From April 1, 2026, the reporting equation for Indian crypto investors changes fundamentally. The Income Tax Department now receives transactional data directly from registered Indian exchanges and reporting entities, layered on top of the existing 1% TDS under Section 194S and the flat 30% rate on virtual digital asset income under Section 115BBH. The crypto tax reporting rules 2026 india regime no longer relies on voluntary disclosure to surface gains; the data lands in AIS, Form 26AS and Schedule VDA whether the filer reports the transactions or not. That single shift moves crypto from a low-detection asset class to a high-detection one for FY 2025-26 returns and onwards.

This guide explains what data exchanges now share, the penalty schedule that applies when reporting is missed or incomplete, and a clean filing checklist for individual VDA holders. The references are to Section 285BAA, Section 115BBH, Section 194S and Section 271FAA as in force; readers should confirm the latest CBDT notifications for any updates after publication.

Why the crypto tax reporting rules 2026 india shift matters

The earlier framework already taxed VDA gains, but enforcement leaned on the taxpayer to self-disclose accurately.

From self-disclosure to data-feed enforcement

Section 285BAA, introduced through Budget 2024 and now operational from April 1, 2026, requires reporting entities to share specified VDA transaction information with the IT Department. The Department aggregates this against the taxpayer’s PAN and surfaces it in AIS.

What changes for the average investor

The Department previously had partial visibility through Section 194S TDS at 1%. With the new feed, the Department sees buy and sell legs, asset identifiers, dates, counterparty type and aggregate values. Schedule VDA mismatches now trigger automated notices instead of manual scrutiny.

What does not change

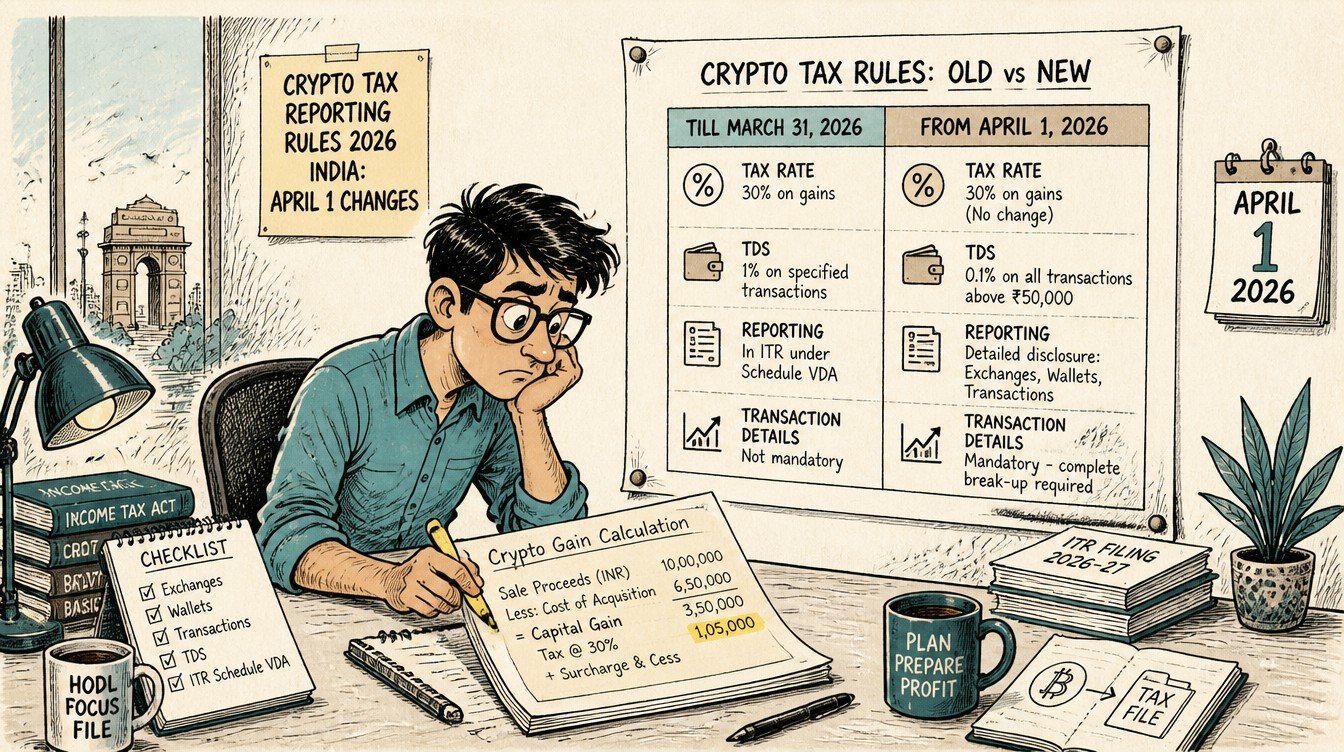

The tax rate of 30% on VDA income under Section 115BBH continues. So does the 1% TDS under Section 194S and the prohibition on offsetting VDA losses against other income. The new framework changes detection, not the underlying rate or set-off rules.

What data goes to the IT Department

Section 285BAA and the associated rules define what reporting entities must send.

Counterparty data

The reporting includes the PAN, Aadhaar or other identifier of each user, KYC details, and the user’s exchange-side account identifier. The Department can map every transaction to a taxpayer at PAN level.

Transaction data

- Asset identifier (BTC, ETH, INR-quoted tokens, stablecoins and so on)

- Buy date, sell date and quantity per leg

- Rupee consideration on each leg

- Brokerage, network fees and any other charges

- 1% TDS under Section 194S deducted, if applicable

- P2P transfers and wallet-to-wallet movements on the platform

Aggregate metrics

The data feed also includes annual aggregates: total buy value, total sell value, realised gains, realised losses, and outstanding balance at year-end. These aggregates populate AIS directly.

Who counts as a reporting entity

Not every player in the ecosystem reports, but the major ones do.

Registered Indian exchanges and brokers

Indian-registered crypto exchanges, brokers, and trading platforms that facilitate VDA transactions are squarely within the reporting net. Examples include the major INR on-ramp exchanges that the average retail investor uses.

Custodians and wallet providers

Custodial wallet providers, including hosted wallets offered as part of an exchange account, are also reporting entities for balances and transfers visible to them.

What sits outside

Self-custodied wallets that do not transit through an Indian reporting entity are technically outside the direct reporting feed. However, every time funds move between a self-custodied wallet and an Indian exchange or fiat on-ramp, the leg that touches the exchange is reported. Pure on-chain activity is also visible to the Department through public blockchain explorers; the new framework simply makes that data part of the formal compliance record.

Penalty schedule for missed or incomplete reporting

The penalties apply both at the reporting entity level and the taxpayer level.

Section 271FAA: penalty on reporting entities

Reporting entities that fail to furnish the prescribed statement attract a penalty of Rs.50,000 for failure to file, and a continuing fee of up to Rs.500 per day for each day of delay beyond the due date. Inaccurate statements attract a separate penalty.

Daily fee for delayed submission

A late-filing fee schedule applies after the original due date. The most commonly cited number is Rs.200 per day as a continuing fee for delay in furnishing the SFT-style statements, with a hard cap that can reach Rs.50,000 aggregated. Exact rates should be confirmed against the latest CBDT rule notification.

Penalties on individual taxpayers

For the individual taxpayer, the consequences flow through the existing under-reporting framework. Section 270A penalty at 50% or 200% applies on tax payable on under-reported income, and Section 234A interest at 1% per month applies on unpaid tax. The under-reporting penalty can quickly exceed the original tax outflow.

How AIS now reflects VDA activity

The Annual Information Statement is where the impact lands for most retail filers.

New VDA line items in AIS

Schedule VDA-linked information now shows up in AIS with the same granularity as broker-reported equity. Filers can see asset-wise totals for buys and sells, plus the TDS deducted and the realised gain or loss in INR.

Reconciliation workflow

The recommended workflow is: download AIS, download the exchange’s annual tax statement, and reconcile transaction by transaction. Mismatches should be flagged inside the AIS feedback channel before filing.

What automated mismatches look like

If Schedule VDA reports a lower aggregate than AIS shows, the return is flagged for a Section 143(1)(a) prima facie adjustment. The notice typically asks the filer to either revise the return or respond with supporting documentation. Ignored notices can escalate to scrutiny.

Schedule VDA in the ITR form

Schedule VDA has evolved over the last two filing cycles to capture more detail.

Transaction-level disclosure

For FY 2025-26, Schedule VDA expects transaction-level details: date of purchase, date of sale, cost of acquisition, sale consideration, and net gain. Filers cannot lump multiple transactions together unless the form explicitly allows it for a given asset type.

Cost of acquisition rules

Only the cost of acquisition is deductible from the sale consideration. Brokerage and network fees on the sale leg are part of the cost of transfer and reduce consideration; purchase-side brokerage is part of cost. No other expense, including software or hardware costs, is deductible.

Loss treatment in Schedule VDA

Losses on individual VDA transactions cannot be set off against gains from other VDA transactions in the same year under the prevailing position. Each gain is taxed standalone at 30%, and losses lapse unless and until a future amendment changes the position.

Worked example: typical retail VDA filer

A simple example shows how the math flows through the return.

Setup

FY 2025-26 transactions on a registered Indian exchange: bought 0.05 BTC at Rs.30,00,000 each, total cost Rs.1,50,000; sold three months later at Rs.36,00,000 each, total consideration Rs.1,80,000. Brokerage on each leg Rs.250.

Gain computation

Net consideration on sale = Rs.1,80,000 minus Rs.250 = Rs.1,79,750. Cost of acquisition = Rs.1,50,000 plus Rs.250 = Rs.1,50,250. Gain = Rs.29,500. Tax under Section 115BBH at 30% = Rs.8,850. Section 194S 1% TDS already deducted on the sale of Rs.1,800 reduces the cash outflow.

Reporting in Schedule VDA

The transaction appears as a single row with the buy date, sell date, cost Rs.1,50,250, consideration Rs.1,79,750, and gain Rs.29,500. The TDS credit appears in the tax-paid schedule and offsets the gross tax payable.

Filing checklist for VDA holders

The checklist below is built around a tax-resident individual with VDA activity on Indian exchanges.

Step 1: Pull every exchange’s annual statement

Each exchange used during the year should issue an annual tax statement summarising all transactions and TDS. Download all of them at once, even from exchanges where activity was minor.

Step 2: Reconcile against AIS

Compare each exchange’s totals against the corresponding AIS lines. Note any difference and submit AIS feedback before filing if numbers are wrong.

Step 3: Compute gain per transaction

For each disposal, compute gain as consideration minus cost. Loss legs are recorded but not netted against other VDA gains. The 30% rate applies to each gain leg individually.

Step 4: Match TDS credit

The 1% TDS under Section 194S appears in Form 26AS and AIS. Ensure the total TDS credit claimed in the return matches what reporting entities have deducted.

Step 5: Disclose holdings under Schedule VDA and Schedule FA where relevant

Holdings at year-end on Indian exchanges go into Schedule VDA. Holdings on foreign exchanges or self-custodied wallets denominated in foreign currency may also trigger Schedule FA reporting for residents. The two schedules are independent and may both apply.

Common mistakes that trigger notices

The new data-feed regime has produced a recognisable set of error patterns.

Netting losses against gains

Treating loss legs as a reduction in taxable gain is the single most common mistake. Section 115BBH does not allow it, and CPC will add back the netted amount with interest.

Reporting only INR-denominated trades

Crypto-to-crypto trades are also taxable in INR equivalent terms. Filers who report only the legs that touched INR understate gains by a meaningful margin in active accounts.

Ignoring small-value transactions

The 1% TDS threshold under Section 194S is intentionally low. Aggregate small transactions still reach the threshold quickly, and AIS picks them up regardless. There is no de minimis exemption inside Section 115BBH.

Missing exchanges

If the year saw activity on multiple exchanges, every one of them feeds into AIS. Filing a return based on only one exchange’s statement is a guaranteed mismatch.

Where ITR-U comes in

The new data feed makes ITR-U particularly relevant for VDA holders.

Voluntary updates for missed VDA income

Filers who under-reported VDA income in earlier years can file ITR-U under the extended 48-month window to bring the return into compliance, paying the regular tax plus the 25% to 70% additional tax depending on how many years have passed.

Why pre-empting the notice is cheaper

Once a Section 148A notice is issued, the under-reporting penalty under Section 270A at up to 200% kicks in. ITR-U with its 25% premium remains the materially cheaper route, particularly for the first 12 months after the relevant assessment year ends.

Documentation to retain

Maintain exchange statements, KYC records, on-chain transaction hashes for self-custodied movements, and bank statements showing fiat legs. A retention horizon of at least eight years aligns with the time-bar windows for reassessment under the Income Tax Act.

Advanced situations

Three nuances deserve a closer look.

Airdrops, staking and mining income

Airdrops and mining rewards are treated as income under Section 56 at fair market value on receipt, and again as VDA disposal when the underlying token is sold. Staking rewards follow a similar two-event pattern. Cost basis for the subsequent disposal is the value already taxed on receipt.

Foreign exchange wallets

Holdings on foreign exchanges trigger Schedule FA reporting for resident taxpayers if the aggregate value crosses the prescribed thresholds. The Schedule VDA reporting on Indian gains and the Schedule FA reporting on foreign holdings are independent and both may apply.

Gift of VDAs

Gifting VDAs above the Section 56 threshold to a non-relative is taxable in the hands of the recipient at fair market value. The donor may face Section 50AA treatment in certain configurations. The rules are still maturing; cautious documentation is the safer default.

Frequently asked questions

What changes for VDA investors from April 1, 2026?

Registered Indian exchanges now share transactional VDA data with the Income Tax Department under Section 285BAA. The data lands in AIS and is reconciled against Schedule VDA in the ITR, making under-reporting much easier to detect.

Can I set off crypto losses against my equity gains?

No. Section 115BBH does not allow VDA losses to be set off against any other income. The losses also cannot be carried forward, and inter-VDA netting is not permitted under the prevailing position.

What penalty applies if I miss reporting a crypto sale?

The individual taxpayer faces tax at 30% plus Section 234A interest at 1% per month and Section 270A penalty at 50% or 200% of the tax on the under-reported income, depending on whether under-reporting is treated as mis-reporting.

Does the 1% TDS under Section 194S cover my full tax liability?

No. The 1% TDS is a withholding mechanism, not the final tax. The 30% tax under Section 115BBH applies on the gain, and the 1% TDS is credited against the final liability.

What records should I keep as a VDA holder?

Exchange annual tax statements, KYC records, bank statements showing fiat legs, on-chain transaction hashes for self-custodied movements, and any communications related to airdrops or staking rewards. A retention horizon of at least eight years is prudent.

Related guides on Section 115BBH mechanics, Schedule VDA filing, and ITR-U for under-reported crypto income are forthcoming on this site.