The 1 percent TDS crypto India regime, set out in Section 194S of the Income Tax Act, is the most frequently misunderstood part of the country’s crypto-tax framework. It sits on top of the 30% flat tax under Section 115BBH but is not itself the final tax. It is a withholding mechanism: every time you transfer a virtual digital asset above the threshold, 1% of the gross consideration is held back by the buyer and deposited with the government against your PAN.

That money is not gone. It shows up in your Form 26AS and AIS, and you claim it as a credit when you file your Income Tax Return. If your final tax bill is lower than the total TDS, the excess flows back as a refund, usually three to nine months after the return is processed. This guide walks through the mechanics, the thresholds, the per-transaction math, the 26AS reconciliation, and the refund path step by step. Crypto carries leveraged volatility risk; do not invest more than you can afford to lose.

Section 194S: The Legal Spine of 1 Percent TDS Crypto

Section 194S was inserted into the Income Tax Act by the Finance Act 2022 and took effect from July 1, 2022. The recodified Income Tax Act 2025 retained it without a change in rate or scope.

What the section actually requires

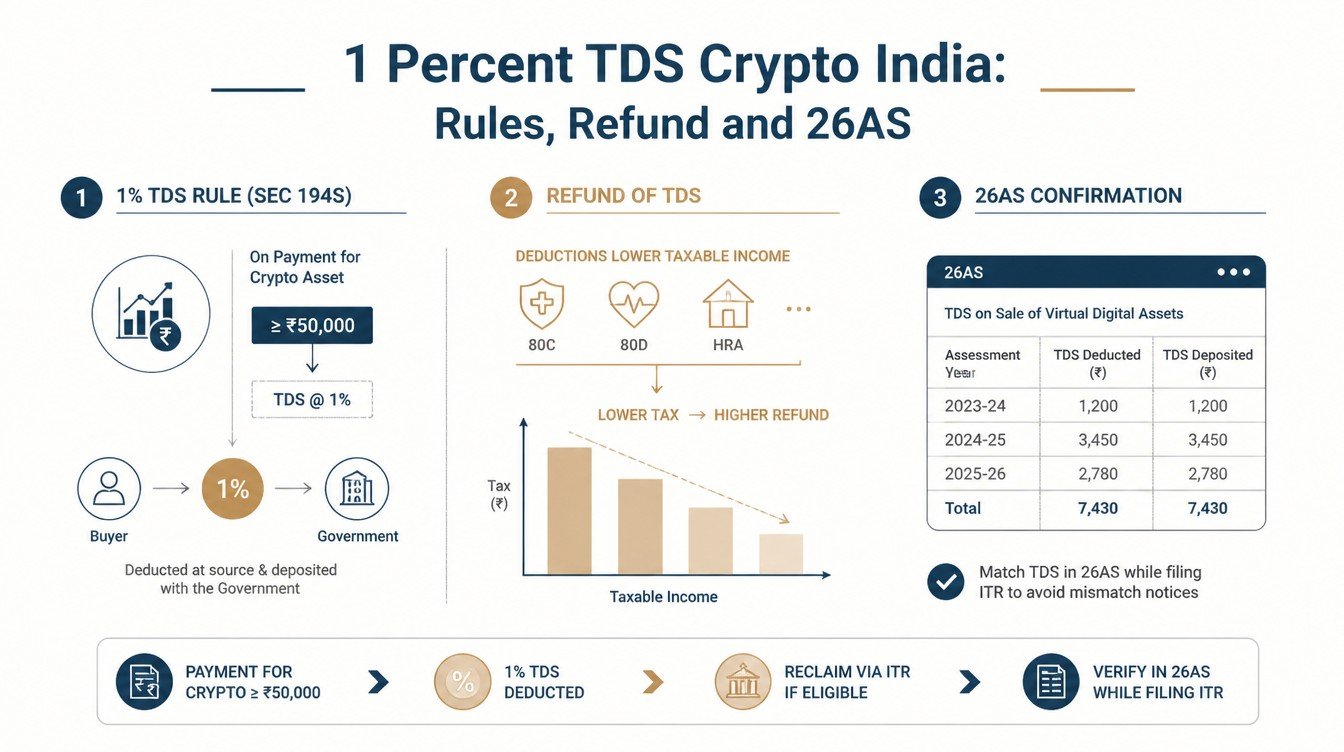

Any person responsible for paying consideration in connection with the transfer of a virtual digital asset to a resident must deduct an amount equal to 1% of the consideration as income tax, at the time of credit of such sum to the account of the resident or at the time of payment, whichever is earlier.

Who deducts and who receives

On a domestic crypto exchange, the exchange itself is the deductor. It withholds 1% of the gross sale value at the point of the transfer, pays the net amount to the seller, and deposits the 1% with the Central Board of Direct Taxes within the prescribed timeline. For peer-to-peer trades and for transactions on platforms that do not deduct, the buyer is legally responsible.

Why TDS exists when there is already an income tax

The withholding is a compliance net. The 30% tax under Section 115BBH is the final tax, but it is computed and paid only when the taxpayer files the return. Section 194S ensures the government has at least some collection from every transaction, in real time, and creates a paper trail that surfaces in 26AS and AIS regardless of whether the taxpayer ultimately files.

The Threshold: Rs.50,000 and Rs.10,000

The 1 percent TDS crypto India rule does not apply to every trade. The Income Tax Act sets two threshold figures based on who the seller is.

Rs.50,000 per year for “specified persons”

For individuals and HUFs whose business or profession is not subject to tax audit, and whose total business turnover does not cross Rs.1 crore (business) or Rs.50 lakh (profession) in the preceding year, the threshold is Rs.50,000 of aggregate consideration in a financial year. Most retail investors fall into this category.

Rs.10,000 per year for everyone else

For all other persons, including companies, larger businesses, and audited professionals, the threshold is Rs.10,000 of aggregate consideration in a financial year. The lower threshold reflects the policy intent of capturing institutional and high-volume activity earlier.

How thresholds are tracked

The threshold is computed cumulatively across the financial year on the platform. Once your total crypto trade value on a given exchange crosses Rs.50,000 (or Rs.10,000), every subsequent trade is subject to the 1% withholding. Most domestic exchanges apply the deduction from the first transaction by default, treating the threshold as crossed.

Per-Transaction TDS Math: Three Worked Examples

Numbers make the mechanism real. The following three cases cover the most common patterns.

Example 1: Simple sale of Bitcoin

Anjali sells Bitcoin worth Rs.2,00,000 on a domestic exchange in June 2025. The TDS is 1% of Rs.2,00,000 = Rs.2,000. The exchange credits Rs.1,98,000 to her bank account and deposits Rs.2,000 with the CBDT against her PAN. The Rs.2,000 appears in her Form 26AS within four to six weeks.

Example 2: Loss-making sale of Ether

Bharath sells Ether worth Rs.1,50,000 in August 2025. He had bought the same Ether for Rs.1,80,000 earlier, so he is sitting on a Rs.30,000 loss. The TDS is still 1% of Rs.1,50,000 = Rs.1,500, deducted from the gross consideration. The TDS does not care whether the trade is profitable; it is on the sale value, not on the gain.

Example 3: Crypto-to-crypto swap

Charita swaps Bitcoin worth Rs.3,00,000 for Ether worth Rs.3,00,000 on a domestic exchange in November 2025. Section 194S applies on both legs: the exchange withholds 1% of Rs.3,00,000 = Rs.3,000, typically by deducting from the receivable side. The full Rs.3,00,000 of consideration is also subject to 30% tax under Section 115BBH on the gain over Charita’s cost in Bitcoin.

| Trade | Gross sale value | 1% TDS | Net received |

|---|---|---|---|

| Anjali (Bitcoin sale) | Rs.2,00,000 | Rs.2,000 | Rs.1,98,000 |

| Bharath (Ether loss sale) | Rs.1,50,000 | Rs.1,500 | Rs.1,48,500 |

| Charita (BTC-ETH swap) | Rs.3,00,000 | Rs.3,000 | Rs.2,97,000 worth of Ether |

Form 26AS and AIS Reconciliation

Once TDS is deducted, the entry must surface in your tax credit statements. Reconciling these statements before you file is the single most useful pre-filing habit you can build.

Form 26AS

Form 26AS is the consolidated annual tax credit statement linked to your PAN. Every TDS deducted under Section 194S by every deductor appears here, typically within four to six weeks of the quarter end. The entry shows the deductor’s TAN, the section code (194S), the date, and the amount.

Annual Information Statement (AIS)

The AIS is a broader information statement that includes 26AS data plus transaction-level disclosures from exchanges and other reporting entities. From the April 1, 2026 Section 509 reporting cycle onward, the AIS will carry trade-level VDA entries with timestamps, asset names, and INR values. The AIS is where your Schedule VDA filing will be cross-checked.

What to do if an entry is missing

If your TDS deduction is visible in your exchange statement but not in 26AS, contact the exchange’s tax-helpline in writing and ask for the deposit challan reference. If the entry is in 26AS but not on your exchange statement, retain a screenshot of both for your records and reconcile against your bank credit. Persistent mismatches should be flagged through the AIS feedback module on the income-tax portal before you file.

How TDS Translates Into a Refund

The refund flow is the part most retail investors get wrong, mainly because they assume the 1% is the final tax. It is not.

The basic logic

Total final tax for the year = (30% of net VDA gains) + (4% cess) + (any applicable surcharge). Total TDS for the year = (1% of every taxable gross consideration on the deductor’s platform). If total TDS is less than total final tax, you pay the balance via Challan 280 before filing. If total TDS exceeds total final tax, the excess flows back as a refund.

When TDS commonly exceeds tax

The 1% TDS is on gross consideration; the 30% tax is on net gain. For thin-margin or loss-making trades, the 1% on gross can exceed the 30% on the (smaller or negative) gain. Active traders who churn the same capital many times in a year often build a TDS credit that exceeds their final tax bill.

The refund timeline

Refunds are processed after the Income Tax Department processes your return under Section 143(1), which typically takes three to nine months from the filing date. The refund is credited to the bank account validated in your ITR. There is no automatic interest until the delay crosses the statutory period (Section 244A), after which interest is added at the prescribed rate.

A Full Refund Walkthrough: From Trade to Bank Credit

A concrete end-to-end example pulls the moving parts together.

Step 1: The trades

Devika, a Mumbai-based product manager, made the following crypto trades in FY 2025-26: she sold Bitcoin for Rs.5,00,000 (gain Rs.50,000), sold Ether for Rs.3,00,000 (loss Rs.30,000), and swapped Solana worth Rs.2,00,000 for Polygon (gain Rs.20,000 on the Solana leg). Total gross consideration on sales: Rs.10,00,000. Total gain (positive-only, per Section 115BBH): Rs.70,000.

Step 2: The TDS computation

The domestic exchange withheld 1% on every transfer above the threshold. Total TDS deducted: Rs.10,000 (1% of Rs.10,00,000). The Rs.10,000 appears in Devika’s Form 26AS and AIS.

Step 3: The income tax computation

Tax at 30% on Rs.70,000 = Rs.21,000. Cess at 4% = Rs.840. Total VDA tax = Rs.21,840. The Ether loss of Rs.30,000 is irrelevant for tax purposes under Section 115BBH(2).

Step 4: The settlement

Devika’s TDS (Rs.10,000) is less than her final tax (Rs.21,840). She pays the shortfall of Rs.11,840 via Challan 280 before filing, claims the Rs.10,000 as a credit in Schedule TDS, and submits the return. No refund is due in this case; the balance was paid as self-assessment tax.

Step 5: When the math flips

Had Devika’s gains been only Rs.10,000 in total, her final tax would be 31.2% of Rs.10,000 = Rs.3,120. With TDS of Rs.10,000 already deducted, she would be entitled to a Rs.6,880 refund, which would arrive after the department processes her return.

Common TDS Mistakes and How to Avoid Them

Several patterns of confusion recur across thousands of crypto returns reviewed every year.

Assuming 1% TDS is the final tax

It is not. Section 194S is a withholding; Section 115BBH is the final tax. Failing to file a return on the assumption that “TDS has been deducted, so I’m done” forfeits the credit and exposes the taxpayer to non-filer notices.

Not reconciling TDS against 26AS

If the exchange deducted Rs.10,000 but only Rs.7,000 appears in 26AS, the missing Rs.3,000 cannot be claimed without producing the deduction certificate. Reconciliation should happen quarterly, not just before filing.

Forgetting TDS on peer-to-peer or offshore trades

If you bought crypto from another individual without going through an exchange, you (the buyer) are legally responsible for deducting and depositing 1% TDS. The same applies to purchases on offshore exchanges that do not deduct. Missing this creates both a deductor-side default and a complication when claiming credit.

Claiming TDS in the wrong assessment year

TDS is claimed in the assessment year corresponding to the financial year of deduction. A deduction made in March 2026 belongs to AY 2026-27 and cannot be shifted to AY 2027-28 to align with a later sale. Match the year of the 26AS entry to the year of the return.

The TDS Refund Path Step by Step

For investors expecting a refund, the cleanest path is procedural rather than analytical.

- Download Form 26AS and AIS for FY 2025-26 from the income-tax portal after April 15, 2026, when the final quarter’s deductions should be visible.

- Cross-tally each TDS entry against your exchange’s tax statement; flag discrepancies in writing to the exchange.

- Calculate your final tax: 30% of (sum of positive-gain VDA transactions), plus 4% cess, plus any surcharge.

- Compute the gap: total TDS minus total tax. A positive gap is your expected refund.

- Open the appropriate ITR (ITR-2 for non-business filers, ITR-3 for those with business income), fill Schedule VDA row by row, and populate Schedule TDS with the 26AS entries.

- Validate the bank account marked for refund on the e-filing portal; an invalid or pre-validated-but-changed account is a common refund-delay reason.

- Submit the return well before the July 31 deadline; earlier filings get processed faster.

- Track the refund status through the “Refund / Demand Status” tab on the portal. If the refund is delayed beyond six months, raise a grievance with the assessing officer.

How the 1% TDS Connects to the April 2026 Reporting Rule

The TDS regime, the 30% income tax, and the new exchange-reporting framework form a closed loop.

The reporting layer reinforces the TDS layer

From April 1, 2026, exchanges must file user-level transaction statements with the IT Department under Section 509. The TDS deducted under Section 194S is one of the line items in each statement. A TDS entry on your exchange statement that does not match the AIS entry will surface as a flagged row before you even open the ITR utility.

What this means for cash-flow planning

Investors who churn capital several times a year build up a meaningful TDS credit, which can take three to nine months to refund. Building working-capital plans around the post-deduction net (rather than the gross) is the only realistic approach. Crypto carries leveraged volatility risk; do not invest more than you can afford to lose, and do not assume locked-up TDS will return on a fast timeline.

Frequently Asked Questions

Is the 1% TDS the same as the 30% crypto tax?

No. The 1% TDS under Section 194S is a withholding on every transfer of a VDA, deducted at source by the buyer or exchange. The 30% tax under Section 115BBH is the final income tax on net VDA gains, paid at the time of filing. The TDS is creditable against the final tax.

What is the threshold for 1% TDS on crypto in India?

For specified persons (most individual and HUF investors not subject to tax audit), the threshold is Rs.50,000 of aggregate consideration in a financial year on a given deductor’s platform. For all other persons, including companies and audited businesses, the threshold is Rs.10,000 of aggregate consideration in a financial year.

How do I claim my crypto TDS back as a refund?

Reconcile the TDS in your Form 26AS and AIS, compute your final tax under Section 115BBH (30% of net positive gains plus cess and surcharge), and file the appropriate ITR with Schedule VDA and Schedule TDS populated. If TDS exceeds final tax, the excess is refunded by the Income Tax Department after processing, typically within three to nine months.

Can I avoid the 1% TDS by using an offshore exchange?

No. Section 194S applies to the consideration paid for the transfer of a VDA to a resident. If you transact through an offshore exchange that does not deduct, the buyer in India is legally responsible for deducting and depositing the 1%. Skipping the deduction is a deductor-side default and does not eliminate the underlying liability.

Does the 1% TDS apply on crypto-to-crypto swaps?

Yes. A swap is a transfer of a VDA and falls within Section 194S. Domestic exchanges typically apply the 1% withholding on the asset given up, valued at the swap-timestamp INR equivalent. Both the swap-in leg and the swap-out leg can independently trigger TDS depending on the platform’s mechanism.

Related LearnFineEdge guides on Section 115BBH, Schedule VDA filing, and Indian crypto exchanges are forthcoming and will be linked here as the cluster expands.