If you bought, sold, swapped, or earned any virtual digital asset (VDA) during FY 2025-26, the crypto tax India 2026 regime now governs every rupee of that activity, and the rules are far stricter than they were when retail traders first piled into Bitcoin in 2020. The flat 30% tax under Section 115BBH, the 1% TDS under Section 194S, and the new Schedule VDA disclosure inside the Income Tax Return form together create a closed-loop system: your exchange tells the Income Tax Department what you did, you tell the same department what you earned, and any mismatch becomes a notice.

Add the April 1, 2026 exchange-reporting mandate, the Rs.200-per-day penalty for non-reporting platforms, and the up-to-Rs.50,000 charge for incorrect disclosure, and the message is clear: there is no quiet corner of the Indian crypto market left. This guide walks through the math, the mechanics, the worked examples, and the mistakes that turn a routine return into a scrutiny case. Crypto carries leveraged volatility risk; do not invest more than you can afford to lose.

What the Crypto Tax India 2026 Framework Actually Covers

The first surprise for most beginners is how wide the net is. The Income Tax Act, through the definition inserted by the Finance Act 2022 and tightened in the Income Tax Act 2025, treats any “virtual digital asset” as taxable property. That definition pulls in not just Bitcoin and Ether but every token, every stablecoin, every play-to-earn reward, and every NFT that meets the statutory test.

Who is a “VDA” holder in the eyes of the law

A salaried professional who buys Rs.10,000 of crypto on a domestic exchange is a VDA holder. So is a freelancer who accepts USDT for a foreign client, a gamer who receives an NFT drop, and a retiree who inherits a wallet. The label does not depend on volume; it depends on the asset.

What transactions trigger tax

Any “transfer” of a VDA is a taxable event. That includes a sale for INR, a swap between two coins, a payment made in crypto, and a gift sent to a non-relative. Even moving tokens from a centralised exchange to your own wallet does not trigger tax on its own, but selling those tokens later certainly does.

What changed between Budget 2022 and Budget 2026

The 30% rate, the 1% TDS, the no-set-off rule, and the no-expense-deduction rule were all introduced in Budget 2022. Budget 2026 left those four pillars untouched but added the exchange-reporting regime, Schedule VDA enforcement, and the new penalty section that goes live on April 1, 2026. The era of “I will sort it out later” is over.

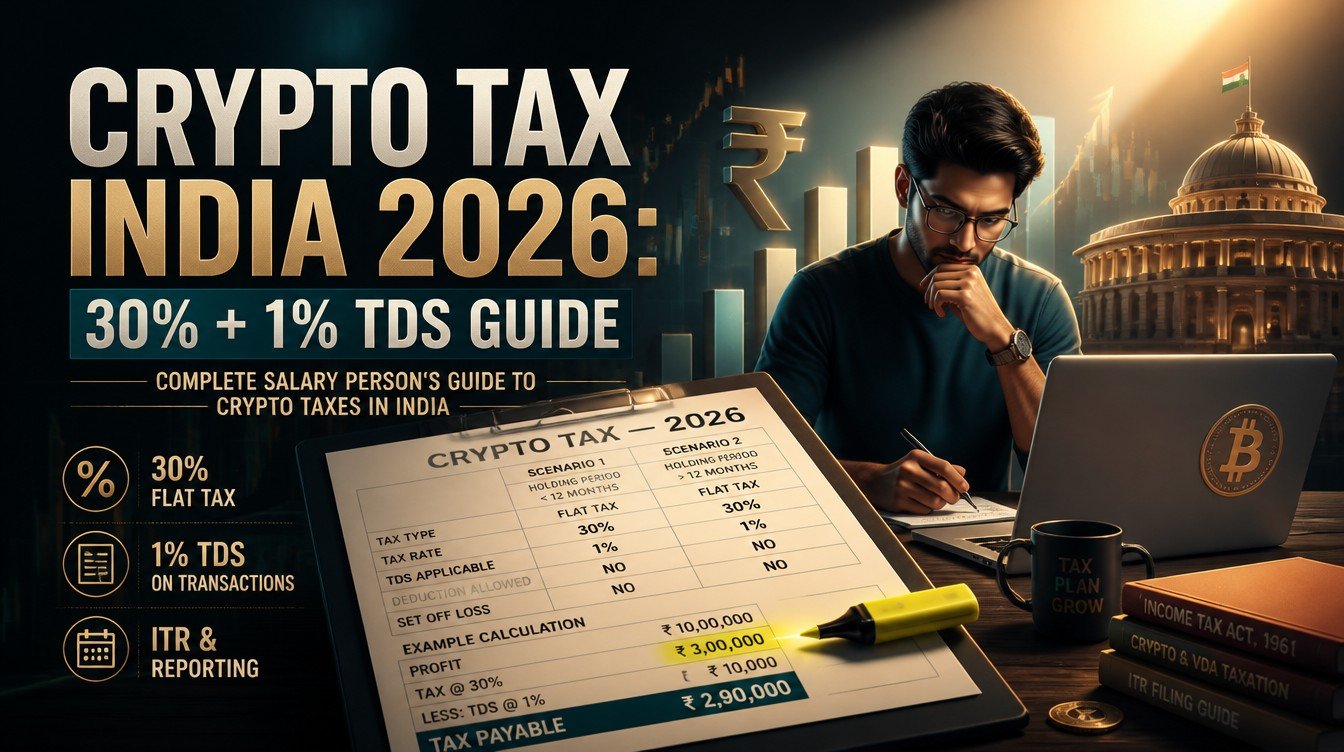

Section 115BBH: The 30% Math, Cess, and Surcharge

Section 115BBH is the engine of the crypto tax India 2026 regime. It imposes a flat 30% tax on income from the transfer of any VDA, regardless of your other income, regardless of whether you held the coin for one day or five years, and regardless of whether you classify yourself as an investor or a trader.

The base 30% rate

Take your sale value, subtract only the cost of acquisition, and apply 30%. No brokerage, no gas fees, no platform charges, no internet-bill apportionment is allowed as a deduction. The Income Tax Department’s reading of “cost of acquisition” is narrow and has been confirmed in successive CBDT clarifications.

Cess and surcharge on top

The 30% is the base; the effective rate is higher. A 4% Health and Education Cess applies on the tax amount, which pushes the effective rate to 31.2%. If your total taxable income (across all heads) crosses the surcharge thresholds, surcharge stacks on top of the 30% before cess.

| Total income band | Surcharge | Effective VDA tax rate |

|---|---|---|

| Up to Rs.50 lakh | Nil | 31.20% |

| Rs.50 lakh to Rs.1 crore | 10% | 34.32% |

| Rs.1 crore to Rs.2 crore | 15% | 35.88% |

| Rs.2 crore to Rs.5 crore | 25% | 39.00% |

| Above Rs.5 crore | 37% (old regime) or 25% (new regime cap) | up to 42.74% (old) / 39.00% (new) |

A worked example for a salaried investor

Consider Priya, a software engineer with Rs.18,00,000 (18 lakh) salary and a Rs.2,00,000 (2 lakh) gain from selling Ether. Her VDA tax is 30% of Rs.2,00,000 = Rs.60,000. The 4% cess on Rs.60,000 is Rs.2,400. Her total VDA tax bill is Rs.62,400. Crucially, that Rs.62,400 sits outside her slab-rate salary tax; the two do not merge.

Section 194S: The 1% TDS Mechanism and Refund Flow

Section 194S layers a withholding tax on top of the 30% income tax. Every time you transfer a VDA above the threshold, the buyer (typically the exchange) deducts 1% TDS on the gross consideration and deposits it with the government against your PAN.

Who deducts and when

On Indian exchanges, the platform itself deducts the 1% TDS at the point of sale or swap. For peer-to-peer trades or transactions on offshore platforms that do not deduct, the buyer is legally responsible. The threshold above which 1% TDS applies is Rs.50,000 per financial year for specified persons (most individuals and HUFs) and Rs.10,000 per year for others.

Why TDS sometimes feels punitive

The 1% is on gross consideration, not on profit. If you sold Rs.10,00,000 (10 lakh) worth of Bitcoin at a Rs.20,000 profit, the exchange still withholds Rs.10,000 as TDS. On a thin-margin swing trade, that withholding can exceed your actual profit, locking up working capital until you file your return.

Claiming TDS back through your return

Section 194S TDS is creditable. It appears in your Form 26AS and AIS, and you claim it as a credit when you file your ITR. If the TDS exceeds your final tax liability for the year, the excess flows back as a refund. The trick is that the refund only comes after you file, and the Income Tax Department processes the return, which can take three to nine months. Active traders should plan cash flow around that lag.

The No-Set-Off Rule: Why a Loss Is Just a Loss

This is the rule that catches first-time filers off guard, and it is the most expensive misunderstanding in the entire crypto tax India 2026 framework. Section 115BBH explicitly bars set-off and carry-forward of VDA losses.

What “no set-off” means in plain English

Losses from one VDA cannot offset gains from another VDA. Losses from VDAs cannot offset gains from equity, mutual funds, business income, or salary. Losses cannot be carried forward to next year. Each profitable transaction is taxed at 30%, and each loss simply disappears.

A worked example to make it concrete

Imagine Arjun made two trades in FY 2025-26. He bought Bitcoin for Rs.5,00,000 (5 lakh) and sold it for Rs.7,00,000, a Rs.2,00,000 gain. He bought Solana for Rs.4,00,000 and sold it for Rs.2,50,000, a Rs.1,50,000 loss. Common sense says he netted Rs.50,000. The Income Tax Act says he made Rs.2,00,000 of taxable gain and the Rs.1,50,000 loss is irrelevant. His tax is 30% of Rs.2,00,000 = Rs.60,000, plus 4% cess = Rs.62,400. His effective tax on his Rs.50,000 net economic gain is 124.8%.

How portfolio behaviour adapts

Sophisticated retail traders now treat each VDA position as a standalone tax silo, because that is how the law treats it. Tax-loss harvesting, which works well for listed equity under Section 70 to Section 74, does nothing for VDAs. The rational response is fewer, more deliberate trades, not more.

The April 1, 2026 Exchange-Reporting Rule

The Income Tax Act 2025 introduced Section 509, which obliges every “prescribed reporting entity” to file periodic crypto-asset transaction statements with the Income Tax Department. The companion penalty section, Section 446, makes the duty bite.

Who reports and what they report

Domestic exchanges, custodial wallets, and platforms registered under the Prevention of Money Laundering Act are the primary reporters. They must share user-level transaction data, including PAN, transaction value, asset, and counterparty information where available. The information flows into the Annual Information Statement and is cross-checked against each taxpayer’s Schedule VDA disclosure.

The penalty stack

A reporting entity that misses or delays filing faces Rs.200 per day of default. A reporting entity that files inaccurate information and does not correct it faces a penalty of up to Rs.50,000. These numbers are directed at platforms, but the second-order effect on individual users is significant: every exchange will tighten KYC, every transaction will be flagged, and reconciliation will be automatic.

What changes for the individual taxpayer

For the salaried investor, the practical impact is that under-reporting in Schedule VDA is no longer survivable. If your exchange says you sold Rs.4,00,000 of Ether and your return claims Rs.1,00,000, the AIS mismatch will trigger a Section 143(1) intimation at minimum, and a Section 270A under-reporting penalty (50% to 200% of the tax shortfall) at worst.

Schedule VDA: Disclosing Crypto in Your ITR

Schedule VDA is the row-by-row disclosure block inside ITR-2 and ITR-3 where every VDA transaction during the year must be reported. The schedule has been live since AY 2023-24 and is now the single biggest reconciliation tool the department uses.

What you fill in each row

For every transaction, you record the date of acquisition, the date of transfer, the cost of acquisition, the consideration received, and the income chargeable. Cost in INR for crypto-to-crypto swaps is the fair market value of the asset given up at the swap timestamp, which means historical exchange records are non-negotiable.

Which ITR form to use

Most retail investors will use ITR-2 (no business income) or ITR-3 (business income, including frequent trading classified as business). High-volume traders sometimes argue for business-income treatment to claim trading expenses, but Section 115BBH overrides Section 28 for VDA-specific gains, so the upside of that argument is narrower than it looks.

Reconciling against AIS and Form 26AS

Before filing, every crypto user should download the AIS, search for VDA entries, and tally them against their exchange transaction history. Any third-party entry that you cannot explain should be flagged through the AIS feedback module before you submit the return. Crypto carries leveraged volatility risk; do not invest more than you can afford to lose, and do not under-report on the assumption that small trades go unnoticed.

NFT and Token-Specific Wrinkles

The VDA definition is broad enough to capture NFTs and most tokens, but the application of the 30% rule has nuances that beginners miss.

NFTs

An NFT that meets the CBDT’s notified definition is a VDA. Gains from selling an NFT for INR or for another VDA are taxed at 30%. NFTs gifted to non-relatives can also trigger tax in the recipient’s hands under Section 56(2)(x) when fair market value exceeds Rs.50,000.

Airdrops, staking rewards, and mining

Receiving an airdrop or a staking reward is taxable at the fair market value on the date of receipt under Section 56(2)(x), at slab rates. The subsequent sale of that token is then taxed at 30% under Section 115BBH on the gain over and above that already-taxed fair market value. Forgetting the first step is a common error.

Stablecoins and INR-pegged tokens

Stablecoins are VDAs. Swapping USDT for INR is a transfer; swapping INR for USDT is an acquisition. The 1% TDS and the 30% income tax both apply, even though the “gain” on a stablecoin trade is usually tiny.

Common Crypto Tax Mistakes and How to Avoid Them

Across thousands of returns reviewed by chartered accountants in the past two filing seasons, a handful of mistakes recur with painful regularity.

Treating crypto-to-crypto swaps as non-events

A swap is a transfer. Every ETH-to-MATIC trade is two events: a deemed sale of ETH and an acquisition of MATIC. Both legs must be priced in INR using the fair market value at the swap time. Ignoring swaps is the single most common cause of AIS mismatches.

Netting losses against gains anyway

Filers, especially those used to equity rules, instinctively net VDA gains and losses. The return form accepts the figure, but the department’s automated cross-check on each row flags the inconsistency. The 50% to 200% Section 270A penalty for under-reporting is far worse than paying the full 30% in the first place.

Ignoring the 1% TDS reconciliation

Some users assume the 1% TDS settles the matter and do not file a return. It does not. The 30% is the headline tax; the 1% is a withholding on account. If you skip the return, you cannot claim the credit, you forfeit any refund, and you sit on the wrong side of a non-filer notice.

Using offshore exchanges to “avoid” Indian tax

Indian tax residence pulls global income into the Indian tax net. Using a Dubai or Cayman exchange does not change the 30%; it only adds a 1% TDS-collection problem (the foreign exchange does not deduct, so the buyer is meant to). The new April 2026 reporting framework also extends information-sharing requests through tax treaties, which makes offshore concealment a poor bet.

Step-by-Step: Filing Your Crypto Tax for FY 2025-26

A clean filing process saves more anxiety than any spreadsheet trick. Treat the following as a checklist, not a suggestion.

- Download every exchange transaction CSV for the full FY 2025-26 by the second week of April 2026.

- Convert every crypto-to-crypto swap into INR using the timestamped fair market value on a reputable price oracle, and store the workings.

- Reconcile the per-transaction TDS in your exchange statements against the entries in Form 26AS and AIS. Flag any mismatches via AIS feedback before filing.

- Aggregate gross consideration and cost of acquisition per asset; compute the 30% tax per profitable row, ignore loss rows for tax purposes.

- Add the 4% cess and any surcharge based on your total taxable income band.

- Open ITR-2 or ITR-3, populate Schedule VDA row by row, and ensure the TDS claim in Schedule TDS matches your AIS.

- Pay any balance via Challan 280 well before the July 31 deadline, and file the return.

- Retain all source documents (exchange CSVs, wallet exports, swap-timestamp screenshots) for at least eight years.

Advanced Edge Cases for Experienced Traders

For readers who have been in the market for several cycles, a few advanced patterns deserve their own treatment.

DeFi yield, lending, and liquidity pools

Yield earned in a lending protocol or a liquidity pool is taxable at the time of accrual at slab rates under Section 56(2)(x), and the underlying token movements are taxable transfers under 115BBH when realised. The CBDT has not yet issued a comprehensive DeFi circular, so cautious practice is to treat each protocol interaction as a discrete reportable event.

Hard forks and chain splits

Tokens received from a fork are treated as acquired at zero cost unless a specific valuation is supportable. The full sale value of the forked tokens, when eventually sold, is taxable at 30%.

Gifting and inheritance

Gifts of VDA to relatives (as defined in the IT Act) are exempt in the recipient’s hands. Gifts to non-relatives are taxable if the aggregate fair market value crosses Rs.50,000 in a year. Inherited crypto inherits the deceased’s cost basis; the transferee’s later sale is taxed at 30% on the gain over that cost.

Crypto Tax India 2026 Budget Updates and What to Watch

Budget 2026 made it clear that the policy direction is tighter compliance, not lower rates. The 30% and 1% TDS are politically settled for now; the energy has shifted to plugging information gaps.

What did not change

The 30% flat tax, the 4% cess, the 1% TDS, the no-set-off rule, and the no-expense-deduction rule were all left intact. Industry asks for parity with equity (a long-term lower rate, loss set-off, and indexation) were declined again.

What did change

Section 509 reporting, Section 446 penalties, expanded Schedule VDA disclosures, and tighter AIS reconciliation were the headline additions. Crypto exchanges now operate under a quasi-broker compliance burden similar to depositories under SEBI rules.

What to watch in Budget 2027

The market is watching for clarification on DeFi treatment, a possible carve-out for stablecoin payments below a de-minimis threshold, and any movement on loss set-off. None of these is promised; none should be assumed.

Frequently Asked Questions

Is the 30% crypto tax in India still 30% in FY 2025-26?

Yes. Section 115BBH continues to apply a flat 30% tax on gains from the transfer of any virtual digital asset, including Bitcoin, Ether, stablecoins, and most NFTs. A 4% Health and Education Cess takes the effective minimum rate to 31.2%, with surcharge stacking on top if total income crosses Rs.50 lakh.

Can I set off crypto losses against any other income?

No. Section 115BBH explicitly bars set-off of VDA losses against any income, including other VDA gains, and bars carry-forward. Each profitable VDA transaction is taxed on its own; each loss is permanently lost for tax purposes.

How does the 1% TDS under Section 194S get refunded?

Indian exchanges deduct 1% TDS on the gross consideration and deposit it against your PAN. The amount appears in Form 26AS and AIS. You claim it as a credit when you file your ITR; if total TDS exceeds final tax due, the excess is refunded after the return is processed, which usually takes three to nine months.

What happens if my exchange reports a transaction that I do not declare?

From April 1, 2026, exchanges must file user-level transaction statements with the Income Tax Department under Section 509. Any mismatch with your Schedule VDA disclosure triggers an automated flag, an intimation under Section 143(1), and potentially a Section 270A under-reporting penalty of 50% to 200% of the tax shortfall.

Are NFTs and stablecoin trades also taxed at 30%?

Yes. The VDA definition covers both. NFTs that meet the CBDT-notified definition are taxed at 30% on transfer, and gifts to non-relatives can additionally trigger Section 56(2)(x) tax in the recipient’s hands. Stablecoin swaps are also taxable transfers at 30%, even when the gain is small.

Related LearnFineEdge guides on India’s crypto tax filing, exchange-reporting compliance, and NFT taxation are forthcoming and will be linked here as the cluster goes live.