Non-fungible tokens have moved from being a niche corner of the digital-asset world to a category that Indian tax law has had to define and treat explicitly. The Income Tax Act, 1961, through Section 115BBH and the broader Virtual Digital Asset (VDA) framework, has brought NFTs within scope of the 30 percent flat-rate tax that applies to crypto gains, along with the same restrictions on loss set-off and the 1 percent TDS on transfers. For Indian creators, collectors, and investors evaluating nft tax india 2026 consequences, the framework is now well-defined in its core, with some genuine ambiguity at the edges (collectibles, royalty income for creators, foreign-platform transactions). Crypto carries leveraged volatility risk; do not invest more than you can afford to lose.

This guide walks through the VDA definition that brings NFTs into the tax net, the specific treatment under Section 115BBH, the unresolved questions around collectible NFTs and creator royalties, and the reporting obligations in Schedule VDA of the income-tax return. The framework applies to FY 2025-26 returns and onwards, with reference to current notifications.

The VDA Definition and Why NFTs Are Included

The starting point for understanding NFT tax in India is the Virtual Digital Asset definition introduced in the Finance Act, 2022 and refined since.

The statutory definition

Under Section 2(47A) of the Income Tax Act, 1961, a Virtual Digital Asset means any information, code, number, or token (not Indian currency or foreign currency) generated through cryptographic means or otherwise, providing a digital representation of value, that is exchanged with or without consideration, and includes a non-fungible token or any other token of similar nature, by whatever name called. The explicit inclusion of NFTs in the definition removed the earlier ambiguity about whether NFTs were taxed differently from fungible crypto.

The CBDT notifications

CBDT has issued notifications specifying the types of NFTs and other digital tokens that fall within the VDA definition, with carve-outs for certain digital representations that the government does not intend to bring under the VDA regime (typically gift cards, loyalty points, and certain other non-investment digital tokens). The notifications evolve; the operative position should always be cross-checked against the latest CBDT release.

What is not a VDA

Digital representations of value that are not generated through cryptographic means and that do not have an investment or speculative character (digital gift cards, store credits, frequent-flier miles) are typically outside the VDA definition. Domain names, software licences, and similar digital products that represent specific utility rather than transferable speculative value are also typically outside.

Why NFTs are clearly in

The text of the VDA definition explicitly names non-fungible tokens. The CBDT notifications confirm the inclusion. The tax treatment of NFT transfers therefore mirrors the treatment of cryptocurrency transfers, with the same 30 percent rate, the same restrictions on losses, and the same TDS framework.

Section 115BBH: The Core Tax Treatment

Section 115BBH of the Income Tax Act, 1961 is the operative provision for taxing gains on the transfer of VDAs, including NFTs.

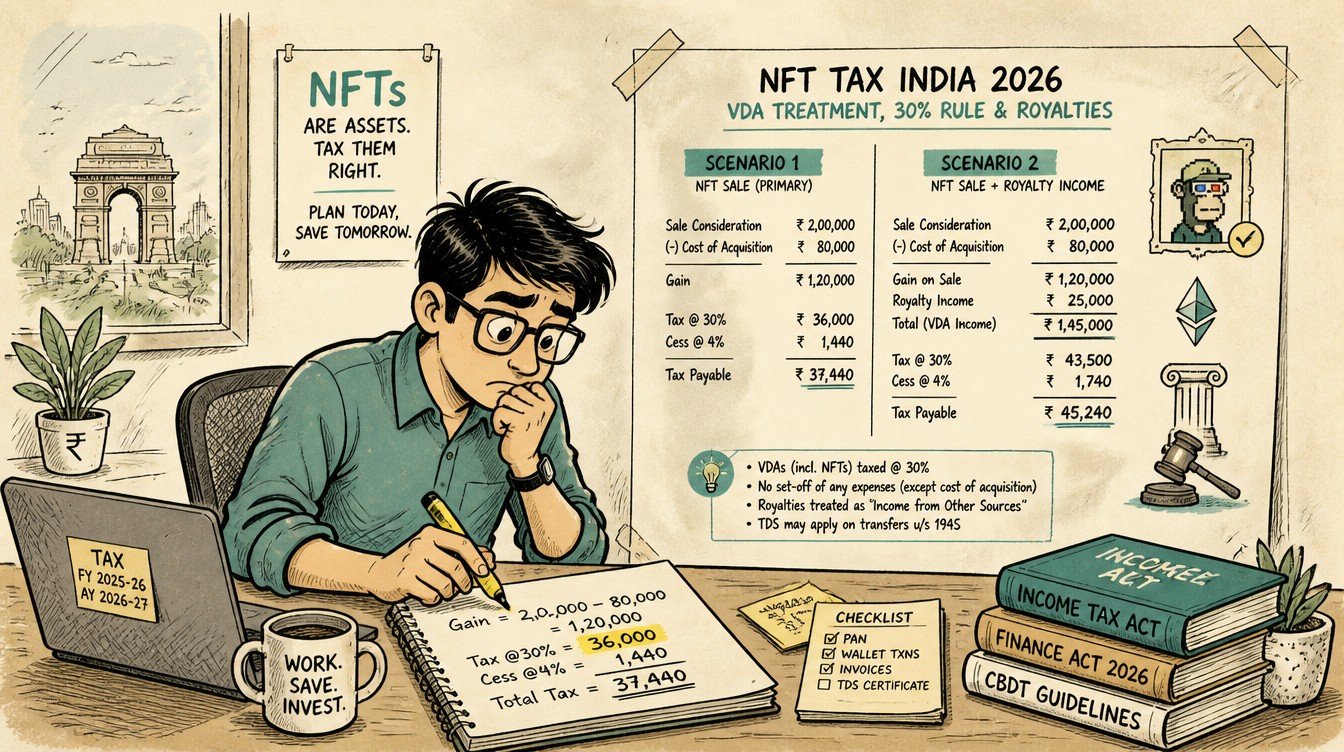

The 30 percent flat rate

Gains from the transfer of a VDA are taxed at a flat rate of 30 percent, plus applicable surcharge and a 4 percent health and education cess. The 30 percent applies regardless of the taxpayer’s overall income slab. A taxpayer in the 5 percent slab and a taxpayer in the 30 percent slab pay the same flat rate on VDA gains.

The acquisition-cost-only deduction

The only deduction permitted against the gross consideration on transfer is the cost of acquisition. Other expenses (gas fees, exchange charges, mining costs, professional fees for advice) are not deductible. The narrow deduction makes the effective tax burden materially higher than the headline 30 percent might suggest, particularly for active traders or creators incurring significant operational costs.

The no-loss-set-off rule

Losses on the transfer of one VDA cannot be set off against gains from any other source, including gains from other VDAs. Each VDA transaction is taxed in isolation; a loss on one NFT cannot offset a gain on another NFT, even within the same financial year. Losses cannot be carried forward to subsequent years. This is the structural feature that makes active VDA trading much harder under Indian tax than under most other Indian asset classes.

The 1 percent TDS overlay

Section 194S requires a 1 percent TDS deduction on the consideration paid for the transfer of a VDA, by the buyer or by the exchange acting on behalf of the buyer, subject to defined thresholds. The TDS is creditable against the seller’s final tax liability, but the cash-flow impact is real. For high-frequency NFT trading, the cumulative TDS deductions can be a meaningful working-capital drag.

The Ambiguity Around Collectible NFTs

Within the broad VDA framework, certain categories of NFTs sit at the boundary of the definition and generate practical interpretation issues.

Pure-art and collectible NFTs

The CBDT notifications have, in some communications, suggested that NFTs whose underlying value is in a transferable physical asset or in a digital representation that does not have a speculative or investment character may fall outside the VDA definition. The application of this principle to digital art NFTs (where the underlying is the digital file itself, with no physical or utility component) is not fully settled in case law or in clarificatory notifications.

Utility NFTs

NFTs that primarily provide access to a service, a membership, or a digital experience (game items, event tickets, membership passes) raise the question of whether their transfer is a transfer of a VDA or a transfer of a service-access right. The practical answer in most cases has been to treat them as VDAs, but the area is under interpretation.

NFTs representing physical assets

NFTs that tokenise ownership of a physical asset (a piece of art, a watch, a property fraction) raise the question of whether the tax applies to the NFT transfer or to the underlying asset. The conservative position is to treat both as separate taxable events: the VDA transfer (under 115BBH) and the underlying asset transfer (under the rules applicable to that asset class). The double-treatment can be costly; specific transactions should be reviewed with a qualified tax professional.

The safer default

Given the unsettled boundary, the safer default for most Indian NFT holders is to treat all NFT transfers as VDA transfers under Section 115BBH, report them in Schedule VDA, and pay the 30 percent tax on gains. The cleaner tax position avoids the audit-and-dispute exposure that aggressive interpretation invites.

Creator Royalty Tax Treatment

A particularly important case for Indian NFT creators is the tax treatment of secondary-market royalties, which is a distinct income stream from the initial mint sale.

The primary mint sale

When an artist mints and sells an NFT for the first time, the sale consideration less the cost of creation (in the limited sense that 115BBH allows) is taxed at 30 percent. The creator’s input costs (software, services, time) are largely non-deductible under the strict 115BBH framework, which is harsher than the treatment that would apply if the same income were professional or business income.

The royalty on secondary sales

Many NFT smart contracts include automatic royalty provisions: every secondary-market sale of the NFT routes a percentage (typically 5 to 10 percent) to the original creator’s wallet. The Indian tax treatment of these recurring royalty payments under Section 115BBH is still subject to interpretation. One view treats each royalty receipt as a fresh VDA transfer (consideration with no acquisition cost), taxable at 30 percent. Another view treats it as royalty income under the normal slab-rate provisions.

The conservative position for creators

Until specific clarificatory notifications resolve the question, the conservative position for creators is to treat secondary-market royalties as VDA-related receipts under Section 115BBH at 30 percent. This may be a less favourable treatment than slab-rate royalty income for creators in lower tax brackets, but it avoids the litigation risk associated with the aggressive position. Working with a qualified tax professional on the specific reporting is recommended.

The business-of-NFTs question

Section 115BBH overrides other provisions, which means that even if the creator’s NFT activity has the character of a business (regular minting, regular sales, professional setup), the 30 percent rate applies. The creator cannot opt to be taxed under the more favourable “business income” provisions that would allow deduction of business expenses. The override is one of the more frequently flagged inequities in the current VDA tax framework.

The Reporting Side: Schedule VDA in the ITR

Schedule VDA, introduced as a dedicated schedule in the income-tax return, is the primary reporting mechanism for VDA transactions including NFT transfers.

What goes in Schedule VDA

Schedule VDA requires the taxpayer to disclose, for each VDA transaction during the financial year, the fields listed below.

- Date of transfer.

- Asset description, with NFT details where relevant.

- Consideration received.

- Cost of acquisition.

- Gain or loss on the transaction.

- Any TDS deducted under Section 194S.

The schedule is granular and assumes the taxpayer has maintained transaction-level records.

The data source problem

For NFT transactions on decentralised marketplaces, the taxpayer often does not have a clean transaction statement equivalent to what a centralised exchange would provide. The taxpayer is responsible for compiling the transaction history from on-chain records, wallet transactions, and any platform receipts. Maintaining a contemporaneous spreadsheet of every NFT minted, bought, sold, or transferred is the cleanest path; reconstructing the history at filing time is materially harder.

The cross-check with Form 26AS and AIS

TDS deducted under Section 194S by Indian exchanges appears in Form 26AS and the Annual Information Statement (AIS). The taxpayer should reconcile every TDS entry against their own records. A mismatch is a flag that the underlying transaction may not have been captured in the taxpayer’s records, which can create issues at scrutiny.

The foreign-platform challenge

NFT transactions on foreign platforms (OpenSea, foreign decentralised marketplaces) do not have Section 194S TDS deducted by the platform, but the gains are still taxable in India for resident taxpayers. The reporting onus is entirely on the taxpayer. Foreign-platform NFTs may also trigger Schedule FA disclosure (foreign assets) if the holding constitutes a foreign asset under the framework. The reporting complexity is one of the structural costs of foreign-platform NFT activity.

The Practical Tax Implication for Common Scenarios

The combined effect of Section 115BBH, the 1 percent TDS, and the limited deductions can be summarised in a few common scenarios.

The summary table

| Scenario | Tax treatment |

|---|---|

| Buy NFT for Rs.50,000, sell for Rs.1,00,000 | 30 percent tax on Rs.50,000 gain, plus 4 percent cess, plus surcharge if applicable; 1 percent TDS at the time of purchase |

| Buy NFT for Rs.1,00,000, sell for Rs.50,000 | No tax payable (loss); loss cannot be set off against other gains; TDS may have been deducted at purchase but no refund of the TDS as such (creditable against final tax) |

| Mint and sell own-created NFT for Rs.2,00,000 | 30 percent tax on the full Rs.2,00,000 (minimal cost-of-acquisition deductible); cess and surcharge apply |

| Receive Rs.10,000 royalty on a secondary-market sale | Conservative treatment: 30 percent tax on the full Rs.10,000 as VDA receipt; alternative treatment as royalty income at slab rate is contested |

| Gift an NFT to a relative | Gift treatment under Section 56(2)(x) for the recipient if the value crosses the relevant threshold; the donor’s basis carries to the recipient for the future gain computation |

| Trade an NFT for another NFT (barter) | Each side is a transfer for tax purposes, with the consideration being the fair market value of the asset received; each side is taxed at 30 percent on the respective gains |

The cumulative effect on active traders

An active NFT trader who has 20 winning trades and 10 losing trades in a year pays 30 percent tax on each of the 20 wins individually, with no offset from the 10 losses. The losses are economic losses to the trader but do not appear in the tax computation. This structural feature means the effective tax rate on a portfolio of NFT activity is often substantially higher than 30 percent of net gains.

The implication for portfolio strategy

The no-loss-set-off rule makes long-hold, low-turnover NFT strategies materially more tax-efficient than active trading. A long-hold strategy crystallises a single net gain at sale, on which 30 percent applies. An active-trade strategy generates multiple gross gains on each of which 30 percent applies, with no credit for the offsetting losses.

Common Mistakes Indian NFT Holders Make on Tax

The same handful of mistakes show up in NFT tax filings across the early years of the VDA framework.

Not maintaining contemporaneous records

The most common mistake is failing to record every NFT transaction at the time it happens. Reconstructing the history months later from on-chain data and wallet activity is laborious, error-prone, and often produces a tax position that the taxpayer cannot fully defend at scrutiny. Maintain a spreadsheet from day one.

Treating NFT activity as professional income to claim expenses

Some creators with significant operational costs try to report NFT income as professional income to claim expenses. Section 115BBH overrides this; the 30 percent rate applies regardless. The aggressive position invites scrutiny, demand notice, and penalty exposure, with little upside.

Ignoring foreign-platform transactions

NFT trades on foreign platforms without TDS deduction are sometimes treated by holders as “off-radar” because there is no automatic flag in Form 26AS. The tax obligation exists regardless of TDS; the holder is responsible for self-reporting and self-paying. The risk of later scrutiny based on foreign asset disclosures is real.

Not adjusting for the TDS in advance-tax computation

Section 194S TDS deducted by Indian exchanges is creditable against final tax liability but does not eliminate it. Holders who treat the TDS as the final tax and skip advance-tax computation can find themselves with a 234A and 234C exposure at filing time. The TDS is a payment-on-account, not the final discharge.

FAQ

Is my NFT taxed the same way as my Bitcoin or Ether holdings?

Yes. NFTs are explicitly included in the Virtual Digital Asset definition under Section 2(47A) of the Income Tax Act, and gains on NFT transfers are taxed under Section 115BBH at the flat 30 percent rate plus cess and surcharge, with only the cost of acquisition deductible. The same 1 percent TDS under Section 194S applies to NFT transfers as it does to cryptocurrency transfers, subject to the relevant thresholds.

If I create and sell my own NFT, can I deduct my time and software costs?

Under the strict reading of Section 115BBH, only the cost of acquisition is deductible. Operational costs incurred by the creator (software, services, professional fees, time) are not deductible against VDA gains. This makes the effective tax burden on creators particularly heavy. The position is one of the items the industry has lobbied to amend; the operative provision in force should be verified before filing.

Can I set off the loss on one NFT against the gain on another NFT?

No. Under Section 115BBH, losses on the transfer of any VDA cannot be set off against gains from any other source, including gains from other VDAs. Each transaction is taxed independently on its own gain; losses are not aggregated. Loss positions are economic losses but do not appear in the tax computation as offsets.

What happens if I receive an NFT as a gift?

The recipient is subject to Section 56(2)(x) treatment for gifts: gifts above the relevant threshold from non-relatives are taxable in the recipient’s hands at the fair market value at the time of receipt. Gifts between specified relatives are not subject to gift tax. The recipient’s cost of acquisition for any subsequent transfer is generally the value at which the gift was taxed (or the donor’s cost in cases where no gift tax was paid).

Should I voluntarily report my foreign-platform NFT activity?

Yes. The tax obligation exists regardless of whether the platform deducts TDS in India. Voluntary disclosure through the regular ITR (Schedule VDA for the transactions, plus Schedule FA where applicable for foreign-asset reporting) is materially safer than the later-discovery scenario, which can attract penalties under multiple provisions including the Black Money Act for undisclosed foreign assets. The disclosure cost is the tax due; the non-disclosure cost can be many multiples of that.

Related guides on this topic are coming to learnfinedge.com soon.