Gold Loan India 2026 rates have moved into a more competitive zone since RBI tightened LTV norms in late 2024 and then revised the cap for small-ticket loans in early 2026. For a salaried earner sitting on family gold and facing a short-term cash crunch, this is one of the cheapest loan products available, often at half the interest rate of a personal loan and with a turnaround time measured in hours. This guide compares current rates from the big four lenders (SBI, HDFC, Muthoot Finance, Manappuram Finance), works through the per-gram disbursement math at today’s prices, and finishes with a side-by-side example of a Rs 50,000 gold loan versus a Rs 50,000 personal loan repaid over 12 months.

The headline reason gold loans are worth a hard look in 2026: gold prices are at all-time highs in rupee terms, so the same family bangle or chain that you pledged in 2022 will get you a meaningfully higher disbursement now. The downside has not changed: miss your EMIs, and the lender auctions your jewellery, with very little of the consumer protection that home loans or vehicle loans carry.

What the RBI LTV rules say in 2026

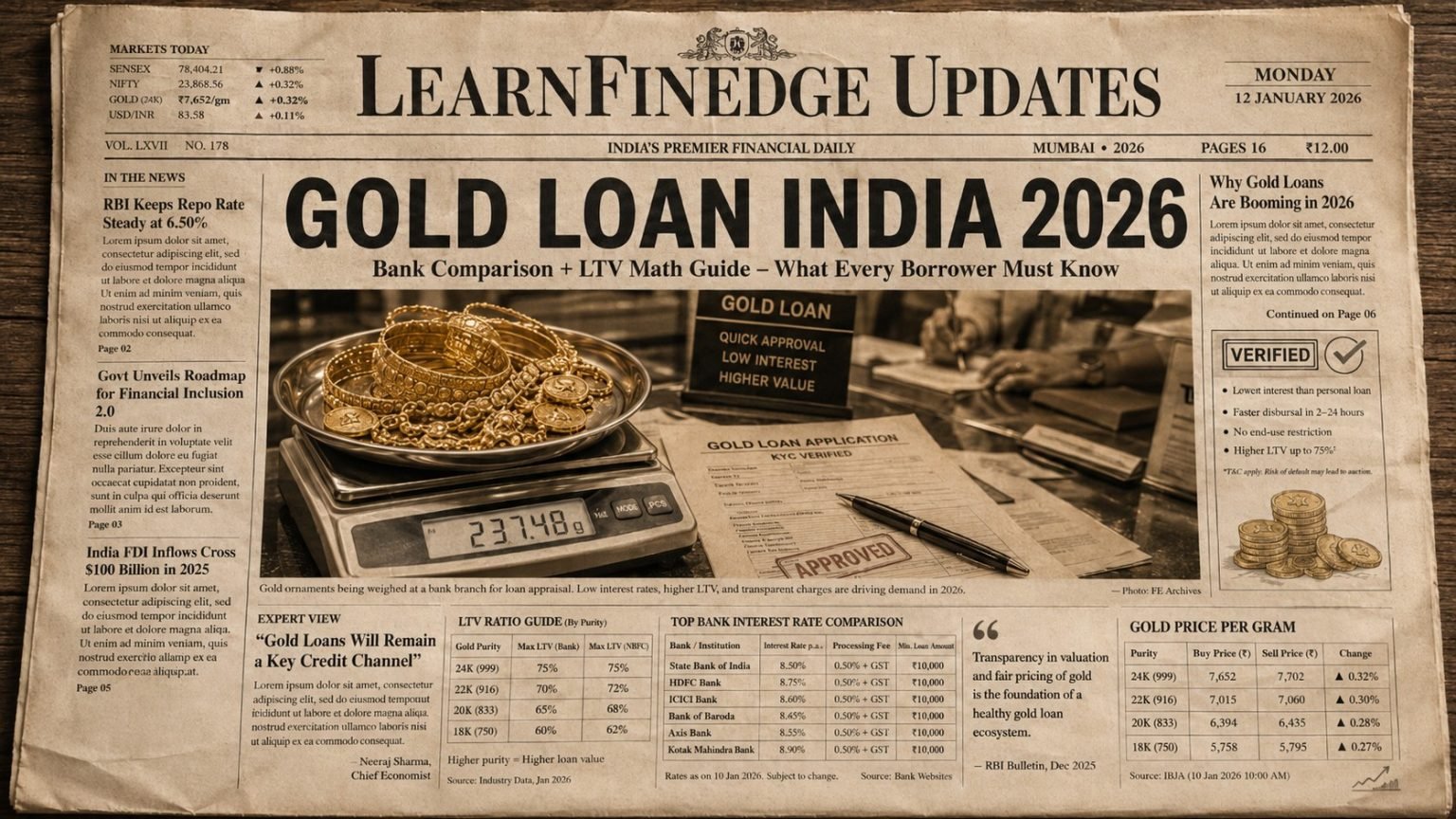

The basic regulatory framework is set by the RBI’s Master Direction on lending against gold. The default loan-to-value cap is 75 per cent of the appraised value of the gold ornaments at the time of disbursement. So if your jewellery is appraised at Rs 1 lakh, you can borrow up to Rs 75,000 against it.

In April 2025 the RBI relaxed the LTV cap for very small loans. For gold loans of up to Rs 2.5 lakh from regulated lenders (banks, NBFCs, and cooperative banks), the LTV can go up to 85 per cent. For loans between Rs 2.5 lakh and Rs 5 lakh, the cap remains 80 per cent. Above Rs 5 lakh, the standard 75 per cent cap applies.

Gold loans for non-agricultural purposes from banks have a maximum loan size cap of Rs 25 lakh per borrower. NBFCs do not face this individual cap but follow the LTV ladder.

The appraised value is based on the prevailing market price of 22-carat gold on the appraisal date (most jewellery in India is 22 carat). Lenders apply the price to the net weight of gold (gross weight minus stones, hooks, and soldering). They do not pay you anything for the making charges or stones.

Current gold loan rates from major lenders

As of mid-2026, here is where the four big lenders are pricing gold loans. Rates change with the repo cycle, so always confirm at the branch.

State Bank of India: starting rate 8.7 percent per annum for the standard gold loan, going up to 9.5 percent for higher ticket sizes and longer tenures. Processing fee 0.5 percent plus GST. SBI offers both EMI-based and overdraft-style gold loans.

HDFC Bank: starting rate 9.2 per cent, capped at around 17 per cent for high-risk borrowers. Processing fee is 1 per cent plus GST. HDFC has a slightly more conservative appraisal, so the same jewellery often fetches Rs 100-200 less per gram compared to NBFCs.

Muthoot Finance: rates start at 9.99 per cent and go up to 24 per cent depending on the loan scheme. Their flagship Gold Loan @ Lowest Rate offers the 9.99 per cent floor on smaller tickets with full LTV. Processing fee: Rs 250 to Rs 500 flat for most products. Disbursement is famously fast, often within 30 minutes.

Manappuram Finance: rates between 10 per cent and 24 per cent, similar structure to Muthoot. Their Online Gold Loan product allows you to keep the gold at home with a virtual pledge in some markets, but the standard product is a physical-pledge branch loan. Processing fee: Rs 250-500.

Cooperative banks and smaller PSU banks often undercut these rates by 50 to 100 basis points, but their per-gram disbursement tends to be lower because their appraisers are more conservative.

Per-gram disbursement math at today’s prices

Take 22-carat gold at roughly Rs 7,200 per gram (mid-2026 market rate; this number moves daily, so confirm on the day of pledge).

For a loan in the up-to-Rs-2.5-lakh ticket size where 85 per cent LTV applies: per gram disbursement = Rs 7,200 multiplied by 0.85 = Rs 6,120.

For a loan in the Rs 2.5 lakh to Rs 5 lakh band at 80 per cent LTV: per gram disbursement = Rs 7,200 multiplied by 0.80 = Rs 5,760.

For loans above Rs 5 lakh at 75 per cent LTV: per gram = Rs 5,400.

So a 50-gram chain (net weight after deducting stones and hooks) gets you Rs 3.06 lakh at 85 per cent LTV in the small-ticket bracket, Rs 2.88 lakh at 80 per cent, and Rs 2.7 lakh at the standard 75 per cent. The per-gram number you see advertised by Muthoot and Manappuram (often around Rs 6,000-6,100 in 2026) is just the LTV rule applied to the day’s gold price, nothing magical.

The number drops sharply for lower-purity gold. For 20-carat ornaments, the per-gram price drops by about 10 per cent. For 18-carat, by about 20 per cent. Most family jewellery is 22-carat, so the higher number applies in practice.

Tenure and repayment options

Gold loans typically come in three repayment flavours.

Bullet repayment: you pay only interest monthly (or even at the end), and the principal is repaid as a single bullet at the end of the tenure. Standard tenure is 6 to 12 months. This is the most common gold loan structure at NBFCs because it lets you take the loan, deploy it, and clear it from a single windfall (festival bonus, business receivable, or salary arrears) without a fixed EMI burden.

EMI repayment: equated monthly instalments covering principal plus interest, structured like a personal loan. Standard tenure is 12 to 36 months. Banks like SBI and HDFC favour this. The monthly outgo is higher, but the loan amortises predictably.

Overdraft style: the lender sanctions a limit against your gold; you withdraw and repay any amount within the limit, and interest accrues only on the utilised portion. SBI and a few other banks offer this. Useful for working-capital-style needs where you do not need the full amount upfront.

Foreclosure (pre-paying the entire loan) is generally allowed without penalty across most lenders in 2026. RBI’s guidelines on retail loan prepayment penalties extend partial protection to gold loans, though some NBFCs still charge a nominal Rs 500-1,000 fee for foreclosure within the first month.

Worked example: Rs 50,000 gold loan vs Rs 50,000 personal loan, 12 months

This is the comparison most salaried earners need to see when deciding between a gold loan and a personal loan for a short-term need.

Assumptions: borrow Rs 50,000 for 12 months and repay in an EMI structure for the personal loan and a bullet structure for the gold loan (the more common form for this size).

Gold loan at 10 per cent per annum on bullet repayment: monthly interest-only payment = Rs 50,000 multiplied by 10 per cent divided by 12 = Rs 417 per month. Twelve months of interest = Rs 5,000. Principal Rs 50,000 paid as a bullet at the end. Total outgo = Rs 55,000. Plus a Rs 500 processing fee. Net cost of loan = Rs 5,500.

Personal loan at 14 per cent per annum on EMI (this is a typical rate for a salaried borrower with a 750+ CIBIL): An EMI on Rs 50,000 for 12 months at 14 per cent is Rs 4,491. Total outgo over 12 months = Rs 53,892. A plus 2 per cent processing fee on Rs 50,000 = Rs 1,000. Net cost of loan = Rs 4,892.

On paper the personal loan looks cheaper because the EMI structure amortises the principal each month, so the average outstanding balance is roughly Rs 25,000, not Rs 50,000. But the comparison flips if the personal loan rate is higher or if your CIBIL is below 750.

Personal loan at 18 per cent (more typical for fresh hires or low-CIBIL borrowers): EMI = Rs 4,584. Total over 12 months = Rs 55,008. Plus a processing fee of Rs 1,000. Net cost = Rs 6,008. Now the gold loan at Rs 5,500 is cheaper.

Gold loan at 12 per cent (a more realistic rate from a mid-tier NBFC): interest payments of Rs 6,000 plus a Rs 500 fee = Rs 6,500. Now the personal loan at 14 per cent (Rs 4,892) wins.

The crossover point depends heavily on the personal loan rate you actually qualify for. Check your CIBIL first and then compare. For a deeper read on improving the score to get better personal loan rates, our disciplined-saver mindset guide is a useful start point.

When a gold loan is the right call

Gold loan wins clearly in four situations.

First, when you need money in under 24 hours. Personal loan disbursal at banks takes 3-5 working days even on paper, often longer in practice. A gold loan at an NBFC branch is 30 minutes to 2 hours. For a medical emergency or a deal you need to close, this matters.

Second, when your CIBIL is below 700. Personal loan rates for a score above 700 start at 11-12 per cent. Below 650, you either get rejected or get quoted 20-24 per cent. Gold loan rates do not depend on your CIBIL at all because the loan is secured by the jewellery. You will get the same 9.99 per cent rate at Muthoot as a salaried earner with 800 CIBIL.

Third, when the loan size is small (under Rs 1 lakh) and short (under 6 months). The personal loan processing fees and the per-EMI overhead make small loans uneconomical. A 6-month, Rs 30,000 gold loan with bullet repayment is dramatically simpler and often cheaper.

Fourth, when you do not want a fresh entry on your credit report. Personal loans show up on CIBIL and affect future loan eligibility. Gold loans from NBFCs sometimes appear on CIBIL and sometimes do not (it depends on the NBFC’s reporting policy). Banks report all gold loans.

When a personal loan or other route is better

Three situations where the gold loan is the wrong choice.

If the loan is for a long tenure (over 24 months). Bullet repayment becomes expensive because you carry the full principal for the entire tenure. EMI-based gold loans are available, but the rates and fees often add up to more than a personal loan at the same tenure.

If you cannot reliably repay. Default leads to an auction of the gold. Family jewellery has emotional value that no auction proceeds will restore. Better to take a personal loan, where default damages your CIBIL but does not lose you the gold.

If the alternative is using your emergency fund. The whole purpose of an emergency fund is to avoid loan dependence. Use it. Rebuild it later. The savings on the avoided interest more than justify the emergency fund drawdown for a genuine short-term need.

What can go wrong and how can you protect yourself

The biggest risk in gold loans is the gold price falling sharply during the tenure. If the price falls by more than 15-20 per cent, the loan can become under-collateralised at the lender’s marked-to-market check, and the lender can issue a top-up demand. If you do not deposit the top-up within the notice period (usually 7-15 days), they have the right to auction the gold without further consultation. In a flat or rising gold market this risk is theoretical, but it has bitten borrowers in past correction cycles.

The second risk is appraisal disputes. The lender’s appraiser will value the gold based on their tests (touchstone, sometimes XRF). Your bangles might test slightly below 22 carat, and you will get a lower loan than you expected. Always ask for the appraisal sheet showing carat purity and net weight. If you disagree, walk to another lender. Different appraisers come up with different numbers on the same jewellery.

The third risk is the auction itself. Read the loan agreement carefully for the auction process: notice period, reserve price method, and your right to recover the surplus if the auction proceeds exceed the loan dues. Reputable NBFCs follow the RBI-mandated process, but the small print varies.

Always get the gold weighed and tested in your presence at pledge time, get a clear receipt with carat, net weight, and gross weight, and keep the original gold loan agreement safe along with the original purchase bills (where available) for the jewellery. Read our term insurance basics guide if you are simultaneously thinking about life cover for the loan tenure, since most secured loans should be life-covered for the outstanding amount.

FAQs

What is the maximum loan to value (LTV) ratio for a gold loan in India in 2026?

The RBI’s LTV cap depends on loan size. For gold loans up to Rs 2.5 lakh, the maximum LTV is 85 per cent of the appraised value of the gold ornaments. For loans between Rs 2.5 lakh and Rs 5 lakh, the cap is 80 per cent. For loans above Rs 5 lakh, the standard 75 per cent cap applies. The appraisal is done on the net weight of the gold (gross weight minus stones, hooks, soldering) and uses the prevailing market price of 22-carat gold on the day of disbursement.

Which lender gives the lowest gold loan rate in India in 2026?

The State Bank of India typically has the lowest published starting rate at around 8.7 per cent per annum for standard gold loans, followed by HDFC Bank at 9.2 per cent. Among NBFCs, Muthoot Finance and Manappuram Finance start their gold loan rates at 9.99 per cent on flagship schemes but go higher with longer tenure or higher LTV. The lowest advertised rate is not always available to all borrowers; the actual offer depends on the loan amount, tenure, and the scheme variant. Always check the all-in cost, including processing fees.

Can I take a gold loan with a low CIBIL score?

Yes. Gold loan eligibility does not depend on your CIBIL score because the loan is secured by the jewellery itself. The lender takes physical possession of the gold, and the rate, tenure, and disbursement are based entirely on the gold’s appraised value. This makes gold loans the natural choice for borrowers with low CIBIL or no credit history. Some lenders still pull your CIBIL for documentation and may report the gold loan to bureaus, so check the lender’s reporting policy if you want to keep this loan off your credit report.

What happens if I cannot repay my gold loan in India?

The lender will issue an EMI default notice followed by a demand notice. After a notice period (typically 15-30 days for the demand notice plus additional auction notice), the lender has the legal right to auction your pledged gold to recover the outstanding loan amount plus interest and charges. If the auction proceeds exceed your dues, the surplus is paid back to you. If proceeds fall short, the lender can pursue you for the shortfall, though in practice this rarely happens because the LTV margin protects them.

Is it cheaper to take a gold loan or a personal loan for Rs 50,000 over 12 months?

It depends on your personal loan rate. A gold loan at 10 per cent bullet repayment costs around Rs 5,500 in interest and fees over 12 months. A personal loan at 14 per cent EMI costs about Rs 4,892 because EMI amortisation reduces the average outstanding balance. But a personal loan at 18 per cent (for lower CIBIL borrowers) costs about Rs 6,008, making the gold loan cheaper. The crossover point sits around a personal loan rate of 15-16 per cent for a 12-month tenure.