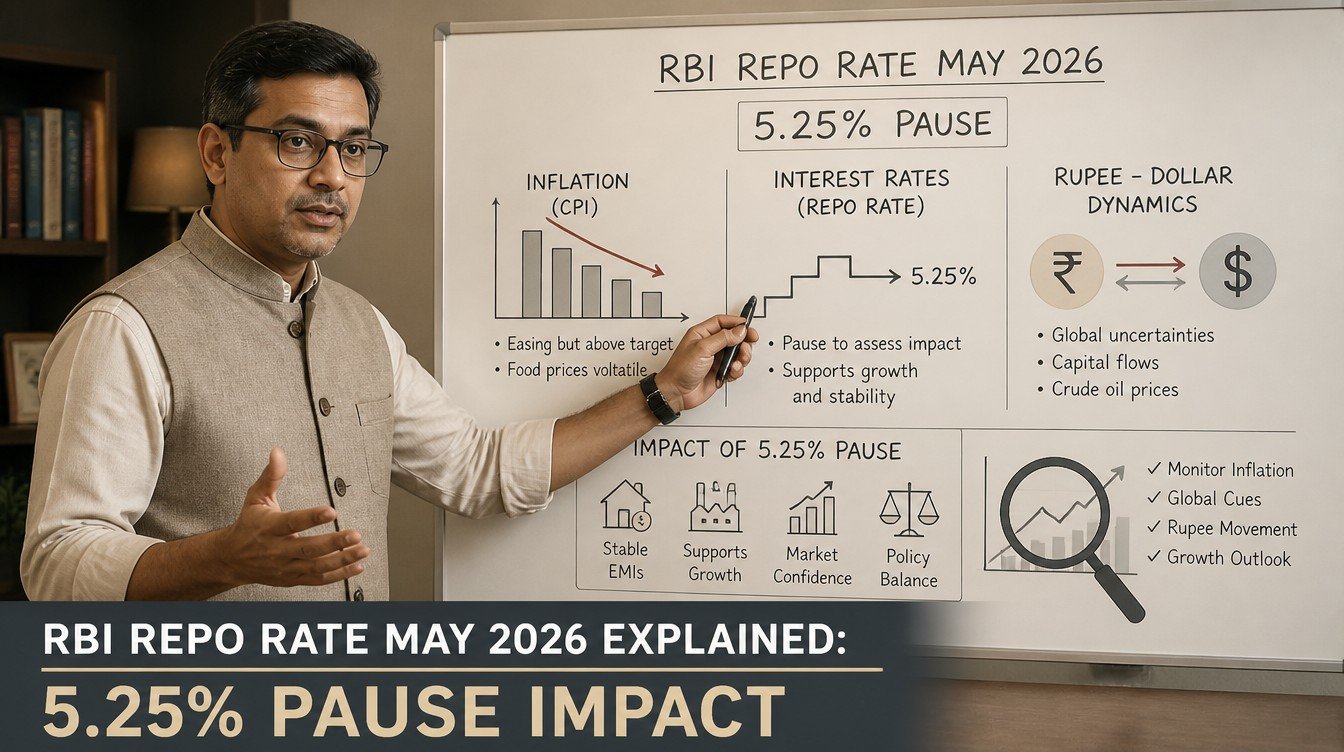

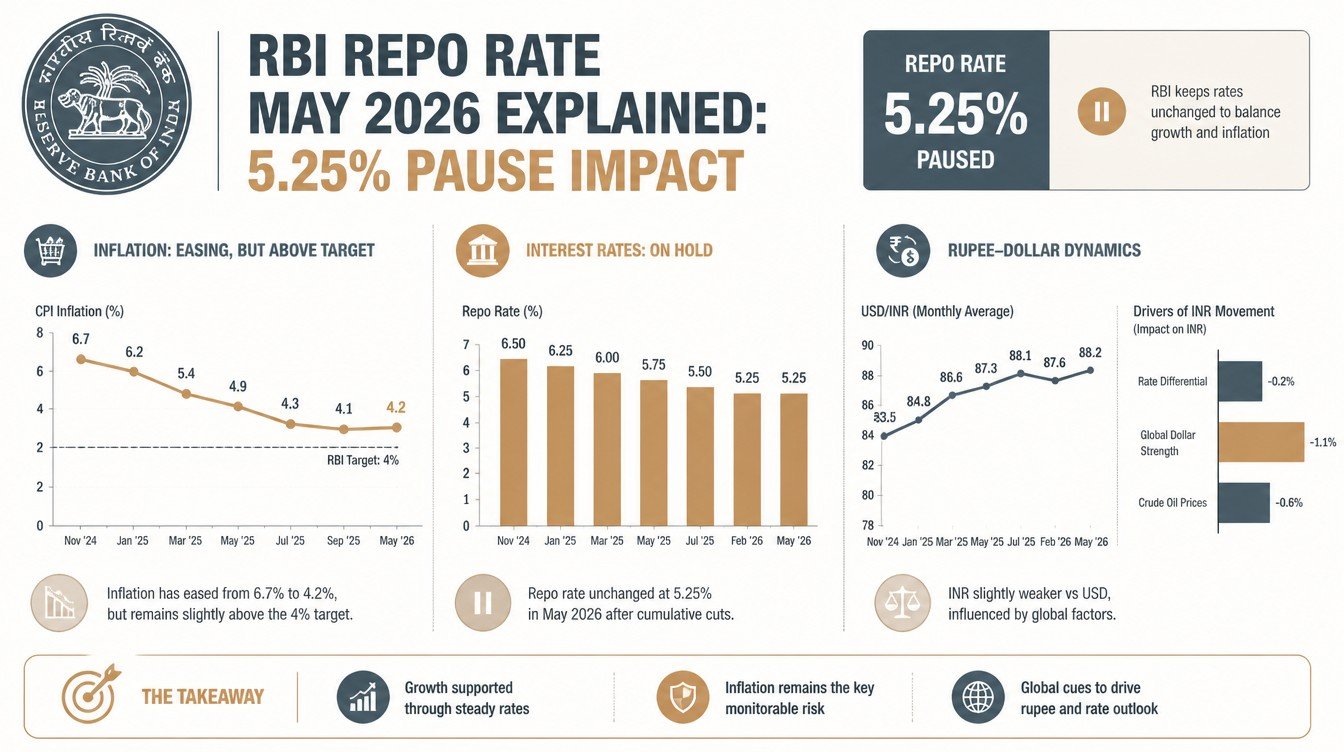

The Reserve Bank of India’s Monetary Policy Committee chose to hold the policy repo rate at 5.25% at its April 2026 meeting, ending a brisk easing cycle and forcing every Indian household to re-examine borrowing, saving, and investing assumptions. This rbi repo rate may 2026 explained guide unpacks the pause in plain English, walks through the MPC statement section by section, and translates it into concrete decisions on home loan EMIs, fixed deposits, small savings schemes, equities, and bonds.

What changed between February 2025 and April 2026 is dramatic. The MPC cut the repo by a cumulative 125 basis points over that window, taking the policy rate from 6.50% down to 5.25%. The April decision was unanimous and the stance was kept at neutral, signalling that the bar for the next move (either up or down) is now meaningfully higher than it was three months ago.

The thesis of this article is simple. A pause is not the same as a peak, and it is not the same as the end of the cycle. For Indian savers, borrowers, and investors, the question is how to position a portfolio when the central bank is on the sidelines, inflation is in range but watchful, and global growth is rattled by geopolitics.

The RBI April 2026 MPC Statement, in Plain English

The April 2026 MPC met from April 6 to April 8 and delivered a unanimous decision to keep the repo rate at 5.25%. The Standing Deposit Facility (SDF) rate stayed at 5.00%. The Marginal Standing Facility (MSF) and Bank Rate stayed at 5.50%. The committee retained the neutral policy stance.

The MPC framed the pause around two ideas. First, a long easing cycle needed time to transmit fully into bank lending and deposit rates. Second, fresh global uncertainty, including renewed tensions in West Asia, has lifted the risk of imported inflation through oil and supply chains. The committee judged that holding fire while watching transmission was the more prudent choice.

What the rate corridor now looks like

The policy corridor in India is anchored by the SDF (the floor) and the MSF (the ceiling), with the repo sitting in between. With SDF at 5.00% and MSF at 5.50%, the corridor remains a tight 50 basis points around the 5.25% repo. This tells money markets that the operating overnight rate is meant to hover close to the repo, with the call money rate as the daily report card.

How the projections shifted

For FY 2026-27, the MPC projected real GDP growth at 6.9% and CPI inflation at 4.6%. Quarterly CPI was cited around 4.0% in Q1, 4.4% in Q2, 5.2% in Q3, and 4.7% in Q4 of FY27. The Q3 bump partly reflects an unfavourable base effect rather than a fresh demand-side surge.

Stance: why neutral matters

A neutral stance means the MPC has explicitly told markets it is data-dependent. It is not pre-committing to cuts and it is not pre-committing to hikes. In practice, neutral is a holding pattern that buys time for the committee to read incoming CPI prints, monsoon outcomes, fiscal trajectory, and global rate moves before its next decision in early June 2026.

Why RBI Paused After 125 bps of Cuts

To grasp the April pause, look at the easing arc behind it. The repo started this cycle at 6.50%. Between February 2025 and the early months of FY 2026-27, the MPC delivered cumulative cuts of 125 basis points in steady increments, taking the policy rate to 5.25%. The pivot from cutting to pausing was less about an inflation scare and more about giving prior cuts room to do their work.

Transmission was already deep but uneven

External Benchmark Lending Rate (EBLR) loans, especially home loans sanctioned after October 2019, repriced quickly because they are mechanically pegged to the repo. MCLR-linked loans, older retail loans, and many corporate loans took longer. Deposit rates lagged even further because banks compete on liability pricing more slowly than they cut asset pricing.

Inflation is in range but not in the rear-view mirror

CPI inflation has cooled toward the RBI’s 4% midpoint with room around it. But the projected lift in Q3 of FY27 and the new oil and West Asia risks mean the committee has no incentive to spend more rate ammunition right now. A pause preserves optionality.

External risks are louder than they were

Global growth is uneven, the US Federal Reserve is cautiously easing on its own track, and crude oil has had volatile months. The rupee has been under pressure against the US dollar in 2026, hovering around the Rs.86 per dollar zone for stretches. A premature additional rate cut while the rupee was already soft could have widened the interest rate differential with the US and pressured the currency further.

RBI Repo Rate May 2026 Explained: A Short History of This Cycle

To frame the pause, look at the rough arc of policy rate moves through this cycle. The numbers below summarise the public direction of travel and are intended to anchor a conversation about how quickly Indian rates have descended from their post-pandemic peak.

| Phase | Approximate Repo Rate | What the MPC was doing |

|---|---|---|

| Pre-cut peak (early FY 2024-25) | 6.50% | Holding at terminal rate, watching inflation come down |

| First cut (February 2025) | 6.25% | Start of the easing cycle, 25 bps cut |

| Mid-cycle (during FY 2025-26) | 5.50% to 5.75% | Series of further cuts as CPI eased |

| February 2026 print | 5.50% | One of the final cuts of the cycle |

| April 2026 MPC | 5.25% | Pause after a 25 bps cut earlier in the year, neutral stance |

| May 2026 (status quo) | 5.25% | Awaiting June 3-5 MPC, no off-cycle action |

A common rule of thumb in Indian personal finance is that 125 basis points of cumulative easing should noticeably move EMIs on floating-rate retail loans. For a borrower with a Rs.50,00,000 (50 lakh) home loan running on EBLR, that swing maps to roughly a four-figure monthly EMI saving, all else equal. The exact number depends on tenure, spread, and reset cadence.

What the Pause Means for Home Loan Borrowers

Home loan borrowers should treat this pause as the end of the free ride down. Floating-rate loans linked to the repo through EBLR will keep repricing inside their normal 90-day window, but the next leg of EMI relief now depends entirely on whether the June 2026 MPC delivers another cut.

EBLR borrowers will see prior cuts settle in

If your sanction letter says the rate is tied to a repo-linked benchmark, your bank is contractually obligated to reset within roughly three months of a policy move. By May 2026, most lenders should have absorbed all of the prior cuts of FY 2025-26 in their statements. Pull your latest provisional interest certificate, confirm the new effective rate, and check whether tenure or EMI was adjusted.

MCLR borrowers still have catch-up to do

Many older home loans are linked to Marginal Cost of Funds Based Lending Rate. MCLR moves slower, and many borrowers will still be paying somewhat above where EBLR equivalents sit. Borrowers in this group should run a switch math (one-time conversion fee versus expected savings) before assuming the easing cycle has helped them as much as it could.

Tenure or EMI: pick once, deliberately

When EMIs fall after a cut, banks typically reduce tenure by default rather than EMI. That is fine if you want to retire the loan faster, but it is not always optimal. Borrowers who would rather free up cash flow now should write to the bank and request EMI reduction in lieu of tenure cut. Get this in writing.

Should you prepay now?

If the floating-rate home loan now sits in the high-7% to 8% range and the borrower has spare cash earning less in liquid funds or sweep-in deposits, partial prepayment continues to make arithmetic sense. The pause does not change that math. Prepay either in lump sum at year-end (after the tax benefit math is final) or in regular extra-EMI installments over the year.

What the Pause Means for Personal Loans, Car Loans, and MSME Borrowers

The repo cycle’s footprint extends well beyond home loans. Personal loans, top-ups, and car loans are mostly priced at fixed spreads over EBLR or MCLR, while MSME borrowers swing between sector-specific schemes and floating-rate working capital limits.

Personal loans and car loans

Effective personal loan rates have eased a little this cycle, but the spread between repo and personal loan rates is wide because of credit risk. Do not expect personal loan APRs to compress sharply just because the repo dropped 125 bps. The right move is still to compare two or three lenders before signing.

MSME and working capital lines

MSME floating-rate facilities follow repo with a lag. If a small business is paying double-digit interest on overdraft or cash credit lines, it is worth requesting a fresh sanction letter from the lender now that the cycle has settled, and asking for a sharpened spread in light of an unchanged credit profile.

Impact on Fixed Deposits and Small Savings Schemes

For savers, a pause is the first whiff of stability after a long, uncomfortable decline in deposit rates. Banks were able to cut FD rates aggressively as the repo fell. Now that the repo has paused at 5.25%, the marginal pressure to cut deposit rates further fades, though banks will continue tinkering with FD slabs based on their own liquidity needs.

Bank fixed deposits: what the pause changes

Bank FD rates in 2026 for one to three year buckets have drifted into the mid-6% range at most large banks, with small finance banks paying somewhat higher. The pause is unlikely to deliver a fresh FD rate cut wave immediately. Savers who still need to deploy idle cash can ladder FDs across 12, 18, 24, and 36 months to average out future rate moves.

Senior citizen FDs and special tenors

Senior citizens benefit from the usual 50 basis points premium on most FDs. Special tenors (444 days, 555 days, etc.) often carry a small extra. Read the term sheet carefully, since these are non-standard and may have separate premature withdrawal rules.

Small savings schemes: politically administered, not market priced

Public Provident Fund (PPF), Sukanya Samriddhi, National Savings Certificate (NSC), Senior Citizen Savings Scheme (SCSS), and the Post Office Monthly Income Scheme are reviewed quarterly by the Ministry of Finance. The Ministry uses a formula linked to G-Sec yields but exercises discretion on the final notification. Through the easing cycle, small savings rates have been kept relatively sticky compared with bank FDs, preserving their attractiveness for risk-averse savers.

Practical FD ladder for the pause

- Park a base liquidity cushion in a sweep-in savings account that auto-converts excess balance into short FDs.

- Place 25% of medium-term savings in a 12-15 month FD, 25% in 18-24 months, 25% in 36 months, and 25% in 5-year tax-saving FD if the 80C limit has room.

- Use the senior citizen bracket where eligible and verify TDS thresholds against Form 15H.

Equity Markets Read: What 5.25% Means for Indian Stocks

Equity investors love rate cuts because lower rates compress the discount rate used to value future cash flows and improve credit conditions. A pause is more ambiguous. It is not a fresh tailwind, but it also removes one source of uncertainty.

Rate-sensitive sectors

Banks, NBFCs, real estate, autos, and consumer durables are the classic rate-sensitive blocks of the Indian market. The first three benefit from cheaper funding; the last two benefit from cheaper EMIs on the demand side. With the repo held at 5.25%, these sectors keep the cumulative benefit they already got, but new tailwinds from this lever go on pause.

Defensives and exporters

IT services, pharma, and FMCG are less directly rate-sensitive. They respond more to dollar revenue mix, US demand, and rural consumption respectively. With the rupee in the Rs.86 per dollar zone, IT services in particular get a transactional currency tailwind that is not directly tied to the MPC.

Equity valuations and earnings

Indian large-cap valuations remain elevated relative to long-term averages. A pause keeps the rate component of the discount rate steady, so the next leg of returns has to come from earnings growth rather than further multiple expansion. Market-linked instruments carry market risk, and past performance is not indicative of future returns.

SIPs should not flinch at a pause

A pause in the policy cycle is not a reason to stop, pause, or accelerate equity SIPs. Goal-based SIPs are designed to weather rate cycles. The rebalancing trigger should be asset allocation drift, not the MPC calendar.

Bond Market Read: G-Secs, Bond Funds, and Duration Calls

The pause is most directly relevant for bond holders. Indian government securities (G-Secs) had a strong run as the cycle eased. With the repo now paused, the next leg of bond price gains needs either fresh cuts or a sharper fall in inflation expectations.

10-year G-Sec at around 7%

The 10-year G-Sec yield in 2026 has hovered roughly in the 6.8% to 7.1% area. For a salaried investor, that yield is competitive with most bank FDs of comparable tenor, and G-Sec interest is sovereign-backed though still taxable as per slab. Yields could drift either way around this level depending on MPC tone and global rates.

Bond funds: what duration to own?

During the easing cycle, longer-duration funds (gilt funds, 10-year constant maturity funds) outperformed because their prices rose as yields fell. With the pause, the calculus changes. Short-duration and medium-duration debt funds offer more predictable accrual at current yields with less mark-to-market noise. Long-duration funds still have a place for goal-based bond holdings but expected price gains from further duration calls are now narrower.

RBI Retail Direct for buying G-Secs

RBI’s Retail Direct platform lets Indian residents buy G-Secs, T-Bills, SDLs, and Sovereign Gold Bonds directly. For investors who want sovereign credit, predictable cash flow, and a transparent yield, Retail Direct is worth a serious look in this rate environment. The platform is free for the retail investor.

What Should Indian Investors Actually Do This Quarter?

The simplest playbook is to act on transmission rather than predicting the next MPC move.

Three-step checklist for borrowers

- Pull the latest interest certificate from the lender, confirm the effective rate, and check whether tenure or EMI was reduced after the prior cuts.

- If on MCLR, evaluate the cost of switching to EBLR by comparing the one-time fee with annualised savings.

- If sitting on idle cash earning less than the home loan rate, plan a partial prepayment for the next quarter end.

Three-step checklist for savers

- Refresh the FD ladder so the next 12 months of liquidity needs are covered with maturing FDs.

- Top up PPF and Sukanya Samriddhi early in FY 2026-27 to maximise compounding.

- Use Form 15G/15H to manage TDS on FD interest where eligible.

Three-step checklist for investors

- Audit asset allocation versus the target, rebalance if any sleeve drifts more than five percentage points.

- Decide debt allocation duration: short-to-medium duration for predictability, long duration only if there is a clear view on further cuts.

- Continue equity SIPs and avoid lump-sum timing decisions tied to MPC calendars.

Forward Look: The June 2026 MPC and Beyond

The next MPC meeting is scheduled for June 3 to June 5, 2026. The committee has six meetings scheduled across FY 2026-27, in line with the standard bi-monthly cadence. Each meeting will be read by markets for the vote split, the stance language, and the projection updates as much as for the headline rate decision.

Three scenarios markets are pricing

The first scenario is a continuation of the pause at 5.25% with neutral stance. This is the path most analysts seem to lean toward as the base case while inflation and global risks settle. The second is a final 25 basis points cut to 5.00%, if domestic CPI undershoots and rupee pressure eases. The third is no change for the next several meetings, with the easing cycle effectively complete at 5.25%. Each is plausible, none is guaranteed.

What to watch between now and June

CPI prints for April and May 2026, the monsoon outlook, oil prices, the rupee’s path against the dollar, and the Federal Reserve’s signals will dominate the run-up to the next MPC. Borrowers and investors should not try to front-run these data points but should know what would change the picture for the central bank.

How to read the next MPC like a pro

When the June MPC statement drops, look for three things. First, the vote split. A 6-0 unanimous decision signals strong consensus; a 4-2 split signals brewing disagreement. Second, the stance: any change from neutral to accommodative or vice versa is the bigger headline. Third, the projection table: any meaningful change to FY27 GDP or CPI projections is the substantive macro signal.

Common Mistakes Indian Savers and Borrowers Make Around an MPC Pause

A pause confuses people who expect every MPC to deliver a directional move.

Locking long FDs in a panic about rates falling further

Some savers heard “pause” and rushed to lock five-year FDs at the assumption that rates would now fall further. That is a possibility but not a certainty. Laddering, not lump-sum locking, is the more resilient approach when the central bank itself is hedging.

Refusing to switch from MCLR to EBLR

Some borrowers stay on MCLR because the conversion fee feels like a sunk cost. Run the actual math. For a residual tenure of 10-plus years and a clear spread differential, the payback period on a switch is often well under a year.

Chasing yield in lower-rated corporate debt

When G-Secs and bank FDs settle in the mid-6% to 7% range, some investors get tempted by AA or AA-minus corporate paper or unlisted debt offering 9-10%. Yield does not come without credit risk. Stick to high-credit-quality debt for the safety sleeve of a portfolio.

Trying to time the SIP based on rate calls

Stopping or restarting SIPs around MPC dates is one of the most common goal-destroying habits in Indian retail investing. The fixed amount, fixed date discipline of an SIP is precisely what survives rate cycles.

How the RBI Repo Rate Sits in the Broader Macro Picture

It helps to zoom out. The repo rate is one lever among several. Fiscal policy, public capex, regulatory tightening, and the rupee’s path all interact with it.

Fiscal arithmetic and bond supply

Central and state government borrowing programmes feed directly into G-Sec yields. A heavier borrowing calendar can lift yields even if the repo is unchanged. Watch the Union Budget 2026 numbers and the half-yearly borrowing calendar from RBI.

The rupee, FII flows, and the differential

If the US Federal Reserve cuts more slowly than expected, the interest rate differential narrows and rupee comes under pressure. RBI typically responds with measured intervention rather than rate moves, but a sustained currency stress could limit how much further the MPC can ease.

India’s growth story remains the anchor

FY 2026-27 GDP growth projected at 6.9% keeps India among the fastest-growing major economies. That alone gives the central bank some comfort that holding rates here is not choking activity. A growth slowdown surprise, however, would re-open the cutting door.

FAQs on the RBI April 2026 Repo Rate Pause

What is the current RBI repo rate in May 2026?

The RBI repo rate in May 2026 stands at 5.25%, unchanged after the April 2026 MPC meeting. The SDF is at 5.00%, the MSF and Bank Rate are at 5.50%, and the policy stance is neutral. The next MPC meeting is scheduled for June 3 to June 5, 2026.

How much has RBI cut the repo rate in the current cycle?

Cumulative cuts in the current easing cycle have totaled 125 basis points, taking the repo from 6.50% down to 5.25% between February 2025 and early FY 2026-27. The April 2026 MPC then paused further moves.

Will my home loan EMI drop again after this pause?

Floating-rate home loans on EBLR will continue to reflect the cumulative cuts already delivered as banks complete their roughly 90-day reset cycles. Any further EMI relief from this lever depends on whether the MPC delivers another cut at a future meeting. Borrowers should confirm the new effective rate on their loan and decide whether to keep the lower EMI or shorten the tenure.

Are bank FD rates likely to fall further now?

With the repo on pause, the pressure to cut FD rates eases. Banks may still trim selective slabs based on their own liquidity, but the broad descent in deposit rates that accompanied the cuts is less likely to continue at the same pace while the repo is steady. Savers can ladder FDs across tenors rather than locking everything at a single maturity.

Is this the end of the rate-cut cycle in India?

It is too early to call the cycle finished. The MPC has explicitly kept a neutral stance and said it will be guided by incoming data on inflation, growth, the rupee, and global conditions. Markets are watching the June 2026 MPC for the next read. Forward-looking statements should be treated as possibilities, not certainties.

Related guides on EBLR mechanics, FD laddering, bond fund duration, and how to read the MPC statement section by section are forthcoming on LearnFineEdge.