparison

For most retail investors, the practical choice for fixed-income allocation is between direct G-Sec ownership and a debt mutual fund. Both have legitimate cases.

The comparison dimensions

| Dimension | Direct G-Sec via Retail Direct | G-Sec or debt mutual fund |

|---|---|---|

| Credit risk | Sovereign, lowest in market | Sovereign for G-Sec funds; varies for other debt funds |

| Yield to investor | The full G-Sec yield, no expense ratio | G-Sec yield minus fund expense ratio (typically 20-50 bps) |

| Liquidity | Secondary-market exit possible but less liquid | Daily NAV-based redemption |

| Reinvestment risk | Coupons need to be reinvested manually | Fund typically reinvests automatically |

| Tax treatment | Interest taxed at slab rate; capital gain on secondary-market sale per debt-fund rules | Debt-fund tax treatment under recent Finance Act provisions, typically slab rate |

| Operational complexity | Moderate: RBI Retail Direct account, auction cycle | Lower: standard mutual-fund flow |

| Suitable for | Investors with specific maturity goals and willingness to manage operationally | Investors who want simpler access and active duration management |

The yield-to-maturity advantage of direct ownership

Holding a G-Sec directly to maturity guarantees the yield at the purchase date, regardless of subsequent yield moves. A 10-year G-Sec bought at a 7 percent yield delivers exactly 7 percent compounded annualised return over the 10-year hold, with no path dependence. A bond fund’s realised return depends on the path of yields during the hold period and on the fund manager’s positioning, neither of which the investor controls.

The convenience advantage of mutual funds

Bond mutual funds provide daily liquidity through standard redemption mechanisms, automatic coupon reinvestment, active duration management (within the fund’s stated mandate), and operational simplicity. For investors without a specific maturity target or with a desire for active management, the convenience advantage often outweighs the small expense-ratio drag.

The hybrid approach

Many sophisticated retail investors hold both: direct G-Secs for the matched-maturity portion of the fixed-income sleeve (against specific goals at known dates), and a G-Sec or short-duration debt mutual fund for the operationally simpler portion. The hybrid captures the best of both routes.

The Tax Treatment of G-Sec Interest and Capital Gains

The tax position on G-Secs has implications for how the investor compares the after-tax return against alternatives.

Interest on G-Secs

Interest received on G-Secs is taxable at the investor’s slab rate in the year of receipt. There is no special exemption for sovereign-bond interest under the regular Income Tax Act provisions for individual taxpayers (unlike, for instance, the partial exemption available on Public Provident Fund interest under different mechanisms).

Capital gains on secondary-market sale

A G-Sec sold in the secondary market before maturity produces a capital gain or loss equal to the difference between the sale price and the cost. The tax treatment depends on the holding period and the current Finance Act provisions for debt instruments. Recent Finance Acts have moved much of the debt-instrument capital-gains treatment to slab rate without indexation for most cases.

The hold-to-maturity case

For G-Secs held to maturity, there is no capital gain or loss; the investor receives the face value of the bond on the maturity date. The taxation is limited to the interest income received during the hold period, taxed at slab rate each year.

The after-tax yield comparison

For an investor in the 30 percent slab, a 7 percent pre-tax G-Sec yield translates into approximately 4.9 percent after-tax (ignoring cess and surcharge). For an investor in the 20 percent slab, the after-tax yield is approximately 5.6 percent. Comparing these against equity returns (where long-term equity gains have their own tax treatment under Section 112A) is the basis for asset-allocation decisions.

How to Build the Fixed-Income Sleeve in 2026

The household’s fixed-income sleeve serves three roles: emergency fund liquidity, goal-funding for specific dated needs, and diversification against equity volatility.

The emergency-fund layer

The first Rs.5,00,000 to Rs.15,00,000 of the fixed-income sleeve (depending on monthly household expenses) should be in genuinely liquid instruments: savings account, sweep-in FD, short-duration debt mutual fund, or short-tenor T-bills. The yield is lower than the 10-year G-Sec but the liquidity premium is the point.

The goal-matched layer

Beyond the emergency fund, fixed-income amounts earmarked for specific dated goals (a planned home down payment in 2030, a child’s college fund maturing in 2033) are best matched to G-Secs maturing close to those dates. The matched-maturity strategy locks in the yield-to-maturity for the goal and eliminates path dependence.

The duration-diversification layer

The remaining fixed-income allocation can be split between intermediate-duration G-Sec mutual funds, short-duration debt funds, and corporate-bond funds with appropriate credit screens. The diversification across durations and issuers reduces single-event risk and provides some active-management benefit.

The annual rebalance

Each April, review the fixed-income sleeve against the household’s overall asset allocation. After a year of strong equity returns, the equity share may have grown above target; the rebalance moves capital into fixed income. After a year of weak equity, the rebalance moves the other way. The annual rhythm avoids overactive trading while keeping the structure aligned to the plan.

Common Mistakes Retail Investors Make on Bonds

The same handful of mistakes show up in retail fixed-income allocations.

Treating all “debt” as one bucket

A G-Sec, a corporate bond, a perpetual bank bond, and a high-yield bond fund all sit under the broad “debt” label but have very different credit, liquidity, and tax profiles. The single most common allocation mistake is treating the debt bucket as homogenous and not paying attention to what is inside it.

Chasing yield to credit risk

A bond yielding 9 percent in a market where G-Secs yield 7 percent has a 200 basis-point credit spread that compensates for credit risk. Some retail investors chase the higher yield without understanding the credit, and discover the risk only when the issuer defaults. The discipline is to anchor the household’s debt allocation in sovereign and high-grade credit, with any high-yield exposure as a small, deliberate satellite.

Day-trading bond-fund NAVs

Some investors move in and out of long-duration bond funds based on short-term yield predictions. The transaction costs, the tax leakage from frequent realisations, and the difficulty of consistently predicting yields all combine to make active bond-fund trading rarely profitable for retail. Duration positioning should be aligned to the household’s hold period, not to short-term yield calls.

Ignoring the after-tax yield comparison

A 7 percent G-Sec for an investor in the 30 percent slab is a 4.9 percent after-tax instrument. A tax-free instrument (where available) at 5.5 percent is structurally better, even if the headline yield is lower. The household’s asset allocation should compare on the after-tax basis, not the pre-tax yield.

FAQ

Can I really buy a G-Sec directly from the RBI as a retail investor?

Yes. The RBI Retail Direct scheme, launched in 2021, allows individual investors to open a Retail Direct Gilt Account directly with the RBI and bid for G-Secs in primary auctions or transact in the secondary market through the platform. The account opening is online with PAN, Aadhaar, and bank details, with no minimum balance and no intermediary cost. The platform’s URL is retaildirect.rbi.org.in.

What is the difference between a G-Sec mutual fund and a debt mutual fund?

A G-Sec mutual fund invests predominantly in Government of India securities, with the lowest credit risk available in the debt-fund universe. A debt mutual fund is a broader category that includes G-Sec funds, corporate bond funds, banking and PSU funds, credit-risk funds, dynamic-bond funds, and others. The credit-risk profile varies materially across the category. For pure sovereign-credit exposure, a G-Sec fund or direct G-Sec ownership is the cleaner route.

How is interest on G-Secs taxed?

Interest received on G-Secs is taxable at the investor’s applicable slab rate in the year of receipt. There is no separate exemption or concessional rate. Interest is added to total income and taxed under the head “Income from Other Sources” in the income-tax return. For investors who hold G-Secs through Retail Direct, the half-yearly coupon credit appears in the linked bank account and should be tracked for filing.

If yields rise after I buy a G-Sec, do I lose money?

If you hold the G-Sec to maturity, no. You receive the agreed coupon payments and the face value at maturity, regardless of intervening yield moves. The yield-to-maturity at purchase is the realised return if held to maturity. If you sell in the secondary market before maturity at a higher yield (lower price) than your purchase, you realise a capital loss. The yield-to-maturity discipline is the structural protection against intra-period yield volatility.

Should I shift my emergency fund from a bank savings account to a short-term G-Sec?

For most households, the answer is no, or only partially. Bank savings account balances are liquid within seconds, while G-Sec secondary-market exit takes a few business days. The emergency fund’s primary requirement is immediate accessibility. A common practical structure is to keep one to two months of expenses in a bank savings account, the next two to three months in a sweep-in FD or liquid mutual fund, and any longer-horizon fixed income in G-Secs or G-Sec funds. The layering matches each tier of need to the appropriate instrument.

Related guides on this topic are coming to learnfinedge.com soon.