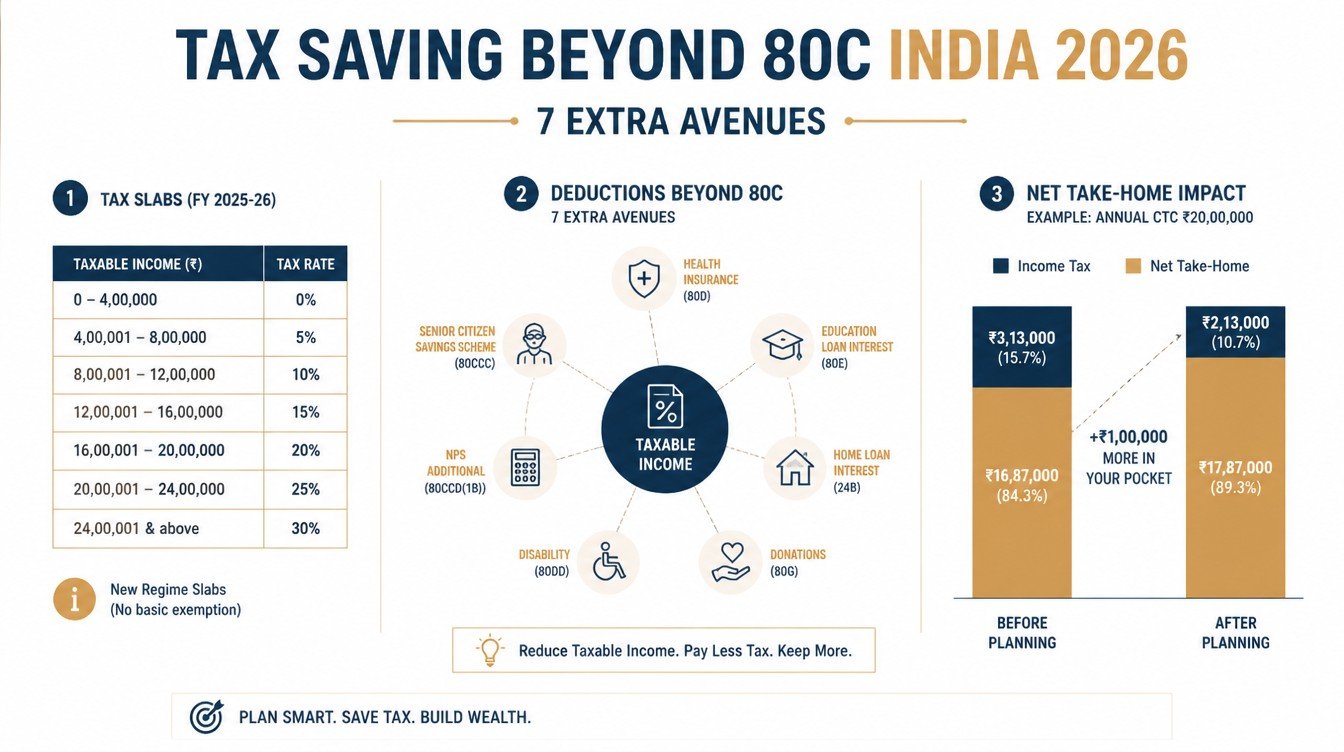

Section 80C is the most familiar tax deduction in India and also the smallest, at Rs.1,50,000 per year. Maxing it out is straightforward for most salaried Indians, because EPF contributions, life insurance premiums and any home loan principal repayment together usually fill the cap before the year is half over. The harder, more interesting question is what comes next. The tax saving beyond 80c india 2026 question matters most under the old regime, where seven other sections quietly add up to another Rs.2,00,000 to Rs.3,00,000 of legitimate deduction headroom for FY 2025-26.

This guide walks through seven specific avenues, the proofs the Income Tax Department expects, and how to stack them so the combined deduction does not collide with any per-section cap. The list is built around what actually reduces taxable income for a salaried Indian, not theoretical exotic structures. All sections referenced are from the Income Tax Act as in force for FY 2025-26; readers should confirm any rate or threshold changes via incometax.gov.in or the latest CBDT notification.

Why tax saving beyond 80c india 2026 still matters

Even with the new regime as default, a meaningful share of salaried Indians continue to opt for the old regime because their deduction stacks justify it. The seven avenues below mostly live inside the old regime.

The old regime is where additional deductions live

Sections 80D, 80E, 80G, 80CCD(1B), 80TTA, 80TTB, 80DDB, and HRA are largely available only when the filer opts for the old regime under Section 115BAC(6). The new regime allows only Section 80CCD(2) on employer NPS and a few narrowly scoped items.

How the stacking arithmetic helps

Layer the seven avenues over Section 80C, and a salaried filer in a metro can comfortably claim Rs.3,00,000 to Rs.5,00,000 of legitimate deductions over standard deduction. That is the headroom that flips the regime choice toward the old regime for many filers in the Rs.15 lakh to Rs.30 lakh band.

Limits and overlap

Each section has its own cap, and the law disallows double-counting the same outgo under two sections. A given premium, contribution or rent receipt belongs to exactly one section. The stacking works only when each cap is filled with a distinct outgo.

Avenue 1: Section 80D health insurance premiums

Section 80D is the most consistently underused deduction outside Section 80C.

Self, spouse and children cover

Premium paid for a health insurance policy covering self, spouse, and dependent children is deductible up to Rs.25,000 per year. If any insured family member is a senior citizen, the cap rises to Rs.50,000.

Parents cover

A separate Rs.25,000 (or Rs.50,000 for senior parents) cap is available for health insurance premium paid on the parents’ policy. The total Section 80D claim can therefore reach Rs.1,00,000 per year for a filer with senior parents.

Preventive health check-up

Within the overall cap, up to Rs.5,000 of preventive health check-up expenses for self, family or parents qualifies. Cash payments are accepted only for this sub-limit; the main premium itself must be paid through banking channels.

Avenue 2: Section 80CCD(1B) additional NPS deduction

Section 80CCD(1B) is the most powerful old-regime add-on for filers who can lock capital for the long run.

Rs.50,000 over and above 80C

An additional Rs.50,000 deduction is available for contributions to the National Pension System Tier-1 account, on top of Section 80C. The same contribution cannot be claimed under both 80C and 80CCD(1B); the cleaner route is to fill 80C with EPF or PPF, and use NPS Tier-1 separately under 80CCD(1B).

Long lock-in trade-off

NPS Tier-1 is locked until 60, with limited partial withdrawals before that. The deduction is real, but the liquidity sacrifice is also real. Filers who already have illiquid retirement allocations elsewhere should size NPS contributions accordingly.

Asset allocation choice

NPS allows the subscriber to pick the equity, corporate debt, and government debt mix. Market-linked instruments inside NPS carry market risk; the deduction is on the contribution, not on any future return.

Avenue 3: Section 80E education loan interest

Section 80E is among the cleanest old-regime deductions because it has no upper cap.

Who can claim

The deduction is available to an individual paying interest on an education loan taken for higher studies for self, spouse, children or a legal ward. The lender must be a financial institution or notified charitable institution.

No cap, eight-year window

Section 80E has no ceiling on the deduction amount. It can be claimed for up to eight years from the year repayment begins or until the interest is fully paid, whichever is earlier. For filers with large education loans, this is one of the highest absolute deductions available.

Only the interest, not principal

Only the interest portion of the EMI is deductible. The principal component of an education loan does not qualify under Section 80E or Section 80C. The bank certificate splits interest and principal each year for this purpose.

Avenue 4: Section 80G donations

Section 80G allows deductions for donations to specified institutions.

50% or 100% deduction tiers

Donations to certain government funds (PM National Relief Fund, National Defence Fund, and similar) qualify for a 100% deduction without the qualifying-amount limit. Donations to most other approved trusts are 50% deductible, often subject to a 10% of adjusted gross total income cap.

Documentation

The donee must furnish a stamped receipt with PAN, 80G registration number, and the donor’s name. Donations above Rs.2,000 in cash are not eligible; banking-channel payments are mandatory above that threshold.

Stacking with CSR-type contributions

Section 80G cannot be used for contributions where corporate CSR rules apply to a company. Salaried filers donating in personal capacity are not affected, but the receipt must be in the individual’s name to qualify.

Avenue 5: Section 80TTA and 80TTB on interest income

These two sections give a small but easy-to-claim deduction on bank interest.

Section 80TTA for non-seniors

Section 80TTA allows a deduction of up to Rs.10,000 on interest from savings accounts in banks, post offices and cooperative banks, for filers below 60. Interest on fixed deposits is not eligible under this section.

Section 80TTB for senior citizens

Senior citizens get the much wider Section 80TTB, with a cap of Rs.50,000 on interest from savings deposits, FDs and recurring deposits combined. A senior filer with bank deposits of Rs.7,00,000-Rs.10,00,000 (7-10 lakh) often fills this cap fully.

How to surface this in returns

Bank interest is reported under Income from Other Sources. The 80TTA or 80TTB deduction is claimed in Chapter VI-A after the gross total income is computed. Many filers forget the deduction, leaving the interest income fully taxable.

Avenue 6: Section 80DDB specified illnesses

Section 80DDB compensates for actual medical expenditure on specified critical illnesses.

Eligible expenses

Expenditure on treatment of specified diseases such as malignant cancers, chronic renal failure, certain neurological conditions, and AIDS qualifies under Section 80DDB. The list is defined by Rule 11DD.

Deduction cap

The deduction is Rs.40,000 for filers below 60 and Rs.1,00,000 for senior citizens. Any amount reimbursed by an insurer or employer is reduced from the eligible amount.

Prescription requirement

A prescription from a specialist with relevant qualifications is mandatory. The deduction cannot be claimed without it, and CPC has been increasingly automated in disallowing 80DDB claims without supporting documentation.

Avenue 7: HRA exemption under Section 10(13A)

HRA is technically an exemption, not a Chapter VI-A deduction, but it sits in the same old-regime advantage bucket.

The three-element formula

The HRA exemption is the least of: actual HRA received, rent paid minus 10% of basic salary, or 50% of basic salary in metro cities (40% in non-metros). The lowest of these three caps the claim.

Landlord PAN above Rs.1,00,000 annual rent

If the annual rent exceeds Rs.1,00,000, the landlord’s PAN must be provided to the employer or declared in the return. Without PAN, the HRA exemption is typically disallowed.

Rent paid to a family member

Rent paid to a parent or other family member is legally allowable but heavily scrutinised. A formal lease, banking-channel rent payment, and the family member declaring the rent as income on their own return are the conditions that hold up at assessment.

The seven that stack well together

The combination below works for a salaried metro filer with senior-citizen parents, an education loan, and HRA access.

| Avenue | Cap or scope | Typical realised deduction |

|---|---|---|

| Section 80D (self + parents) | Rs.25,000-Rs.50,000 + Rs.25,000-Rs.50,000 | Rs.50,000-Rs.1,00,000 |

| Section 80CCD(1B) NPS Tier-1 | Rs.50,000 | Rs.50,000 |

| Section 80E education loan interest | No cap, 8-year window | Rs.50,000-Rs.1,50,000 |

| Section 80G donations (50% or 100%) | Variable, subject to 10% GTI cap | Rs.10,000-Rs.50,000 |

| Section 80TTA / 80TTB | Rs.10,000 / Rs.50,000 | Rs.5,000-Rs.50,000 |

| Section 80DDB specified illnesses | Rs.40,000 / Rs.1,00,000 | Rs.0-Rs.1,00,000 |

| HRA under Section 10(13A) | Least of three formula caps | Rs.1,00,000-Rs.4,00,000 |

A salaried metro filer with the combinations above can legitimately claim Rs.2,50,000-Rs.6,00,000 of deductions over and above Section 80C in a single financial year, depending on circumstances.

Common mistakes when stacking deductions

The stack collapses fast when documentation gaps appear.

Double counting the same outgo

EPF contributions cannot count under both 80C and 80CCD(1B). NPS Tier-1 cannot be claimed twice. Filers who try to layer the same amount across two sections receive defective-return notices.

Cash donations above Rs.2,000

Cash donations to 80G entities above Rs.2,000 are disallowed entirely. Use banking channels for any donation that needs to qualify under 80G.

Missing landlord PAN for HRA

The single most common HRA disallowance reason is a missing landlord PAN when rent exceeds Rs.1,00,000 per year. Collect it before March 31 and keep the receipt on file.

Forgetting 80DDB documentation

The 80DDB claim is contingent on a specialist’s prescription with prescribed details. A general medical bill is not sufficient.

Where the new regime can still help

Even in the new regime, two specific deductions survive and can move the math.

Employer NPS under Section 80CCD(2)

Employer NPS contributions up to 10% of basic salary (14% for central government employees) remain deductible under both regimes. Filers in companies that allow basic-versus-flexible salary restructuring often raise employer NPS to capture more of this deduction.

Standard deduction in new regime

The Rs.75,000 standard deduction in the new regime is higher than the Rs.50,000 in the old regime. For very light deduction stacks, this single difference can sway the regime choice.

Family pension deduction

Family pension recipients get a deduction of one-third of the pension or Rs.25,000, whichever is lower, in the new regime as well. This is a niche but useful carve-out for many senior families.

Advanced moves and edge cases

Beyond the seven main avenues, a small number of niche sections are worth knowing.

Section 80EEB on electric vehicle loan interest

Section 80EEB allows up to Rs.1,50,000 of interest deduction on a loan taken to buy an electric vehicle, sanctioned in eligible years. This is one-off but sizeable when applicable.

Section 80GG for rent paid without HRA

Salaried filers who do not receive HRA but pay rent can claim a limited deduction under Section 80GG. The cap is the least of Rs.5,000 per month, 25% of total income, or rent paid minus 10% of total income.

Section 24(b) home loan interest

While not strictly Chapter VI-A, the Section 24(b) home loan interest deduction of up to Rs.2,00,000 for self-occupied property is one of the largest old-regime exemptions and is usually evaluated alongside the seven avenues above.

Frequently asked questions

Do these deductions work in the new tax regime?

Most of them do not. Sections 80D, 80E, 80G, 80CCD(1B), 80TTA, 80TTB, 80DDB and HRA are largely available only in the old regime. The new regime keeps employer NPS under 80CCD(2) and a few narrow items.

Can the same insurance premium count under 80C and 80D?

No. A given premium belongs to one section only. Life insurance premium for a non-pension policy counts under 80C; health insurance premium counts under 80D. They cannot be double-claimed.

Is there a cap on total Chapter VI-A deductions?

Each section has its own cap. There is no aggregate ceiling separate from per-section limits. Total deductions cannot exceed gross total income, which is the implicit overall constraint.

What proofs should I keep ready before filing?

Bank challans, premium receipts, NPS contribution statements, education loan interest certificates, rent receipts with landlord PAN, donation receipts with 80G registration number, and specialist prescriptions for 80DDB. CPC may ask for any of these later.

Can a single filer realistically claim all seven?

Most filers will claim three to five of these in any given year. Claiming all seven requires an unusual mix of circumstances, but the framework is designed so any combination is legal as long as documentation supports each claim.

Related guides on the new-vs-old regime decision, HRA exemption math, and NPS Tier-1 contribution mechanics are forthcoming on this site.