The itr-u updated return india 2026 framework is now one of the most powerful late-filing tools in the Income Tax Act. The Finance Act 2025 extended the ITR-U window from 24 months to 48 months from the end of the relevant assessment year, which means a taxpayer who missed reporting some income in FY 2025-26 can still file a corrective ITR-U as late as 31 March 2031. The catch is that the additional tax scales sharply over those four years, from 25% in the first 12 months to 70% in the fourth year.

This guide explains who is eligible to file ITR-U, the year-wise additional tax slabs that decide the cost, where ITR-U sits relative to a revised return under Section 139(5) and a rectification under Section 154, and the situations where running through ITR-U is actually the rational choice. The numbers reflect Section 139(8A) as amended by the Finance Act 2025; every filer should still confirm the latest CBDT notification before filing.

What is ITR-U and why was the window extended

ITR-U is the updated return introduced through Section 139(8A) of the Income Tax Act. It exists specifically so that taxpayers can voluntarily declare income that was missed, under-reported, or wrongly classified in an earlier return.

Origin under Finance Act 2022

ITR-U was originally introduced in Budget 2022 with a 24-month window. The idea was to give the Department a structured channel for voluntary corrections, without forcing every disclosure through the reassessment route under Section 148.

Extension to 48 months under Finance Act 2025

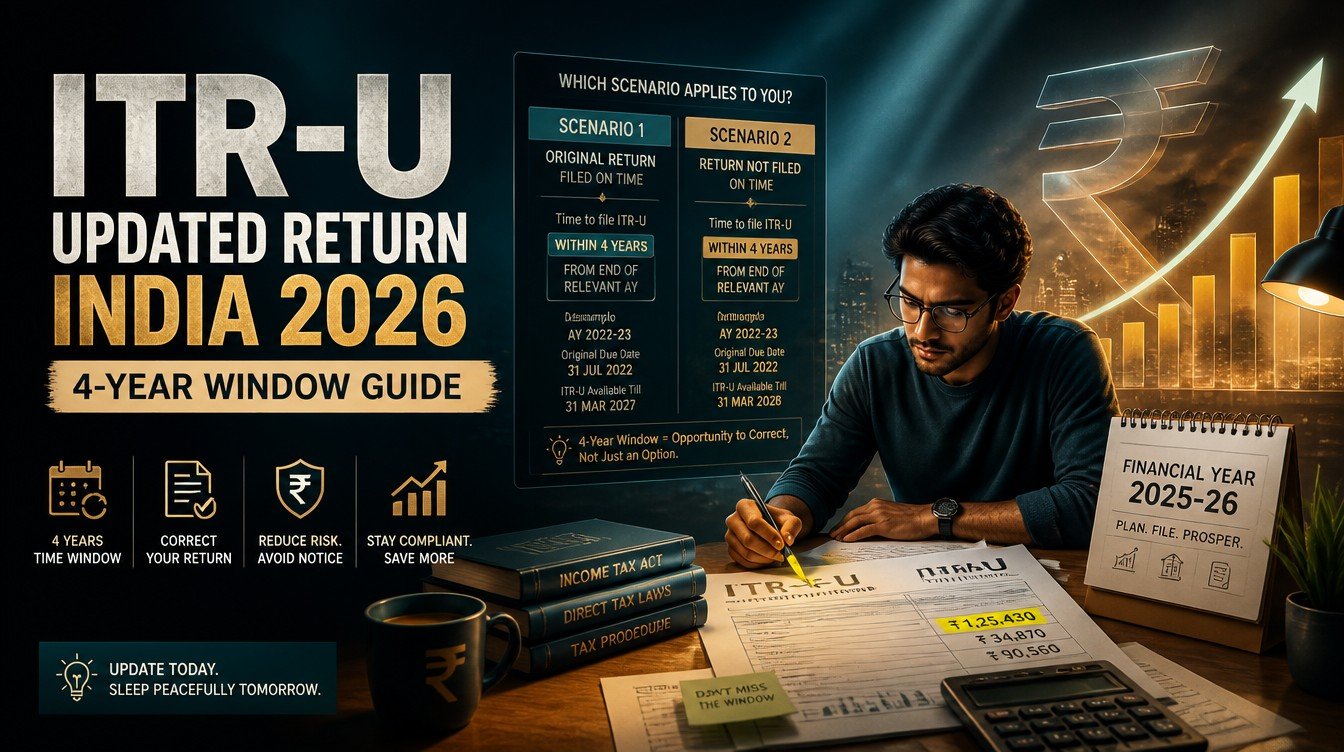

The Finance Act 2025 doubled the available window to 48 months from the end of the relevant assessment year. For FY 2025-26 income (AY 2026-27), the extended window now runs through 31 March 2031. The trade-off is a higher additional-tax rate in the third and fourth years to discourage indefinite procrastination.

What ITR-U cannot do

ITR-U is a one-way street toward higher tax. It cannot be used to claim a fresh refund that did not exist in the original return. It cannot reduce the previously declared tax liability beyond very narrow conditions. It also cannot be filed in years where the additional submission would not produce extra tax payable, although the Finance Bill 2026 has proposed targeted relaxations such as allowing carried-forward loss reductions.

Eligibility for ITR-U

Most individual taxpayers can use ITR-U, but the law lays out a specific set of conditions and exclusions.

Who can file ITR-U

- Any taxpayer who failed to file a return in the original window

- Any taxpayer who filed but missed some income

- Any taxpayer who reported the wrong head of income or wrong rate

- Any taxpayer who declared the wrong tax credit or carried forward an incorrect loss

Who cannot file ITR-U

- Cases where the return would result in a refund or an increase in refund

- Cases where total declared income or loss would reduce

- Years already under search, survey, prosecution, or specific information from another authority

- Years where an assessment, reassessment, recomputation or revision order is already passed and pending

How the eligibility check happens

The e-filing portal at incometax.gov.in runs a pre-check before allowing an ITR-U submission. If the form computes a refund, a reduction in tax, or hits any of the exclusion grounds above, the submission is blocked at validation. This is by design, since ITR-U is a voluntary disclosure mechanism, not a corrective utility.

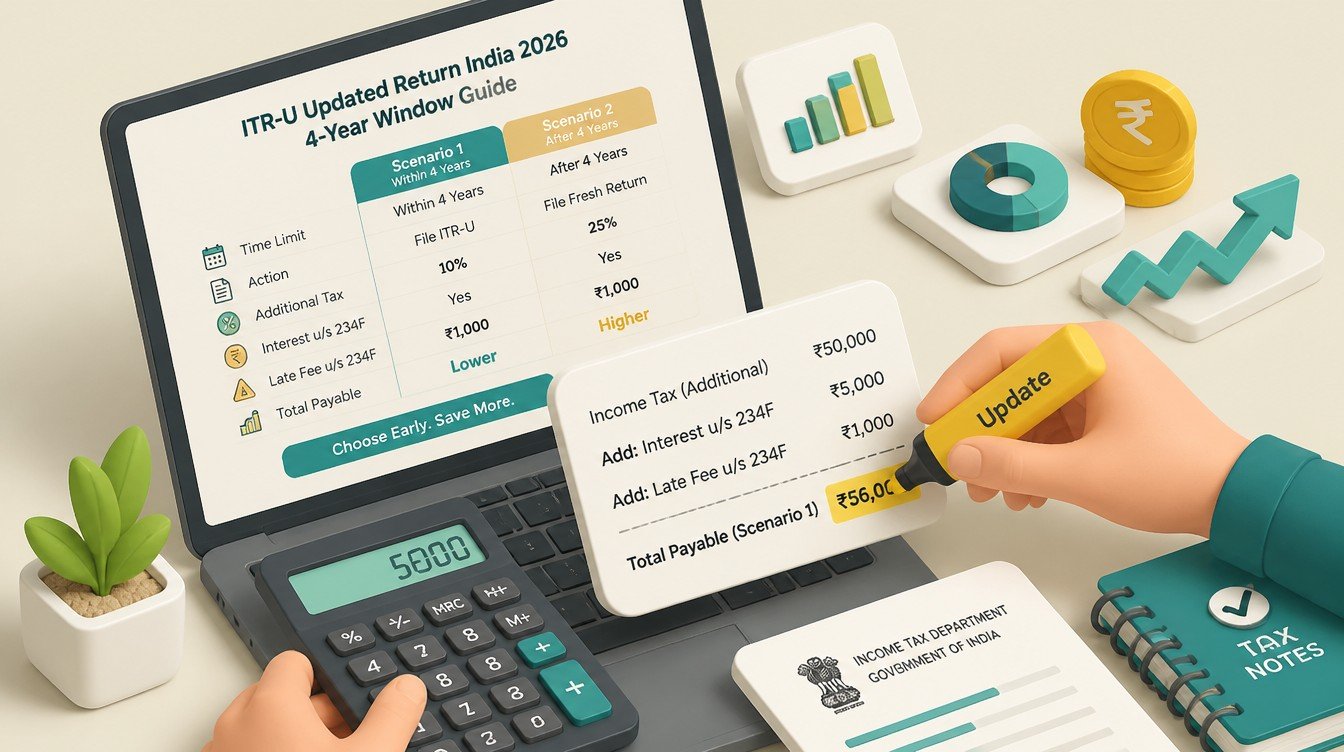

Year-wise additional tax: 25%, 50%, 60% and 70%

The defining feature of ITR-U is the additional tax that escalates the longer the taxpayer waits.

The four bands

| Time elapsed from end of relevant assessment year | Additional tax over the regular tax plus interest | Last date for FY 2025-26 (AY 2026-27) |

|---|---|---|

| Up to 12 months | 25% | 31 March 2028 |

| 12 to 24 months | 50% | 31 March 2029 |

| 24 to 36 months | 60% | 31 March 2030 |

| 36 to 48 months | 70% | 31 March 2031 |

Worked example

Assume a salaried filer in FY 2025-26 missed declaring Rs.4,00,000 of freelance income, on which the additional regular tax liability works out to Rs.80,000 plus Section 234A and 234B interest of approximately Rs.10,000. Filing ITR-U in March 2028 (within 12 months) requires an additional 25% over (Rs.80,000 + Rs.10,000), i.e. Rs.22,500. Filing the same correction in March 2030 (third year) requires 60% over the same base, i.e. Rs.54,000.

Why the timer matters so much

The additional tax is computed over the aggregate of tax and interest, not just tax. The longer the wait, the larger the interest base, and the higher the marginal multiplier on top. In practical terms, every year of delay can roughly increase the cost of correction by 10-15 percentage points of the underlying liability.

How ITR-U differs from a revised return

It helps to map the three correction routes available to a filer.

Revised return under Section 139(5)

A revised return is available only until the end of the relevant assessment year. For FY 2025-26, that is 31 March 2027. It can change any element of the original return, including increasing or decreasing the tax. There is no additional tax penalty layered on the revision itself.

ITR-U under Section 139(8A)

ITR-U becomes the only voluntary correction route once 31 March 2027 has passed. It cannot reduce liability or create a fresh refund, and it attaches the year-wise additional tax described above.

Rectification under Section 154

Section 154 rectification is for mistakes apparent from the record, after a 143(1) intimation or assessment order. It cannot be used to declare missed income. The distinction is operational: 154 corrects what the Department already saw and processed; ITR-U declares something the Department had not been told.

Step-by-step: filing ITR-U for FY 2025-26 income

The mechanics are similar to a regular ITR filing, with extra fields specific to the updated return.

Step 1: Reconfirm the original return is on record

Pull up the original ITR acknowledgement and Form 26AS. If no original return was filed, ITR-U can still be used, but the additional tax and Section 234F late fee both apply.

Step 2: Recompute total income with the missed item

Add the omitted income to the relevant schedule. Examples include freelance receipts not reported, capital gains on a property sale that did not appear in AIS, or interest income on a long-running fixed deposit. Re-run the slab math under the same regime originally chosen.

Step 3: Compute regular tax and interest first

Calculate the incremental tax that would have been payable if the missed item had been declared in the original return, plus Section 234A interest from the original due date and Section 234B interest where applicable.

Step 4: Layer the ITR-U additional tax

Apply 25%, 50%, 60% or 70% depending on which year window the filing falls into. Pay the total via the e-pay tax facility and quote the challan in the ITR-U form.

Step 5: Submit the ITR-U through the portal

Select ITR-U as the form type, attach the reason for the updated return from the dropdown (for example, return previously not filed, income not reported correctly), and submit. E-verify within 30 days.

When ITR-U makes financial sense

Even with the additional tax, ITR-U is often the cheaper option compared to the alternatives.

Versus a reassessment notice under Section 148A

If the Department picks up the discrepancy independently, a Section 148A notice can trigger a full reassessment, with penalty under Section 270A at up to 200% of the tax on under-reported income. ITR-U at 25% looks inexpensive next to a 200% penalty.

Versus prosecution risk

Wilful non-disclosure above thresholds can attract prosecution under Section 276C. ITR-U closes that door for the year covered, provided the filing is voluntary and not after a search or survey.

Where ITR-U does not help

If the original return already reported the income but at the wrong rate, and the correction would reduce tax, ITR-U cannot help. The route there is rectification under Section 154 if it qualifies, or an appeal under Section 246A if it does not.

Common scenarios that trigger an ITR-U

Three categories of income are showing up most often in updated-return filings.

Crypto and VDA gains

From 1 April 2026, Indian crypto exchanges share data with the IT Department under the new reporting framework. Filers who under-declared VDA gains in earlier years have a clear motivation to file ITR-U before the data-sharing exposes the gap.

Freelance and consulting receipts

Indian-resident consultants paid from overseas often have receipts visible in bank statements but not in Form 26AS. AIS now picks up many of these inflows. ITR-U is the corrective route for past years.

Capital gains on property sales

Property sales above stamp-duty thresholds are reported by sub-registrars under SFT. A capital gain not reported in the original return tends to surface during AIS reconciliation. ITR-U is the standard fix.

Documentation to keep with an ITR-U

An ITR-U filing is more scrutinised than a regular return, so the record should be airtight.

Source documents for the missed income

Invoices, bank credits, broker statements, and any TDS certificates for the missed income. These should be filed and indexed in case a notice arrives later.

Computation working

A clean working that shows opening tax, incremental tax on missed income, Section 234A and 234B interest, and the additional ITR-U tax. The same working should match the challan paid.

Acknowledgement of original return

Even if the original return is more than a year old, keep the acknowledgement. ITR-U is treated as an update over the original, and reconciliation can be requested by CPC.

Common mistakes filers make with ITR-U

A few patterns of error keep recurring at CPC.

Filing ITR-U to claim a refund

ITR-U is the wrong form for any correction that would lead to a refund. The portal will reject the submission, and the filer loses time.

Missing the additional-tax computation

Some filers compute only the incremental tax and forget the 25% to 70% additional layer. The return is then short-paid and treated as defective.

Filing ITR-U during a pending assessment

If a notice under Section 148A or an assessment order is already in motion, ITR-U is not available. The correction has to ride through the reassessment, where the rate structure is harsher.

Choosing the wrong regime

ITR-U requires the same regime that was used (or available by default) in the original year. Trying to switch regimes through ITR-U is a common rejection ground.

Frequently asked questions

Until when can ITR-U be filed for FY 2025-26?

The extended window under the Finance Act 2025 allows ITR-U for FY 2025-26 up to 31 March 2031. The additional tax rises across that window, from 25% in the first 12 months to 70% in the fourth year.

Can ITR-U be used to claim a refund I missed?

No. ITR-U cannot be used to claim a refund or reduce previously declared tax. If your correction would lower tax or generate a refund, the only routes are a revised return within the original window or a rectification under Section 154 if eligible.

Is Section 234F late fee payable with ITR-U?

If the original return was not filed in time, Section 234F applies along with the ITR-U additional tax. If the original return was filed in time, only the additional tax and interest layers apply on the incremental income.

Is ITR-U available for every assessment year?

ITR-U is available for the four assessment years immediately preceding the current financial year, subject to the exclusions in Section 139(8A). The exact eligibility for older years should be verified on the portal before payment.

Does ITR-U protect against penalty under Section 270A?

A voluntary, timely ITR-U filing for under-reported income generally avoids the Section 270A penalty for that income, since the disclosure precedes Department action. This protection ends once a Section 148A notice or search/survey starts.

Related guides on revised returns, belated return penalty math, and reassessment timelines under Section 148 are forthcoming on this site.