The capital gains tax 2026 india framework looks very different from where it stood three years ago. The Union Budget 2024 reset most of the rates and indexation rules, the Finance Act 2025 fine-tuned a few edges, and Budget 2026 carries forward that revised structure into FY 2025-26. This pillar guide collapses the entire capital-gains map into one place: asset-wise short-term and long-term rates for listed equity, unlisted equity, debt mutual funds, gold, immovable property and virtual digital assets, what changed with the removal of indexation, the grandfathering still in force, and how losses can be set off and carried forward.

None of the percentages are invented. They reflect the rates currently codified in Sections 111A, 112 and 112A, together with the special VDA regime under Section 115BBH. Filers should still confirm any post-budget tweak via incometax.gov.in or the CBDT’s FAQ before locking a return.

Why the capital gains tax 2026 india map matters

Capital gains is the single area where rate changes have the largest one-line impact on a taxpayer’s bill. A wrong assumption on holding period or rate can swing a return by several percentage points.

Holding period defines the rate

Every capital asset has a statutory holding period that separates short-term from long-term. The holding period is no longer uniform across assets, which is the first thing most filers get wrong. Listed equity has its own threshold; immovable property has another; debt mutual funds sit in a different bucket entirely.

Indexation has been narrowed

Indexation benefit, once available on most long-term assets, was removed or restricted on several categories under the Budget 2024 changes. A targeted relief was layered for resident individual sellers of land and buildings acquired before July 23, 2024, who can choose between a 12.5% rate without indexation or a 20% rate with indexation.

Special regimes layer on top

Virtual digital assets sit in their own regime under Section 115BBH with a flat 30% rate, no indexation, and severely restricted loss set-off. Cryptocurrency gains do not behave like equity gains in any meaningful sense, which is something the asset-wise table below makes explicit.

Asset-wise rate table for FY 2025-26

The table consolidates the rates in force for capital gains arising during FY 2025-26, ignoring surcharge and cess. The actual liability adds 4% cess and applicable surcharge.

| Asset class | Short-term holding | STCG rate | Long-term holding | LTCG rate |

|---|---|---|---|---|

| Listed equity shares and equity mutual funds (STT paid) | Up to 12 months | 20% under Section 111A | More than 12 months | 12.5% above Rs.1,25,000 exemption under Section 112A |

| Unlisted equity, including foreign stock | Up to 24 months | Slab rates | More than 24 months | 12.5% without indexation |

| Immovable property (land and buildings) | Up to 24 months | Slab rates | More than 24 months | 12.5% without indexation, or 20% with indexation if acquired before July 23, 2024 (resident individual/HUF only) |

| Debt mutual funds (specified, purchased on or after April 1, 2023) | Any holding period | Slab rates | Not applicable | Taxed at slab rates as STCG |

| Gold, gold ETFs and physical gold | Up to 24 months | Slab rates | More than 24 months | 12.5% without indexation |

| Sovereign Gold Bonds (held to maturity) | Not applicable | Not applicable | Held to maturity | Exempt on maturity for individuals |

| Virtual digital assets under Section 115BBH | Any holding period | Flat 30% on gains, no indexation, no loss set-off | Same as STCG | Same as STCG |

Reading the table correctly

The rates above apply to the gain, not the sale proceeds. The gain is computed as net consideration minus cost of acquisition minus cost of improvement minus expenses on transfer. Where indexation is no longer allowed, the cost is taken at actual price paid.

Surcharge cap on LTCG

Surcharge on LTCG covered by Section 112A and Section 111A is capped at 15%, which is meaningfully lower than the 25% or 37% surcharge that can apply on slab-rate income at the top brackets. This cap continues to be one of the design advantages of long-term equity holding.

Listed equity: Section 112A and the Rs.1,25,000 exemption

Listed equity is where most retail investors meet capital gains tax for the first time.

Holding period for shares and equity mutual funds

Listed shares on a recognised stock exchange and equity-oriented mutual funds qualify as long-term when held for more than 12 months. Below that, gains are short-term.

The Rs.1,25,000 LTCG exemption

The first Rs.1,25,000 of long-term capital gains on listed equity in a financial year is exempt under Section 112A. Anything above is taxed at 12.5%. The exemption is per filer per year and is not transferable across years.

STCG at 20% under Section 111A

Short-term gains on the same listed equity instruments are taxed at a flat 20% under Section 111A, irrespective of the filer’s slab. The flat rate replaced the earlier 15% under Budget 2024 changes.

Debt mutual funds: indexation removed, slab rates apply

Debt mutual funds were the largest category to lose preferential tax treatment.

The April 2023 cut-off

Specified debt mutual funds purchased on or after April 1, 2023 do not get long-term treatment at all. Gains are taxed at slab rates regardless of holding period, similar to interest income.

Older units pre-April 2023

Units purchased before April 1, 2023 retain the older treatment: 36-month holding period for long-term classification, with the 20% with indexation rate applying for those long-term gains under the rules in force at the time.

Why this matters for asset allocation

The change effectively pushes investors toward arbitrage funds, target-maturity funds with equity-like structuring, or direct fixed income, depending on horizon. Debt mutual funds remain a legitimate fixed-income vehicle but are no longer a tax-arbitrage instrument.

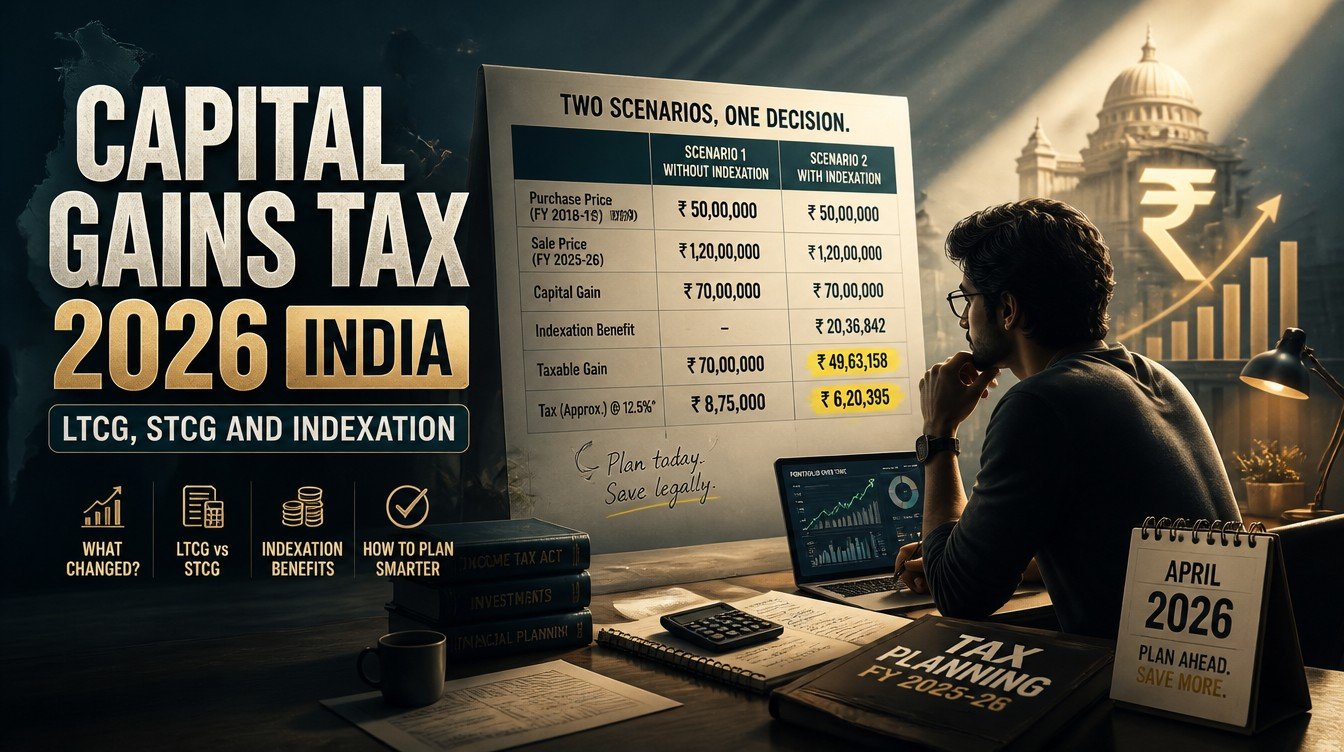

Immovable property: indexation and grandfathering

Land and buildings carry the most complex regime, because Budget 2024 added a special election for older purchases.

Standard new regime: 12.5% without indexation

For transfers on or after July 23, 2024, immovable property held for more than 24 months attracts LTCG at 12.5% without indexation. The cost of acquisition is taken at the actual price paid.

Grandfathering for pre-July 2024 acquisitions

For resident individuals and HUFs who acquired the property before July 23, 2024, the law allows the taxpayer to choose between the new 12.5% without indexation route and the older 20% with indexation route, whichever yields a lower tax. This election is per property.

Section 54 and 54EC reinvestment routes

Long-term capital gains from house property can still be reinvested under Section 54 (in another residential property) or Section 54EC (in specified bonds up to Rs.50 lakh) to claim exemption, subject to the conditions specified in those sections.

Gold, ETFs and Sovereign Gold Bonds

Gold sits in its own bucket with three sub-flavours.

Physical gold and gold ETFs

Holding period above 24 months qualifies as long-term, with LTCG taxed at 12.5% without indexation. Below 24 months, gains are added to total income and taxed at slab rates.

Sovereign Gold Bonds

SGBs held to maturity remain exempt from capital gains for individual investors, which is one of the few remaining structural tax advantages in the gold ecosystem. The 2.5% per annum interest is, however, taxable.

Gold mutual funds

Gold funds are treated similarly to physical gold for capital gains purposes once the underlying is bullion. The treatment may differ if the fund structure is closer to a debt mutual fund; the scheme document is the source of truth.

Crypto and virtual digital assets under Section 115BBH

The crypto regime is the most restrictive of any asset class.

Flat 30% on every gain

Section 115BBH levies a flat 30% tax on income from transfer of any virtual digital asset, regardless of holding period. There is no concessional rate and no long-term carve-out.

No loss set-off, no indexation

Losses on VDA transactions cannot be set off against any other income, nor against gains from other VDAs in many configurations. The loss is also not carried forward to future years. Indexation is not available, and only the cost of acquisition is deductible.

1% TDS under Section 194S

Exchanges deduct 1% TDS under Section 194S on every transfer above the prescribed threshold. From April 2026, registered Indian exchanges share data with the IT Department, which will surface discrepancies in AIS and Schedule VDA more aggressively than in past years.

Set-off and carry-forward rules

The loss set-off framework is just as important as the rate map.

Intra-head set-off rules

- Long-term capital loss can be set off only against long-term capital gain

- Short-term capital loss can be set off against either short-term or long-term capital gain

- Losses on VDAs cannot be set off against any income, including other VDA gains

- Losses on listed equity STCG and LTCG follow the standard intra-head rules

Inter-head set-off rules

Capital losses (other than VDA) cannot be set off against salary, business income or other heads. They can only flow within the capital gains head. House property losses, in contrast, can be set off against other heads up to Rs.2,00,000 per year.

Carry-forward window

Unabsorbed capital losses can be carried forward for eight assessment years immediately following the year in which the loss was first computed. The return for the loss year must be filed by the original due date; a belated return forfeits the carry-forward for most loss categories.

Worked example: equity portfolio with mixed holding periods

A typical Indian retail investor’s tax computation rarely involves a single transaction.

Setup

FY 2025-26 transactions: STCG of Rs.80,000 from listed equity sold within 6 months; LTCG of Rs.2,00,000 from equity mutual funds held over 12 months; capital loss of Rs.40,000 from listed equity sold short-term; capital loss of Rs.20,000 from a VDA sale.

Step-by-step computation

STCG net of intra-head loss: Rs.80,000 minus Rs.40,000 = Rs.40,000. Tax at 20% under Section 111A = Rs.8,000. LTCG of Rs.2,00,000 net of the Rs.1,25,000 exemption = Rs.75,000 taxed at 12.5% = Rs.9,375. VDA loss of Rs.20,000 cannot be set off and lapses. Total capital gains tax = Rs.17,375 plus 4% cess.

Where filers go wrong

The most common error is trying to net the Rs.20,000 VDA loss against the equity STCG. Section 115BBH does not permit this, and CPC will add back the netting in a 143(1) intimation.

Surcharge and cess on capital gains

Headline rates are only part of the story.

Health and education cess

A 4% health and education cess applies on the tax plus surcharge, across all heads of income, including capital gains. The cess is non-negotiable.

Surcharge cap of 15% on Section 112A and 111A

Surcharge on LTCG under Section 112A and STCG under Section 111A is capped at 15%, even when the rest of the taxpayer’s income would otherwise attract 25% or 37% surcharge. This is one of the structural reasons listed equity remains a tax-efficient holding above the 12-month mark.

Marginal relief

For income that crosses a surcharge band by a small amount, marginal relief brings down the surcharge so the additional tax does not exceed the additional income. The relief is computed at the return level, not per asset.

Common mistakes when computing capital gains

The same pattern of mistakes recurs every filing season.

Treating brokerage and STT as deductible costs

Brokerage and exchange charges are part of cost of transfer and are deductible from sale consideration. STT, however, is not deductible in the capital gains computation, although it is the price paid for the favourable Section 111A and 112A rates.

Forgetting the Rs.1,25,000 LTCG exemption

The first Rs.1,25,000 of LTCG under Section 112A is exempt in the year. Many filers report gross LTCG without applying the exemption, overpaying tax until they file a revised return.

Misclassifying debt fund redemptions

Debt mutual fund units purchased on or after April 1, 2023 are taxed at slab rates without any long-term carve-out. Filers who continue to apply the older 20% with indexation rate to post-April-2023 units file an incorrect return.

Ignoring AIS for capital gains

AIS now reports broker and AMC transactions extensively. Returns that under-report capital gains relative to AIS are tagged for CPC follow-up.

Advanced moves: harvesting and reinvestment

Capital gains is one of the few heads where year-end planning still helps.

Tax-loss harvesting

Booking losses on selected positions before year-end, while keeping the underlying allocation similar through replacement instruments, can absorb gains in the same year. The 30-day wash-sale concept is not codified in India, but artificial transactions can be challenged.

Section 54EC bonds for property gains

LTCG from immovable property can be invested in bonds of NHAI, REC and similar issuers under Section 54EC, up to a cap of Rs.50,00,000 per financial year per filer, for an exemption. The lock-in is five years, and the interest is taxable.

Reinvestment under Section 54 and 54F

Section 54 covers reinvestment of house-property LTCG in another residential property. Section 54F covers reinvestment of LTCG from any other long-term asset in a residential property. Both have specific timing windows and conditions that must be matched.

Frequently asked questions

What is the LTCG rate on listed equity for FY 2025-26?

Long-term capital gains on listed equity and equity mutual funds above the Rs.1,25,000 exemption are taxed at 12.5% under Section 112A. Holding period for long-term classification is more than 12 months.

Is indexation still available on property sales?

For resident individuals and HUFs who acquired the property before July 23, 2024, the option to use 20% with indexation alongside the new 12.5% without indexation has been retained. For all other property sales, indexation is no longer available.

How are debt mutual funds taxed now?

Specified debt mutual fund units purchased on or after April 1, 2023 are taxed at slab rates regardless of holding period. Indexation is not available, and there is no long-term carve-out.

Can crypto losses be set off against crypto gains?

Section 115BBH does not allow VDA losses to be set off against other income, and the prevailing position restricts set-off against other VDA gains and forbids carry-forward. Filers should not assume any netting until the law explicitly permits it.

How long can capital losses be carried forward?

Capital losses, other than VDA losses, can be carried forward for eight assessment years following the loss year. The return for that year must be filed by the original due date; a belated return forfeits carry-forward.

Related guides on Section 54EC bonds, tax-loss harvesting, and the VDA reporting framework from April 2026 are forthcoming on this site.