The tax year concept in India is the single biggest structural change salaried filers will meet when the Income Tax Act 2025 takes effect on 1 April 2026. For decades, filing meant juggling two overlapping labels, the Previous Year and the Assessment Year. The new law replaces both with one clean idea: the Tax Year.

If you draw a monthly salary, have TDS cut by your employer, and file a return every summer, this matters to you. The underlying maths of your tax does not change on day one; what changes is the vocabulary, the timelines you quote, and the way income is labelled. This guide walks a salaried reader through what the tax year is, what it replaces, and how it plays out.

What the Tax Year Concept in India Actually Means

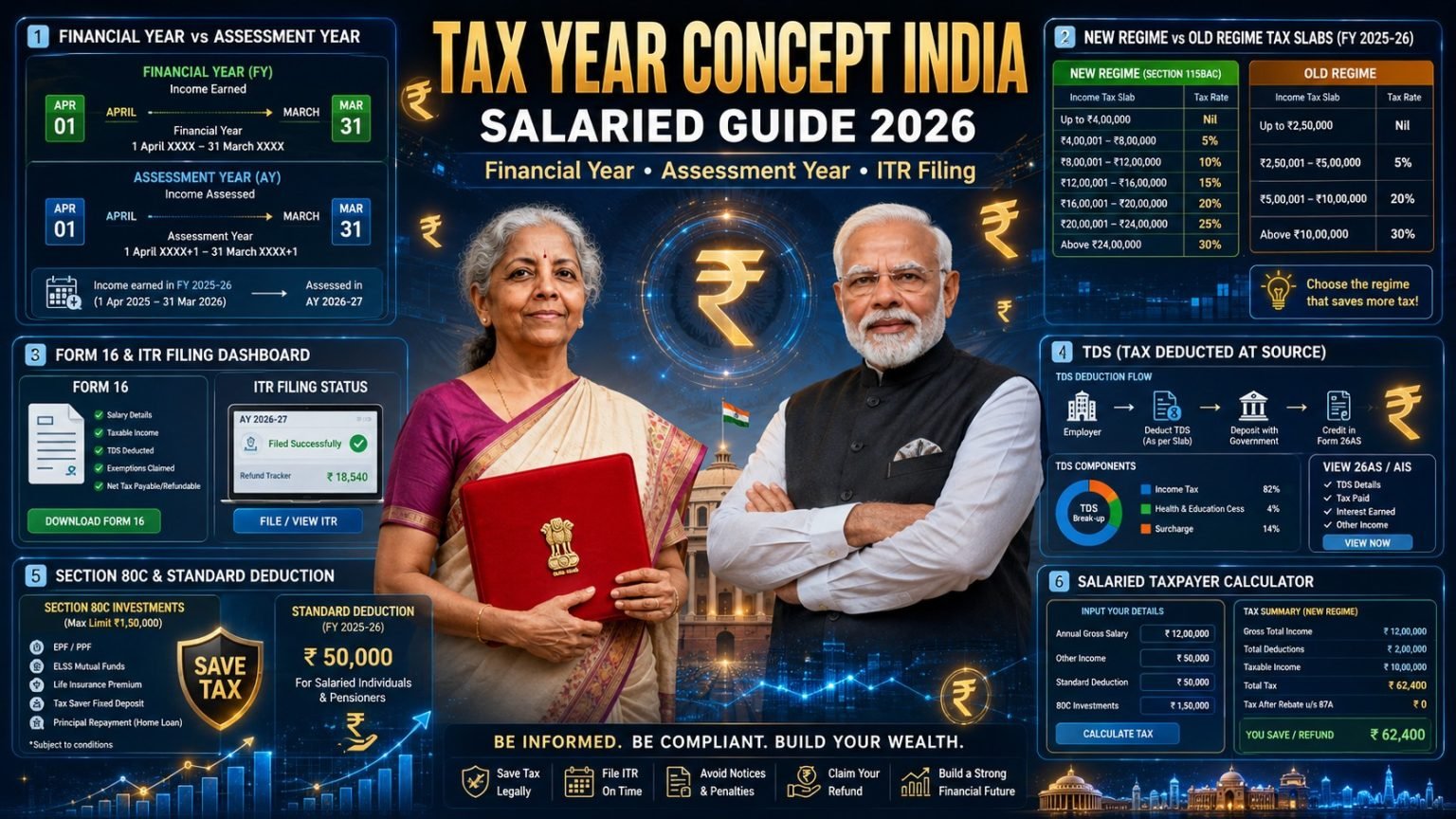

Under the old Income Tax Act 1961, income earned in a twelve-month window was the previous year, and the following year in which you assessed and paid tax was the assessment year. The tax year concept in India collapses these two into one 12-month period in which income is both earned and reckoned.

In practice, a tax year runs from 1 April to 31 March, matching the financial year you already use for payroll and the provident fund, with no second calendar to track.

The core definition

The tax year is the 12-month period for which your income is measured and taxed. For a new business or fresh source of income, it begins on the date that source comes into existence and ends on the following 31 March.

Why the change was made

The previous year and assessment year split was a frequent source of confusion, wrong form selection, and mismatched notices. A common rule of thumb in Indian personal finance is that simpler labels mean fewer mistakes.

What the Tax Year Replaces: AY and PY are retired.

The heart of this reform is a straight substitution: the Income Tax Act 2025 removes the twin terms and installs one.

Previous Year, gone

The previous year was the year in which you earned income. It is folded into the tax year, so the year of earning and the year of reference are now the same.

Assessment year gone

The assessment year was the year after earning, in which you filed and were assessed. You will no longer quote it on your return. The tax year vs assessment year distinction still helps for old records, but going forward there is one year to name.

| Feature | Old law (Act 1961) | New law (Act 2025) |

|---|---|---|

| Year income is earned | Previous Year (PY) | Tax Year |

| The year’s tax is assessed | Assessment Year (AY) | Tax Year (same year) |

| Number of labels | Two | One |

| Period covered | 1 April to 31 March | 1 April to 31 March |

| Effective from | Until 31 March 2026 | 1 April 2026 |

The period itself, April to March, is unchanged; only the naming and the removal of the second year differ. If you have mastered the old versus new tax regime decision points, that logic carries over intact.

Effective Date: Why 1 April 2026 Is the Line in the Sand

The Income Tax Act 2025 becomes operative from 1 April 2026. That date is the boundary between the old two-year system and the new single tax year.

What happens before the date

Income earned up to 31 March 2026 still belongs to the old framework: the previous year, 2025-26, was assessed in assessment year 2026-27.

What happens on and after the date

Income earned from 1 April 2026 onwards falls into the first tax year, running to 31 March 2027, the first period you describe purely as a tax year with no assessment year attached.

A transition worth watching

Keep your AIS and TIS records and statements sorted by date: anything before 1 April 2026 uses old terminology; anything after uses the tax year.

Worked Example: Does a March or April Salary Fall in Which Tax Year?

A salary credited on or before 31 March 2026 stays in the old previous year and assessment year system, while a salary from 1 April 2026 onwards falls into the first tax year. The rule is unchanged: salary belongs to the period in which it is earned, and the April-to-March boundary decides its home.

The March 2026 salary

Your March 2026 salary of Rs 80,000, paid on 31 March 2026, sits in the old previous year (2025-26) and assessment year (2026-27), never touching the new tax year.

The April 2026 salary

Your April 2026 salary of Rs 80,000, paid on 30 April 2026, falls into the first tax year (1 April 2026 to 31 March 2027) and starts your life under the single-label system.

Putting a full year together

Imagine a package of Rs.1,200,000 (12 lakh) across April 2026 to March 2027. Every rupee belongs to one tax year. Follow these steps to place any pay slip:

- Find the month the salary is credited.

- If it is on or after 1 April 2026, it belongs to the tax year.

- If it is dated 31 March 2026 or earlier, it stays under the old PY and AY labels.

- Match each entry against Form 16 so your totals reconcile.

Tax Year Concept in India: Filing Implications for Salaried Earners

Does the tax year change how you file? For most salaried readers the process stays similar, but the return labels change.

Choosing the right period on the form

When you file for income from April 2026 onwards, you report it against the relevant tax year rather than a previous year plus an assessment year, removing a common form-selection mistake. The mechanics still follow the step-by-step return filing guide.

TDS, Form 16, and reconciliation

Your employer continues to deduct TDS monthly and issue Form 16 after year end. Cross-check Form 16 against the annual information statement before submitting, because that habit protects you whatever the year is called.

Deductions and the standard deduction

The tax year change does not touch deductions. The standard deduction of Rs.75,000 under the new regime still applies against salary income.

Advanced Nuances for Experienced Filers

A few edge cases reward attention if you have income beyond salary.

New sources mid-year

If you start a side consultancy partway through the year, its first tax year begins on the date that it starts and runs to the next 31 March.

Capital gains and market-linked income

Gains from selling equity or redeeming mutual fund units belong to the tax year in which the transaction settles. Market-linked instruments carry market risk, and past performance is not indicative of future returns, so time redemptions for real need, not to game a label.

Revised and belated returns

The ability to correct an already filed return continues under the new law. If you spot an omission, a revised return in India remains your route to fix it within the allowed window.

Common Mistakes and How to Avoid Them

Any change in terminology invites errors in the first year, so knowing the traps keeps filing clean.

Mixing old and new labels

The most frequent mistake will be quoting an assessment year for income that belongs to a tax year, or the reverse. One rule fixes it: income up to 31 March 2026 uses AY and PY; later income uses the tax year.

Ignoring reconciliation

Filers who skip the Form 16 versus statement check tend to receive mismatch notices. This risk is unchanged by the tax year:

- Confirm the credit date of every salary entry.

- Reconcile Form 16 totals with your statements.

- Apply the standard deduction and eligible deductions correctly.

- Use the Tax Year label only from 1 April 2026 onwards.

How the Tax Year Concept in India Fits the Wider Reform

The single tax year is one piece of a broader modernisation under the Income Tax Act 2025, aiming for simpler language and fewer overlapping terms.

A cleaner mental model

Think of the old two-year system as a passbook recording a deposit in one book and its interest in a second. The tax year merges both into one ledger, so a single line tells the year.

What stays exactly the same

Slab rates, regime choice, and the April-to-March cycle are unchanged on the effective date. The new tax rules in April 2026 are about structure and clarity, not a fresh tax burden.

Frequently Asked Questions on the Tax Year

What is the tax year concept in India under the Income Tax Act 2025?

It is a single 12-month period, 1 April to 31 March, in which income is both earned and assessed. It replaces the earlier pair, Previous Year and Assessment Year, with one label from 1 April 2026.

When does the new tax year system take effect?

From 1 April 2026. Income on or after that date falls into the first tax year, while income up to 31 March 2026 stays under the old framework.

What is the difference between a tax year and an assessment year?

Under the old law, the assessment year was the year after earning, separate from the previous year of earning. Under the new law, both merge into one tax year, so you no longer quote a separate assessment year.

Does my March 2026 salary fall in the new tax year?

No. A salary credited on 31 March 2026 or earlier belongs to the old previous year, 2025-26, and assessment year, 2026-27. Only salary from 1 April 2026 onwards falls into the first tax year.

Do salaried filers need to change how they file?

The core steps stay similar, but you report income against a single tax year rather than a previous year plus an assessment year. Your employer still deducts TDS and issues Form 16.