The ULIP-versus-mutual-fund debate has been rerun every year since the 2010 IRDAI charge-cap reforms, and the answer keeps shifting as tax rules and fund-management costs change. In 2026, with the Rs.2,50,000 (2.5 lakh) annual-premium ceiling for ULIP tax-exemption under Section 10(10D) firmly in place and Long-Term Capital Gains on equity mutual funds taxed at 12.5 percent above the Rs.1,25,000 (1.25 lakh) annual threshold, the math is no longer a simple “ULIP wins on tax” or “MF wins on returns”.

This guide settles the ulip vs term india 2026 question with a 20-year worked example using the same monthly outflow, the full charge structure of a typical ULIP, and the realistic post-tax outcome of the term-insurance-plus-index-fund route. The goal is not to crown a winner for everyone; it is to give you a calculation you can replicate with your own numbers before signing either policy form.

If you have ever sat through a bank-relationship-manager pitch that ended with a ULIP brochure and an “it’s the same as a mutual fund with insurance free” line, this is the article that does the actual arithmetic.

What A ULIP Actually Is, Stripped Of Marketing

A unit-linked insurance plan is a single contract that bundles a life-insurance cover with a market-linked investment account, and charges you separately for both layers. The premium you pay each year is split into mortality charges (the genuine insurance cost), policy administration charges, fund management charges, and, in older designs, a premium-allocation charge that takes a slice off the top before any of it reaches the investment side.

The remaining amount buys units in one or more chosen funds, each of which behaves like a small mutual fund inside the policy wrapper. The unit balance, less applicable charges, is what the policyholder sees as the fund value. On maturity or earlier surrender after the five-year lock-in, that fund value is paid out subject to tax rules covered later.

Where the charges actually land

The 2010 and 2019 IRDAI reforms forced ULIP charges into a much narrower band than the pre-2010 products, but they did not eliminate them. A modern 2026 ULIP from a large insurer typically carries fund management charges in the 1.25 to 1.35 percent annual range, policy administration of Rs.500 to Rs.6,000 per year, and mortality charges that scale with age and sum-at-risk. The total drag in the first five years can still be meaningfully higher than a direct-plan mutual fund.

The “discontinuance” trap most buyers miss

If premiums stop within the first five-year lock-in, the fund value is moved to a discontinued-policy fund that earns a low fixed rate (typically the savings-account-rate band) and is paid out after the lock-in ends. This sounds protective but in practice it converts a high-conviction equity bet into a low-yield holding pen for several years, and the discontinuance charges that apply in the early years can erase a meaningful slice of the corpus.

Switching between funds within the ULIP

ULIPs allow tax-free switching between the equity, debt, and balanced funds inside the policy, and this is one of the genuine structural advantages of the wrapper. A mutual-fund investor who rebalances between an equity fund and a debt fund triggers a tax event each time, while the ULIP holder does not. The size of this advantage depends on how often you actually rebalance, which for most retail investors is once a year at most.

What “Term + Mutual Fund” Actually Means

The alternative route splits the same monthly budget into two separate products. A pure-term insurance policy buys protection for the household, and the difference between the term premium and the original ULIP outflow goes into a direct-plan equity mutual fund, typically a broad index fund or a low-cost large-cap fund.

Why the term cover gets larger

For the same Rs.12,000 monthly outflow, the term-plus-MF route almost always buys a meaningfully larger life cover because the term plan is priced as pure mortality risk without the investment-side overhead. A 32-year-old non-smoker buying Rs.1,00,00,000 (1 crore) of pure term cover pays roughly Rs.12,000 to Rs.15,000 per year in 2026, while a comparable ULIP might bundle Rs.10,00,000 (10 lakh) of cover with a Rs.12,000 monthly investment.

Why the investment side runs leaner

A direct-plan Nifty 50 or Nifty 500 index fund carries a total expense ratio of roughly 0.15 to 0.30 percent in 2026. A direct-plan actively managed large-cap fund runs in the 0.6 to 0.9 percent range. Either way, the long-term drag is below half of what a typical ULIP fund charges, and over a 20-year horizon that gap compounds into a number that is hard to ignore.

The discipline question

The strongest argument for ULIPs is that the five-year lock-in forces discipline. An honest comparison has to acknowledge this. Some investors who chose the term-plus-MF route in 2010 stopped the SIP during the 2013 taper tantrum, the 2020 pandemic crash, or the 2022 drawdown, and ended up worse off than the ULIP buyer who could not exit. The wrapper is not the only thing that drives outcomes; behaviour does.

The ULIP Charge Stack, Item By Item

Reading a ULIP benefit illustration without understanding the charge stack is the most common cause of buyer’s remorse three years in. Each of the following charges is disclosed in the policy document; the issue is that they are usually buried in a table the seller never walks the buyer through.

- Premium allocation charge: Older ULIPs took 4 to 10 percent of the premium off the top in the first few years before any of it was invested. Modern 2026 designs from large insurers have largely reduced this to zero or to a small first-year-only deduction, but always check.

- Policy administration charge: A monthly flat charge, typically Rs.40 to Rs.500 per month, deducted by cancelling units. On smaller premiums this is a meaningful drag because it is fixed in rupee terms.

- Fund management charge (FMC): Annual percentage charge on assets under management, typically 1.25 to 1.35 percent for equity funds in the wrapper. This is the biggest single drag over a 20-year horizon.

- Mortality charge: The pure-cost-of-insurance line. Rises with age. Deducted monthly by cancelling units. For older policyholders or higher sums at risk, this becomes the dominant drag in the later years.

- Switching charges: Most modern ULIPs offer a generous number of free switches per year (commonly unlimited), with a small charge thereafter.

- Premium discontinuance charge: Applies if you stop paying premium before completing the five-year lock-in. Tapered downward by policy year.

- Surrender charge: Effectively zero after the five-year lock-in for IRDAI-compliant products.

What total cost-to-NAV typically looks like

A buyer-facing way to think about all of these together is to ask, “What percentage of my fund value is the wrapper eating each year?” In a competitive 2026 ULIP from a large insurer, that number is typically 1.6 to 2.2 percent in the first five years, settling to 1.4 to 1.8 percent thereafter, including mortality. A direct-plan index fund runs at 0.15 to 0.30 percent. That gap is the entire argument.

Where ULIPs have genuinely improved

It is fair to say that post-2019 ULIPs from listed life insurers are dramatically better than the products that gave the category its bad name in the 2000s. Charge caps, simpler disclosure, and competitive pressure from mutual funds have all compressed the wrapper cost. The category is no longer indefensible; it is just usually still more expensive than the direct-plan alternative, and the tax advantage that historically offset the cost has narrowed sharply.

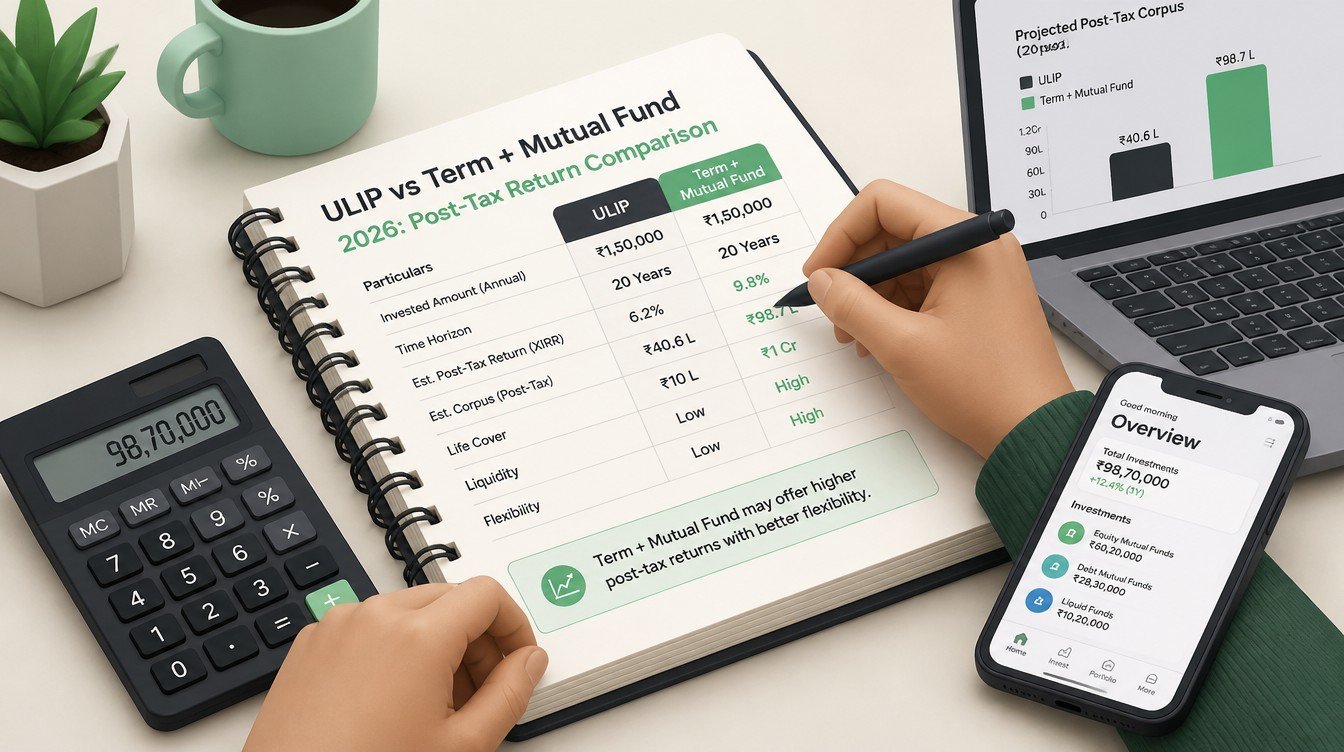

The 20-Year Worked Example: Same Premium, Two Paths

The cleanest way to compare the two paths is to run the same monthly outflow through each over the same 20-year horizon with the same gross equity-market assumption. The example below uses Rs.12,000 per month (Rs.1,44,000 per year), a starting age of 32, a non-smoker male, and a long-term equity return assumption of 11 percent per year before charges. Numbers are illustrative and meant for comparison, not as a return forecast.

| Line Item | ULIP Path | Term + Index Fund Path |

|---|---|---|

| Annual outflow | Rs.1,44,000 | Rs.1,44,000 |

| Life cover | Rs.15,00,000 (15 lakh) | Rs.1,00,00,000 (1 crore) |

| Term premium | Bundled | ~Rs.13,000 / year |

| Annual amount reaching equity | ~Rs.1,28,000 (after charges) | ~Rs.1,31,000 (after term premium) |

| Annual drag on invested amount | ~1.6 percent (FMC + admin + mortality) | ~0.20 percent (index fund TER) |

| 20-year illustrative corpus (pre-tax) | ~Rs.78,00,000 (78 lakh) | ~Rs.95,00,000 (95 lakh) |

| Tax on maturity (premium > Rs.2.5 lakh? No, exempt under 10(10D)) | Nil | LTCG 12.5% above Rs.1.25 lakh annual exemption |

| Estimated post-tax outcome | ~Rs.78,00,000 | ~Rs.86,00,000 to Rs.88,00,000 |

How to read the table

The ULIP route in this example keeps the entire maturity payout tax-free because annual premium is below the Rs.2,50,000 (2.5 lakh) ceiling, which is its single biggest structural advantage. The term-plus-MF route faces LTCG tax of 12.5 percent on equity gains above the Rs.1,25,000 (1.25 lakh) annual exemption when units are sold, which dents the post-tax number. Even after that dent, the lower charge structure and the larger life cover mean the second route still ends up in a comparable or better post-tax position in this base case.

What changes the answer

The answer flips depending on three variables. If your annual ULIP premium would exceed Rs.2,50,000 (2.5 lakh), the wrapper loses Section 10(10D) exemption and the gains are taxed as capital gains, which closes most of the ULIP’s tax advantage. If your mutual-fund redemption pattern is large lumpsum sales rather than gradual swp-style withdrawals, the LTCG hit on the MF side is heavier. If you switch between equity and debt frequently, the tax-free intra-wrapper switching of the ULIP starts to add real value.

Why the cover gap matters even more than the corpus gap

Look again at the life-cover line in the table. The ULIP buyer carries Rs.15,00,000 (15 lakh) of cover; the term-plus-MF buyer carries Rs.1,00,00,000 (1 crore) of cover for the same outflow. If the earner dies in year three, the ULIP nominee receives roughly Rs.15,00,000 (the higher of sum assured and fund value, subject to product terms), while the term-plus-MF nominee receives the Rs.1,00,00,000 term payout plus the small MF balance built up so far. For a household with dependents, this is the single most consequential difference between the two paths.

Tax Treatment: Section 10(10D), The Rs.2.5 Lakh Cap, And LTCG

Tax rules have done more to reshape the ULIP-versus-MF debate than any product redesign. Three rules matter most in 2026, and getting any of them wrong materially distorts the comparison.

The Section 10(10D) maturity exemption for ULIPs

For ULIPs issued on or after 1 February 2021, the maturity payout is exempt under Section 10(10D) only if the aggregate annual premium across all such ULIPs you hold does not exceed Rs.2,50,000 (2.5 lakh). The aggregation is across policies, not per policy, which closes the older loophole of stacking multiple small ULIPs.

What happens above the Rs.2.5 lakh ceiling

If aggregate annual ULIP premium exceeds Rs.2,50,000 (2.5 lakh), the maturity proceeds of the offending policies are taxed as capital gains. Equity-oriented ULIPs are taxed in line with equity mutual funds: short-term gains at 20 percent if the holding period is up to 12 months, and long-term gains at 12.5 percent above the Rs.1,25,000 (1.25 lakh) annual exemption beyond that. Debt-oriented ULIPs in this band are taxed at the policyholder’s slab.

Tax on mutual fund redemption

On the mutual-fund side, redemption of equity-oriented funds attracts LTCG of 12.5 percent above the Rs.1,25,000 (1.25 lakh) annual exemption for holding periods over 12 months. Short-term gains within 12 months are taxed at 20 percent. Systematic Withdrawal Plans (SWPs) are a tactical lever, because spreading redemptions across financial years can keep each year’s gain within or close to the Rs.1,25,000 exemption.

Death benefits

Death benefits under both ULIPs and pure term plans remain fully exempt under Section 10(10D), regardless of premium size. This is one of the cleanest tax features of life insurance in India and is the reason term cover should be evaluated on protection grounds, not tax grounds.

Who Should Actually Consider A ULIP In 2026

There is a small but real set of profiles for which a ULIP is the right call in 2026, even after the tax tightening. The mistake is to over-extend that set into the wider buying population.

The Rs.2 lakh-or-less annual premium investor with no MF discipline

An investor whose total annual life-insurance-plus-equity outflow will stay below Rs.2,50,000 (2.5 lakh), who has never built a SIP habit, and who values the five-year lock-in as a forcing function may find a competitively priced ULIP useful. The tax exemption is fully available, the lock-in protects the corpus from behavioural exits, and the charge gap versus a direct-plan MF is partially offset by the tax-free switching.

The frequent rebalancer

An investor who genuinely rebalances between equity and debt several times a year captures real value from tax-free intra-wrapper switching. For most retail investors this is a theoretical advantage that they never use, but for a disciplined goal-based rebalancer it is worth something.

The high-net-worth investor stacking allocation

Above the Rs.2,50,000 (2.5 lakh) annual ULIP premium ceiling, the tax advantage disappears and a ULIP is essentially a charge-heavy equity vehicle with a life cover. In that band, term-plus-direct-plan-MF is almost always the cleaner answer, supplemented by PMS or category-specific MF allocations where appropriate.

Who should not buy a ULIP

Anyone with dependents who has not first secured a pure-term cover of the right size should not buy a ULIP first. The ULIP bundles a small life cover that is almost always inadequate, and the buyer ends up under-insured while believing they are “covered”. Term cover is the foundation; any equity-investment wrapper is secondary.

How To Evaluate A ULIP Benefit Illustration Without Getting Sold

A benefit illustration is a regulator-mandated document that shows projected fund value at 4 percent and 8 percent gross return assumptions. The numbers are useful only if you read them with a few corrections in mind. These are the practical steps to take when an agent hands you the illustration.

- Check the FMC and confirm it is included in the projection. Some illustrations show fund value before deducting FMC; ask explicitly.

- Add up the year-by-year mortality charge over the policy term. Over 20 years, mortality charges on a moderately sized cover can total Rs.2,00,000 to Rs.4,00,000. This is real money.

- Compare the 8% projection to a direct-plan index fund running at 0.2% TER. Run the same monthly outflow at 8% gross with 0.2% drag; compare the ending corpus. The gap is the cost of the wrapper.

- Confirm the premium-to-sum-assured ratio. If annual premium exceeds 10 percent of sum assured, Section 10(10D) exemption is lost for that policy regardless of the Rs.2.5 lakh ceiling.

- Read the discontinuance terms. Understand what happens if you cannot pay premium in years 3 or 4. This is where most regret accumulates.

The two questions that cut through the pitch

Two questions reliably separate well-suited ULIP buyers from mis-sold ones. First: “What is the total annual outflow I am committing for the next five years, and can I sustain it through a job change?” Second: “If I bought a pure-term cover of Rs.1,00,00,000 (1 crore) and put the difference into a direct-plan index fund, how does the 20-year outcome compare?” If the seller cannot or will not run the second number, the conversation should pause.

The “ULIP top-up” lever

Most ULIPs allow top-up premiums above the regular premium. Top-up premiums above 10 percent of sum assured are not eligible for Section 80C deduction and may not qualify for Section 10(10D) exemption. Treat the regular premium as the binding number for the tax-exemption test; do not assume top-ups carry the same treatment.

Common Mistakes In The ULIP-vs-MF Decision

Most mis-pricing of the decision comes from a handful of recurring errors. Each of these is correctable if the household runs the numbers on its own outflow profile.

- Treating the ULIP’s bundled life cover as adequate protection. It almost never is. Cover sizing should come from a needs-based calculation, not from whatever the wrapper happens to include.

- Comparing ULIP “8 percent illustration” to a mutual-fund “20-year average return” number. These are not comparable. Use the same gross-return assumption for both paths and let the charges speak for themselves.

- Forgetting the LTCG hit on the MF side. Skipping the tax leg flatters the MF route. The honest comparison applies LTCG above Rs.1.25 lakh per year on equity MF redemptions.

- Ignoring switching frequency. If you actually rebalance equity-to-debt every year, the ULIP’s tax-free switching is worth something real. If you do not, that advantage is theoretical.

- Buying a ULIP because “tax planning is sorted”. Under the new tax regime, Section 80C is unavailable, and the premium-side deduction that historically made ULIPs attractive is gone for new-regime taxpayers.

The endowment-plus-ULIP stacking trap

Some buyers stack a traditional endowment plan, an old ULIP from the 2000s, and a new ULIP, then declare their “investments are in insurance”. Pure-term cover is almost always inadequate in this stack, and the blended return on the corpus side is usually below a basic balanced fund. Untangling the stack typically means surrendering the older endowment after the lock-in, buying pure term cover, and redirecting the freed-up premium into a direct-plan equity fund.

The “guaranteed” return brochure

If a ULIP brochure or an agent’s pitch uses the word “guaranteed” for the equity-fund portion, the conversation should end. Equity ULIPs are market-linked; only the death benefit is guaranteed. Some non-linked endowment products are sometimes confused with ULIPs in agent-led conversations; check the policy document classification before signing.

Decision Framework: A Five-Step Test

The framework below collapses the entire decision into five sequential questions. Run them in order, and if any one fails, the answer flips to term-plus-MF.

- Do you already have adequate pure-term cover sized to your actual needs? If no, buy term first; pause the ULIP conversation entirely.

- Will your aggregate annual ULIP premium across all policies stay below Rs.2,50,000 (2.5 lakh) for the policy’s full term? If no, the Section 10(10D) exemption is unavailable for the gains, and the wrapper’s tax advantage disappears.

- Can you commit the premium through job changes and life events for at least five years? If no, the discontinuance trap will hurt you. Choose an MF SIP, which you can pause without losing units to a low-yield holding fund.

- Will you actually use the tax-free intra-wrapper switching feature at least once a year? If no, you are paying for an option you will not exercise.

- Have you compared the 8 percent ULIP projection to a direct-plan index fund at 0.2 percent TER for the same outflow? If the ULIP loses by more than 10 percent over 20 years, the wrapper is not worth it for you.

What “yes to all five” looks like in practice

A 35-year-old salaried investor with a 30-year-old spouse, an existing Rs.1,50,00,000 (1.5 crore) term cover, an annual ULIP premium plan of Rs.2,00,000 (2 lakh), no other ULIPs in force, a stable job in a non-volatile sector, an actual rebalancing discipline, and a benefit illustration that comes within 5 percent of a direct-plan index fund over 20 years is the genuine ULIP candidate. This is a narrower buyer profile than the category is sold to.

What “no on any one” looks like

If any of the five fails, the calmer alternative is a pure-term cover sized by the household’s actual needs plus a direct-plan equity index fund SIP. The combination is simpler to administer, cheaper in charges, and provides a much larger life cover for the same monthly outflow.

The Behavioural Argument For ULIPs, And Why It Has Weakened

The strongest pro-ULIP argument has always been behavioural rather than mathematical: the five-year lock-in stops nervous investors from selling at the bottom. This is a real benefit, and dismissing it sounds clever but ignores how most household-level investing actually fails.

What has changed about the MF side

Direct-plan index funds with mandatory long-term goal tagging, the AMFI-driven discipline around SIP renewals, and the rise of platform-level “lock” features that prevent panic redemptions have closed a meaningful slice of the behavioural gap. A goal-tagged SIP into a direct-plan Nifty 500 index fund, set up with auto-debit and reviewed annually rather than monthly, replicates much of the discipline a ULIP enforces.

Where the ULIP’s discipline still helps

For investors who have repeatedly broken their SIP during drawdowns, the ULIP’s hard lock is still a useful guardrail. The honest framing is, “If you have ever stopped a SIP because of a market crash, the ULIP’s lock-in may be worth the higher charges to you.” For investors who have never broken a SIP, the lock-in is a constraint without much benefit.

The portfolio view

A blended approach is sometimes the right answer: a smaller ULIP for the lock-in benefit on a slice of the portfolio, plus a larger MF SIP for the bulk of the allocation, plus a pure-term cover for protection. This is not “either-or”; it is recognising that household finances rarely reduce to a single product.

Frequently Asked Questions

Is the maturity amount from a ULIP fully tax-free in 2026?

The maturity amount from a ULIP issued on or after 1 February 2021 is exempt under Section 10(10D) only if aggregate annual premium across all such ULIPs is at or below Rs.2,50,000 (2.5 lakh). Above that, the gains are taxed as capital gains: equity ULIPs at 12.5 percent above the Rs.1,25,000 (1.25 lakh) annual exemption for holding periods above 12 months.

Which route gives a larger life cover for the same monthly outflow?

The term-plus-mutual-fund route almost always provides a larger life cover for the same monthly outflow, because pure-term premium is priced as mortality risk alone. A typical Rs.12,000-a-month ULIP carries roughly Rs.15,00,000 to Rs.20,00,000 in sum assured, while the same outflow can fund a Rs.1,00,00,000 (1 crore) pure-term cover plus a direct-plan equity SIP.

What is the five-year lock-in and what happens if I stop paying?

ULIPs have a mandatory five-year lock-in. If premiums stop within that window, the fund value moves to a discontinued-policy fund earning a low fixed rate, and any discontinuance charges apply. The corpus is paid out only after the five-year lock-in ends, which can convert a high-conviction equity bet into a low-yield holding pen for several years.

Are direct-plan mutual fund charges really lower than ULIP charges?

Yes, meaningfully. A direct-plan Nifty 50 or Nifty 500 index fund typically runs at a total expense ratio of 0.15 to 0.30 percent in 2026, while a competitive 2026 ULIP carries a wrapper drag of roughly 1.4 to 2.2 percent depending on age and design. Over a 20-year horizon, the difference compounds into a material gap.

Should I switch from an old ULIP to mutual funds?

The answer depends on lock-in status, surrender charges, and the alternative use of the freed-up capital. Most ULIPs issued before 2010 carry heavier wrapper costs and should be reviewed carefully; surrendering after lock-in and redirecting premium into pure term plus a direct-plan index fund usually improves the long-term outcome. Run the numbers before acting, and confirm the surrender value with the insurer in writing.

Related guides on term-cover sizing, mutual-fund taxation, and goal-based SIP planning are forthcoming on LearnFineEdge and will be linked here once published.