TCS on Foreign Remittance India 2026: LRS Rules Explained

A reader in Pune wrote to me last month with a screenshot from her bank. She had wired USD 12,000 to her son’s university in Toronto, and the bank had added Rs 2.04 lakh as TCS on top of the principal. Her panic was understandable. She thought she had lost the money. She had not. She had prepaid a chunk of her FY 2026-27 income tax, and the bank should have explained that better.

The TCS foreign remittance India 2026 framework is the single most misunderstood piece of cross-border tax in the country. Parents funding overseas education, families planning medical treatment abroad, freelancers paying for SaaS subscriptions on US cards, and travellers loading forex prepaid cards all run into it. The rates are not the problem; the timing and the credit mechanic are. This guide walks through the Liberalised Remittance Scheme cap, the current TCS rates after the 2025-26 amendments, the education and medical carve-outs, and a worked example on a Rs 10 lakh overseas tuition transfer so the actual cash impact is visible.

What is the Liberalised Remittance Scheme and where does TCS sit inside it

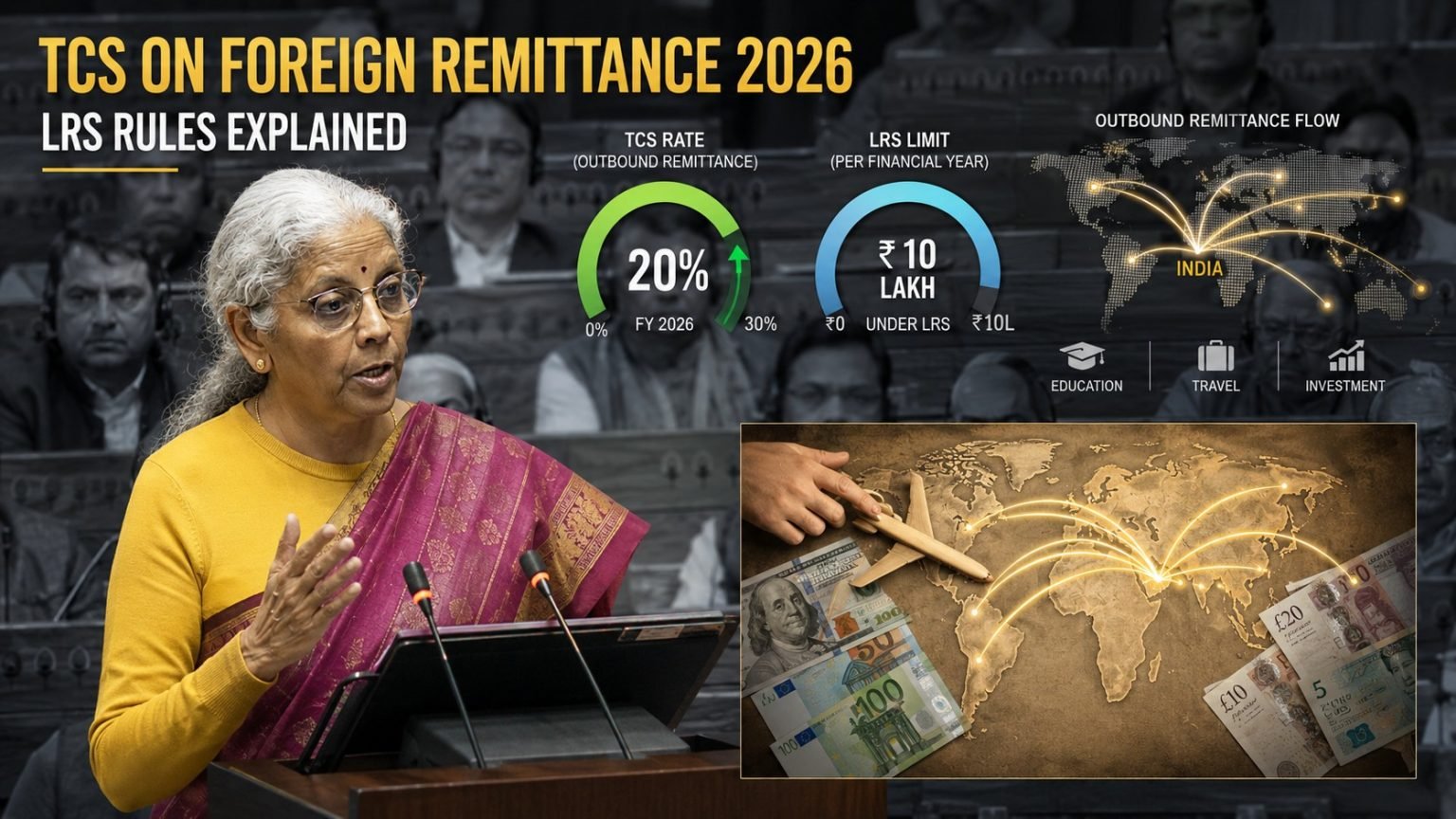

The Liberalised Remittance Scheme, commonly called LRS, is an RBI framework that lets every resident individual, including minors, send up to USD 250,000 per financial year out of India for permitted purposes. The scheme was introduced in 2004 with a much smaller cap and has been progressively widened to its current ceiling. Companies, partnership firms, and trusts do not use LRS; they remit under separate FEMA windows.

Tax collected at source under section 206C(1G) of the Income Tax Act, 1961, is the layer that sits on top of LRS. It is not a separate tax. It is the government collecting a slice of your eventual income tax liability at the moment the bank processes the outward wire, the same way TDS works on salary. The bank or authorised dealer is the collector. You are the collectee. The amount lands in your Form 26AS and your annual information statement and is fully adjustable against your final tax liability at return-filing time.

Why TCS exists on LRS at all

The policy intent is two-fold. First, it creates a verifiable audit trail of outward remittances tied to your PAN, which closes the gap between declared income and actual cross-border spending. Second, in the case of high-ticket transfers, it front-loads the eventual tax pay-out so a salaried earner is not surprised by a large self-assessment liability at filing time. The framework has been tightened twice in the last three years, and the current rate card is the version effective for FY 2025-26 and onwards.

The USD 250,000 annual cap is per person, not per family

Each resident individual gets a separate USD 250,000 envelope in a financial year. A married couple can remit USD 500,000 between them. A family of four, including two adult children, can remit USD 1,000,000. The cap is fungible across permitted purposes: education, medical treatment, gifts, travel, investment in foreign securities, real estate purchase abroad, and maintenance of close relatives. Bank-side reporting consolidates all remittances under your PAN to track the annual ceiling.

The 2026 TCS rate card on LRS, in plain numbers

The rate card splits across two variables: the purpose of remittance and the cumulative amount you have sent in the financial year. The current structure, after the rate revisions effective for FY 2025-26, is the version every bank will apply.

Education and medical remittances

For overseas education and medical treatment, there is a generous threshold. The first Rs 7 lakh of remittances under these heads in a financial year attract zero TCS. Above Rs 7 lakh, the rate splits further by funding source. If the education remittance is funded by a loan from a financial institution as defined under section 80E (banks, NBFCs registered for the purpose, and notified institutions), the rate above Rs 7 lakh is 0.5 per cent. If the remittance is funded from your own savings or a non-80E loan, the rate above Rs 7 lakh is 5 per cent. Medical treatment remittances follow the same 5 per cent slab above Rs 7 lakh.

All other purposes

For every other permitted purpose under LRS, which includes maintenance of close relatives, gifts to non-residents, investment in foreign equities, real estate purchase abroad, and travel and tourism via tour packages, the threshold is also Rs 7 lakh in a financial year. The first Rs 7 lakh under these heads attracts zero TCS. The portion above Rs 7 lakh attracts 20 per cent TCS. The 20 per cent rate is the headline figure most personal-finance commentary in India refers to when discussing the LRS.

Overseas tour packages have a separate treatment

Outbound tour packages purchased from an Indian operator are not technically LRS remittances, but they sit in the same rate framework. The first Rs 7 lakh of tour package spend in a financial year attracts 5 per cent TCS; the portion above Rs 7 lakh attracts 20 per cent. The threshold here is shared with the broader LRS bucket for the same financial year, so a household that has already exhausted the Rs 7 lakh comfort zone on a foreign-securities investment will see the next rupee of tour package spend taxed at 20 per cent on the full amount.

Worked example: Rs 10 lakh transfer for overseas tuition

A clean way to internalise the rules is to walk through a single transaction with numbers. Consider a parent in Bengaluru sending Rs 10 lakh to a Canadian university for a daughter’s master’s programme tuition, funded entirely from a savings account, not from an education loan.

The TCS computation, step by step

Step one is to identify the purpose. Overseas education is the head, so the Rs 7 lakh threshold and the 5 per cent rate above the threshold apply.

Step two is to apply the threshold. The first Rs 700,000 of the remittance attracts zero TCS.

Step three is to apply the 5 per cent rate on the excess. The excess is Rs 1,000,000 minus Rs 700,000, which is Rs 300,000. Five per cent of Rs 300,000 is Rs 15,000.

Step four is the cash flow at the counter. The bank will debit Rs 10,15,000 from the parent’s savings account: Rs 10 lakh is converted to Canadian dollars and wired to the university, and Rs 15,000 is collected as TCS and deposited to the credit of the central government against the parent’s PAN.

The same transaction funded by an 80E education loan

If the same Rs 10 lakh tuition transfer is funded by an education loan from a scheduled bank that qualifies under section 80E, the rate above Rs 7 lakh drops to 0.5 per cent. The TCS becomes 0.5 per cent of Rs 300,000, which is Rs 1,500. The cash impact is materially smaller. This is one of several reasons families with multiple education-funding options should run the loan-vs-savings math holistically rather than reflexively paying from savings. A related discussion on the deduction side is in the LearnFineEdge piece on tax saving beyond 80C.

What if the transfer is Rs 7 lakh or less

A Rs 7 lakh tuition transfer in a financial year, with no other LRS remittances, attracts zero TCS. The bank still reports the remittance to the Income Tax Department under the LRS purpose code, but no amount is collected at source. This is why splitting a large transfer across two financial years, where the academic calendar permits, is sometimes a useful planning move. Each financial year gets its own Rs 7 lakh threshold.

How TCS becomes a credit against your final tax liability

The single most important thing to understand about TCS on LRS is that it is not an additional tax. It is a prepayment that is fully creditable against your eventual income tax for the same financial year. The amount sits in your Form 26AS and AIS, and your return-filing software pulls it in automatically.

The flow from remittance to credit

When the bank collects TCS, it deposits the amount to the central government against your PAN within a stipulated window. The deposit is reported by the bank in its quarterly TCS return, which the Income Tax Department uses to update your Form 26AS, usually with a one-quarter lag. By the time you sit down to file your return for the same financial year, the TCS entries are visible under the appropriate sections of 26AS and the AIS, and the return-filing utility includes them in the tax-credit computation.

The salaried-earner credit mechanic

Section 206C(1H) and the matching clauses in the Finance Act allow a salaried employee to ask the employer to consider TCS on LRS while computing TDS for the year. In practice this requires submitting Form 12BAA (or the equivalent declaration prescribed for the year) to the HR or payroll team, attaching the bank’s TCS certificate. The employer then reduces the monthly TDS by an amount corresponding to the TCS already collected. The net effect is that the parent in the Rs 10 lakh example sees Rs 15,000 of relief in monthly take-home over the rest of the financial year, rather than waiting for a refund after filing.

What if the TCS exceeds your final tax liability

A retired parent or a low-income remitter may find that TCS collected during the year exceeds the final tax liability computed at filing. The excess is a refund processed by the Centralised Processing Centre after the return is filed and processed. The refund typically lands in the bank account linked to the PAN within four to twelve weeks, depending on processing volumes. There is no separate application; the refund is automatic from the return computation.

The carve-outs and the lesser-known edges

The headline numbers cover most transactions, but the carve-outs matter in roughly one in four LRS remittances. The framework has been tweaked enough times that some of the older online write-ups still quote stale rules.

International credit card spends abroad are out of LRS scope

The position after the 2023-24 clarifications is that spends on Indian-issued international credit cards while travelling abroad do not count against the LRS USD 250,000 cap and do not attract TCS. The earlier proposal to bring credit card spends inside LRS was deferred and has not been operationalised. Indian-issued debit cards used abroad, by contrast, do count against LRS and do attract TCS once the cumulative drawdown crosses Rs 7 lakh in a financial year.

Forex prepaid cards loaded for travel

Loading a forex prepaid card from a bank in India counts as an LRS outflow at the moment of loading, even if the spend happens later. The TCS rate that applies is the 5 per cent above the Rs 7 lakh slab for travel and tourism, or 20 per cent above the Rs 7 lakh if the card is for non-tour purposes that exhaust other LRS buckets first. The cleanest planning move is to load the card in a financial year where the LRS bucket has not been exhausted on other heads.

Maintenance of close relatives

Remittances to close relatives abroad, such as a parent sending a child living overseas a maintenance amount, fall under LRS. The Rs 7 lakh threshold and the 20 per cent above-threshold rate apply. The remittance is not deductible against the resident’s income, but it is also not taxable in the hands of a relative as defined in section 56. The standard exemption for gifts from close relatives applies.

Foreign equity investments

An Indian resident buying foreign equities through a permitted route, including Indian platforms that offer US stock access, faces LRS reporting and the TCS rate card. The Rs 7 lakh threshold and 20 per cent above-threshold apply. The TCS is creditable, the same as in any other case. For a household running broad asset allocation with a small foreign equity tilt, the TCS is a cash-flow friction rather than a real cost.

Practical sequencing for FY 2026-27

Most of the cash-flow pain on TCS comes from poor sequencing rather than the rates themselves. A handful of habits keep the cost of compliance low.

Front-load the Rs 7 lakh comfort zone deliberately

The Rs 7 lakh threshold is a one-time annual window. Households expecting both education spend and foreign-securities investment in the same financial year should consciously decide which one earns the threshold. Education and medical heads, anyway, sit at a softer above-threshold rate of 5 per cent, so the threshold is more valuable when applied to the 20 per cent buckets like foreign equities, gifts, and tour packages.

Use the 80E loan route where the math works

An education loan that qualifies under section 80E gives two-layered benefits. The interest is deductible under section 80E with no upper cap for eight years. The TCS rate above the Rs 7 lakh threshold drops from 5 per cent to 0.5 per cent. For larger overseas tuition transfers, the loan-vs-savings comparison is rarely as one-sided as parents assume, and the TCS arithmetic tilts the balance slightly more toward the loan route. The broader rationale for borrowing to fund growth is touched on in the LearnFineEdge guide on term insurance versus investment.

Submit Form 12BAA at payroll to recover TCS in the same year

Salaried parents who have paid significant TCS on overseas tuition or medical remittances should formally communicate the TCS credit to payroll so the in-year TDS is adjusted. Waiting until return-filing for the refund creates a twelve-to-eighteen-month opportunity cost on what is often a non-trivial amount.

Time the academic calendar around the financial year

For a student joining a programme that starts in August, the parent has the option of paying part of the tuition in March of one financial year and part in April of the next. Splitting the spend across two financial years means two separate Rs 7 lakh thresholds. The first Rs 14 lakh is then TCS-free, instead of only Rs 7 lakh on a single-year transfer. The strategy only works where the university accepts staggered payments, but many do.

Mistakes to avoid and what to do if TCS was already deducted in error

Two common mistakes drive most of the complaints I see from readers on this topic. The first is treating TCS as a cost. The second is failing to claim the credit when filing.

Mistake 1: treating TCS as a sunk cost

The TCS is a tax pre-payment, not a fee. Every rupee shows up in 26AS and is adjustable against your final liability. Households that mentally write it off lose visibility on what is essentially a government float that returns to them at filing.

Mistake 2: forgetting to verify 26AS before filing

The bank-side reporting can lag by a quarter. If you filed quickly after March 31 without verifying that the LRS TCS entries are reflected, you may have under-claimed the credit. The remedy is a revised return under section 139(5), filed within the timelines for the relevant assessment year. The Income Tax Department’s portal walks the user through the revised return flow.

Mistake 3: assuming the credit is automatic on the new tax regime

The TCS credit is regime-agnostic. It applies under both the new and old regimes. The new tax regime under section 115BAC removes most exemptions and deductions, but it does not affect TCS credits, which are pure tax pre-payments. Households moving to the new regime should not be discouraged from claiming the TCS adjustment.

What if TCS was deducted on an exempt transaction

Edge cases exist where a bank applies TCS on a transaction that arguably should not attract it. The remedy is to ask the bank for a corrected TCS certificate and ensure the corresponding entry is updated in the next quarterly TCS return. If the bank refuses, the practical path is to claim the credit anyway and let the Income Tax Department’s matching process flag any discrepancy at filing. Most disputes resolve at the bank level within a few weeks.

How TCS interacts with the broader financial planning picture

TCS on LRS is a small piece of a much larger personal-finance question for Indian households with cross-border exposure. The framework is stable enough now that it can be planned around, rather than reacted to.

Education funding decisions

Parents thinking about overseas education for children five to ten years out should layer the TCS reality into the savings plan. A parent saving Rs 25,000 a month into a goal-based corpus for a child’s overseas master’s programme is not building a Rs 30 lakh corpus. They are building a corpus that, at the point of remittance, will be reduced by 5 per cent on the portion above Rs 7 lakh per financial year. The goal amount should incorporate this drag, plus the underlying foreign-exchange movement.

Emergency fund sizing for medical emergencies abroad

A family with a relative receiving treatment abroad may need to remit large amounts at short notice. The 5 per cent TCS above Rs 7 lakh is a real cash-flow item even if creditable later. The emergency fund for such a family should be sized to absorb both the principal remittance and the TCS surcharge, with a buffer for foreign-exchange variation.

Retirement corpus and overseas children

Retirees whose children are settled abroad and who occasionally travel to spend time with them face the LRS cap on travel and maintenance remittances. The 20 per cent above-threshold rate matters most for retirees with limited current income, because the prepaid tax sits idle until the next return is filed. Some retirees plan a partial remittance in March and a partial in April to spread the threshold across two financial years.

Tier 1 NPS withdrawal feeding overseas investment

A retiree pulling a lump sum from NPS Tier 1 at superannuation and considering deploying part of it in foreign equities or real estate via LRS should look at the TCS implication separately from the NPS withdrawal taxation. A primer on the underlying NPS structure is in the LearnFineEdge piece on NPS Tier 1 vs Tier 2.

The two-page checklist for any overseas remittance in 2026

For most readers, a short checklist is more useful than the full rulebook.

- Identify the purpose of remittance. Education, medical, travel, gift, maintenance, investment, or other LRS purposes.

- Check your cumulative LRS remittances in the current financial year against the USD 250,000 cap. The bank will refuse the transaction if the cap is breached.

- Check your cumulative remittances against the Rs 7 lakh threshold for the purpose. Below the threshold, TCS is zero.

- If above the threshold, apply the correct rate: 0.5 per cent for 80E-loan-funded education, 5 per cent for self-funded education or medical, and 20 per cent for everything else.

- Confirm with the bank that the TCS will be deposited against your PAN, and ask for the TCS certificate after the transaction.

- Submit the TCS certificate to your employer’s payroll team along with Form 12BAA (or the current declaration) to claim in-year TDS relief.

- At filing time, verify the TCS entries in Form 26AS and AIS, and reconcile with the return-filing utility.

- If the TCS amount is reflected wrong or missing, follow up with the bank first and file a revised return if needed.

None of this is hard. The complaints I receive on TCS overwhelmingly come from households that did not know step one or step two existed, not from households where the rules genuinely broke down. The framework is built to be navigated, not feared. The Rs 7 lakh threshold per purpose, per person, per year, gives most middle-class families enough headroom to handle ordinary cross-border life without paying a single rupee in TCS, and where the threshold is breached, the amount returns as a tax credit within the same financial year. Treat it as a process item, not a tax shock, and the cash-flow planning becomes straightforward. A more general guide to managing the household tax bill is the LearnFineEdge article on ELSS vs NPS.

Frequently asked questions

Is the 20 per cent TCS rate applied to the entire LRS remittance or only the amount above Rs 7 lakh?

Only the amount above Rs 7 lakh. The first Rs 7 lakh of remittances under most LRS purposes in a financial year attracts zero TCS. The 20 per cent rate applies only to the portion above the Rs 7 lakh threshold. So a Rs 10 lakh non-education remittance attracts 20 per cent on Rs 3 lakh, which is Rs 60,000, not 20 per cent on Rs 10 lakh. The full amount remitted plus the TCS is debited from the savings account, and the TCS is creditable against final tax liability.

Can I claim TCS on an LRS remittance as a credit if I have opted for the new tax regime?

Yes. TCS is a tax prepayment, not a deduction or an exemption. It is fully creditable against final tax liability under both the new and the old tax regimes. Section 115BAC, which governs the new regime, withdraws most deductions and exemptions, but it does not affect TDS or TCS credits. The credit shows up in Form 26AS and AIS and is automatically picked up by the return-filing utility for both regimes.

Does TCS on overseas education tuition apply if the transfer is funded by an education loan?

Yes, but at a softer rate. For education-purpose remittances above the Rs 7 lakh threshold, the rate is 0.5 per cent if the funding comes from a loan that qualifies under section 80E, which includes loans from scheduled banks and notified financial institutions. If the same education remittance is funded from savings or a non-80E loan, the rate above Rs 7 lakh is 5 per cent. Funding the transfer via a qualifying loan brings the in-year cash-flow drag down materially.

Do international credit card spends abroad attract TCS or count against the LRS cap?

The current position is that spends on Indian-issued international credit cards during overseas travel do not count against the LRS USD 250,000 cap and do not attract TCS. The proposal to include credit card spends within LRS was deferred and has not been brought into force. Debit cards and forex prepaid cards used abroad do count against LRS and attract TCS once cumulative drawdown crosses Rs 7 lakh in a financial year, so card choice for overseas spend matters.

How quickly does the TCS amount become visible in my Form 26AS for refund or adjustment purposes?

The bank deposits the TCS to the credit of the central government and reports it in the quarterly TCS return, which usually appears in Form 26AS and AIS with a lag of one to two months after the quarter ends. For a TCS deduction in April, the entry typically reflects it by August or September. Salaried earners who want in-year relief should submit Form 12BAA with the bank’s TCS certificate to payroll, rather than waiting for the 26AS reflection.