Picking the wrong ITR form is the single most common reason a filer receives a defective-return notice under Section 139(9). The itr form selection india 2026 question gets harder every year because the eligibility criteria for ITR-1 keep narrowing, capital gains and crypto increasingly push filers into ITR-2, and any freelance or business income immediately escalates the requirement to ITR-3. This decision-tree guide walks through which form fits which profile for FY 2025-26, the eligibility checklist for each, and the consequences when a defective form is submitted.

The references are to the ITR forms notified by the CBDT for AY 2026-27 alongside the underlying eligibility tests in the Income Tax Act. Filers should still confirm the latest form schema at incometax.gov.in before finalising the choice.

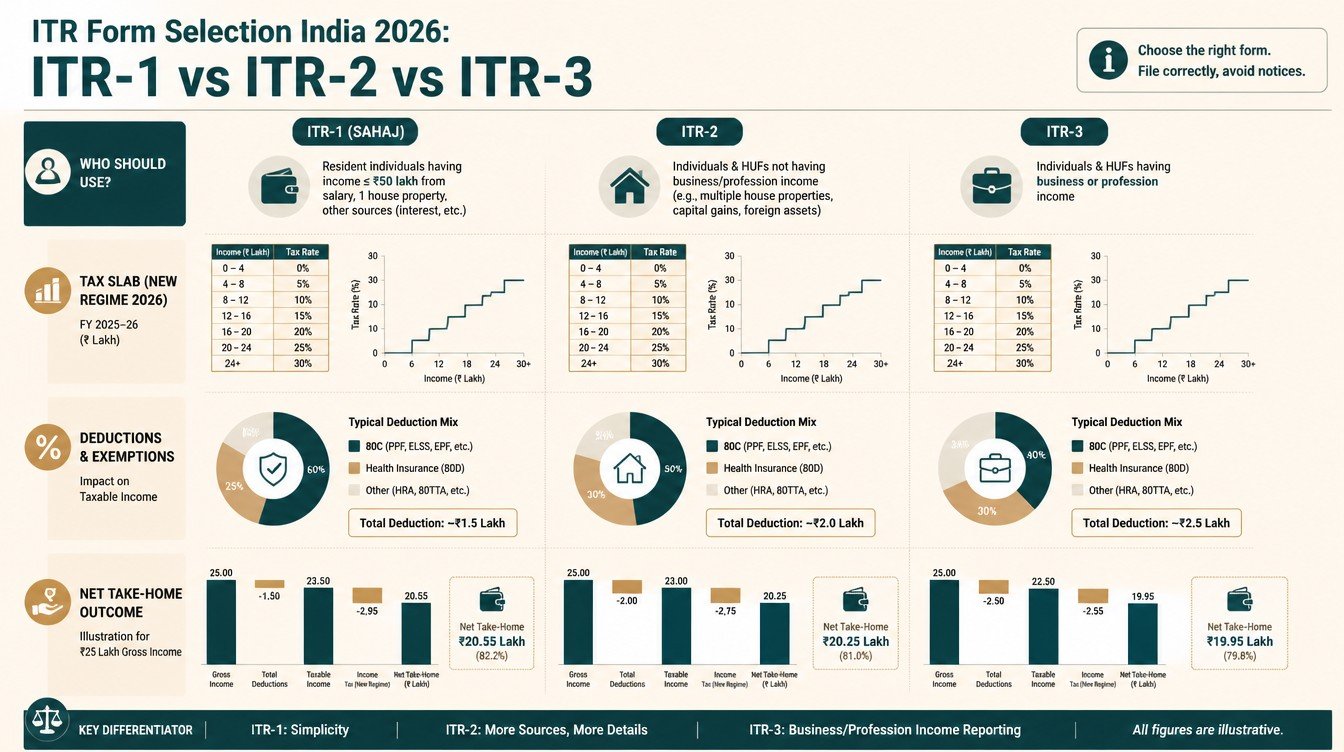

Why itr form selection india 2026 matters more than ever

The seven ITR forms (ITR-1 to ITR-7) target different taxpayer profiles. For individuals, only ITR-1, ITR-2, ITR-3 and ITR-4 are relevant.

The cost of picking the wrong form

A return filed in the wrong form is treated as defective. CPC issues a Section 139(9) notice asking the filer to cure the defect within 15 days. If the defect is not cured, the return is treated as invalid, the original date of filing is lost, and the late-fee plus interest clock keeps running.

Eligibility tests are not all about income

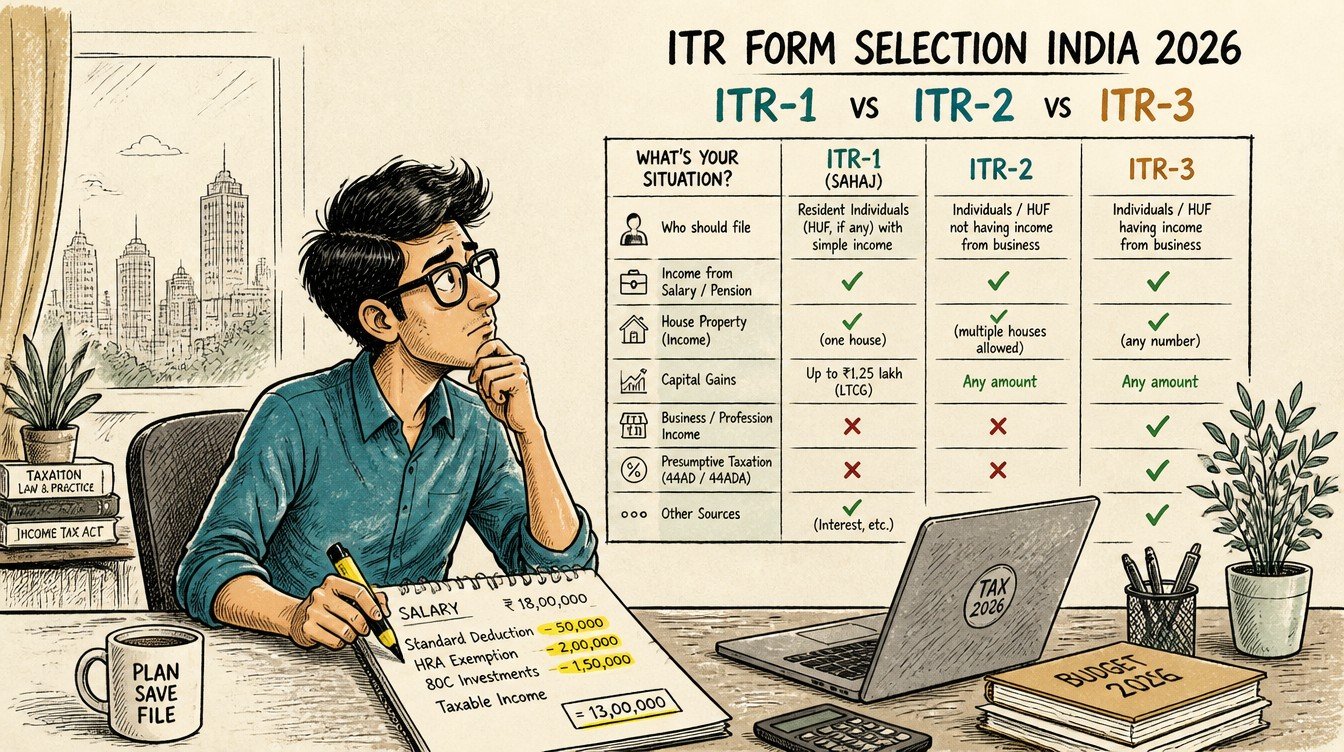

ITR-1 has both an income cap (Rs.50 lakh) and a structural-eligibility test (no capital gains beyond Rs.1,25,000 LTCG on listed equity, no foreign income, no business income, only one house property, no agricultural income above Rs.5,000). A high-income salaried filer might still qualify if the structural tests are passed; a low-income filer with foreign income cannot.

The decision tree, in one paragraph

Start with whether you have business or professional income. If yes, go to ITR-3 (or ITR-4 for presumptive). If no, check whether you have capital gains, foreign assets, more than one house property, or income above Rs.50 lakh. If yes, ITR-2. Otherwise, ITR-1. Each branch has additional fine print.

ITR-1 (Sahaj): the cleanest path

ITR-1 is the shortest and easiest form. It is designed for resident individuals with simple income profiles.

Who can file ITR-1

- Resident individuals (not RNOR, not non-resident)

- Total income up to Rs.50,00,000 (50 lakh) for the year

- Income from salary or pension

- Income from one house property (excluding losses brought forward or carried forward)

- Income from other sources excluding lottery and racehorse income

- Long-term capital gains under Section 112A up to Rs.1,25,000 with no carry-forward of capital losses

- Agricultural income up to Rs.5,000

Who cannot file ITR-1

- Directors of a company

- Filers holding unlisted equity shares

- Filers with foreign assets, foreign income, or signing authority on a foreign account

- Filers with capital gains above Rs.1,25,000 or with any short-term capital gains

- Filers with brought-forward or carry-forward losses

- Filers with more than one house property

Typical ITR-1 filer

A salaried Indian working at a single employer, paying rent in a city, earning bank interest, and possibly selling a small quantity of mutual funds with LTCG under Rs.1,25,000 fits ITR-1 perfectly. The form pre-fills extensively from Form 16, AIS and Form 26AS.

ITR-2: salaried plus capital gains and complexity

ITR-2 absorbs everything ITR-1 cannot handle, short of business income.

Who must file ITR-2

- Individuals and HUFs without any business or professional income

- Filers with capital gains above the Rs.1,25,000 LTCG threshold or any STCG

- Filers with more than one house property

- Filers with foreign income or foreign assets requiring Schedule FA

- Filers with VDA gains under Section 115BBH

- Filers whose income exceeds Rs.50,00,000

- Filers carrying forward or claiming brought-forward capital losses

Common ITR-2 profiles

A salaried filer with equity gains, an NRI taxed on India-sourced income, a senior citizen with multiple properties, or any resident with foreign ESOPs typically files ITR-2. The form is significantly larger than ITR-1 but still excludes business and professional income schedules.

Schedules unique to ITR-2

ITR-2 includes Schedule CG (Capital Gains), Schedule OS (Other Sources with detailed crypto and gambling fields), Schedule VDA, Schedule FA (Foreign Assets), Schedule FSI (Foreign Source Income), and Schedule TR (Tax Relief on doubly-taxed foreign income).

ITR-3: business and professional income

The moment business or professional income appears, ITR-3 is the default.

Who must file ITR-3

- Freelancers and consultants billing under their own PAN

- Doctors, lawyers, architects and other professionals (whether or not under presumptive scheme)

- Sole proprietors and partners in firms (income from partnership)

- F&O traders, since F&O is treated as non-speculative business income

- Intraday equity traders, since intraday is speculative business income

What ITR-3 demands

ITR-3 requires detailed financial statements, a balance sheet for the business or profession, profit and loss schedule, and tax audit information where applicable under Section 44AB. The form is materially heavier than ITR-2.

When ITR-4 is cleaner than ITR-3

Filers eligible for the presumptive scheme under Section 44AD, 44ADA or 44AE can use the much shorter ITR-4 instead. The trade-off is that the presumptive route locks in the assumed margin and limits deductions, which suits some professionals and not others.

ITR-4 (Sugam): the presumptive shortcut

ITR-4 is the presumptive-income version for small businesses and professionals.

Who can file ITR-4

- Resident individuals, HUFs and partnership firms (other than LLPs)

- Total income up to Rs.50,00,000

- Business income under Section 44AD (gross receipts up to Rs.3 crore where digital receipts dominate)

- Professional income under Section 44ADA (gross receipts up to Rs.75 lakh where digital receipts dominate)

- Goods carriage business under Section 44AE

What ITR-4 simplifies

The presumptive route accepts an assumed profit margin (8% in cash, 6% in digital for 44AD; 50% for 44ADA), so the form skips the full balance sheet and detailed P&L. Filers who can live with the assumed margin save substantial compliance effort.

When ITR-4 stops being the right pick

ITR-4 cannot handle capital gains beyond LTCG of Rs.1,25,000, more than one house property, foreign income, or income above Rs.50 lakh. Once any of those appear, the filer is back in ITR-3 territory.

A one-page decision diagram

The decision tree below walks through the choices in sequence.

| Question | If yes | If no |

|---|---|---|

| Do you have business or professional income? | Eligible for presumptive scheme? Then ITR-4. Otherwise ITR-3. | Continue |

| Do you have any capital gains other than equity LTCG up to Rs.1,25,000? | ITR-2 | Continue |

| Do you hold foreign assets, have foreign income, or are an NRI/RNOR? | ITR-2 | Continue |

| Do you have more than one house property? | ITR-2 | Continue |

| Is your total income above Rs.50,00,000? | ITR-2 | Continue |

| Do you have brought-forward or carry-forward losses? | ITR-2 | Continue |

| Are you a director of a company or hold unlisted equity? | ITR-2 | Continue |

| None of the above triggers fired? | ITR-1 | – |

Run this checklist top-down. The first yes determines the form. If every question is answered no, ITR-1 applies.

Common ambiguities the decision tree resolves

A few situations trip filers up consistently.

Single equity trade in the year

Even a single equity sale that produces LTCG above Rs.1,25,000 or any STCG knocks the filer out of ITR-1. The decision tree catches this through the capital-gains question. ITR-2 is the right form even for one small transaction above the threshold.

Foreign ESOPs from an Indian employer’s foreign parent

Vested ESOPs in a foreign parent company create foreign-asset exposure that requires Schedule FA. ITR-2 is mandatory; ITR-1 cannot accommodate Schedule FA.

Multiple house properties

Owning two flats (even self-occupied plus rented) requires ITR-2. ITR-1 explicitly limits to a single house property.

Freelance income alongside salary

A salaried Indian with even small freelance receipts is technically running a profession or business in parallel. The right form is ITR-3 (or ITR-4 if presumptive). ITR-1 is not available.

Consequences of filing the wrong form

The penalty path follows Section 139(9) and is more painful than most filers expect.

Defective return notice

CPC issues a Section 139(9) notice within weeks of submission. The filer has 15 days to cure the defect by filing the correct form. The notice usually arrives via the registered email and the e-filing portal inbox.

Loss of original filing date

If the defect is not cured within the 15-day window (or any extension granted), the return is treated as invalid. The original filing date is then lost, and the late-fee plus interest clock starts ticking again.

Carry-forward of losses

An invalid return cannot be used to carry forward losses. Filers with capital losses or business losses lose the right to set them off against future income if the form is wrong and the defect is not cured.

Refund delays

Refunds claimed on a defective return are blocked until the defect is cured. For larger refunds, this can mean a delay of two to three months.

How to cure a defective return

The cure path is well defined.

Receive and read the notice

The Section 139(9) notice specifies the defect (typically by quoting the schedule that cannot be filled in the chosen form). Read the notice carefully before responding.

File a revised return in the correct form

Login to the e-filing portal, select Revised Return under Section 139(5), pick the correct ITR form, refill the return with the same income data, and submit. The original acknowledgement number is referenced inside the revised return.

E-verify the revised return

E-verification within 30 days is mandatory. An unverified revised return is treated as not filed, exactly as for any other return.

Confirm defect cured

The e-filing portal updates the status to “Defect cured” within a few days. Until that happens, treat the return as still defective.

Salaried filer profiles mapped to forms

A quick mapping helps anchor the decision tree to realistic profiles.

Profile A: single-employer salaried filer with bank interest only

One employer, no capital gains, no business income, income below Rs.50 lakh, single house property (or none): ITR-1.

Profile B: salaried filer with equity gains

Salary plus LTCG above Rs.1,25,000 or any STCG, or any crypto income: ITR-2.

Profile C: dual-employment salaried filer with foreign ESOPs

Two Form 16s in the year, vested foreign ESOPs, capital gains on RSU sales: ITR-2.

Profile D: salaried plus freelance consulting

Salary plus consulting receipts on the same PAN: ITR-3 (regular) or ITR-4 (if presumptive under Section 44ADA applies and gross receipts are within cap).

Profile E: full-time freelancer or trader

No salary, business or professional receipts as the primary income: ITR-3 in general, ITR-4 only when presumptive eligibility is met cleanly.

Frequently confused edge cases

Three edge cases come up repeatedly.

Interest on the income tax refund

Interest on an income tax refund is taxable as Income from Other Sources. It does not by itself bump a filer out of ITR-1 unless it pushes total income above the Rs.50 lakh threshold.

Gift income

Gifts above the Section 56(2)(x) threshold from non-relatives are taxable under Other Sources. ITR-1 can handle small amounts of Other Sources income, but gifts requiring detailed Schedule OS reporting often push the filer into ITR-2.

Co-owned house property

If the filer is a co-owner of a single house with a spouse, the property still counts as one for the filer’s own return. Owning two properties in the filer’s own name pushes the form to ITR-2.

Frequently asked questions

Can a salaried filer with capital gains use ITR-1 for FY 2025-26?

Only if the capital gains are LTCG under Section 112A up to Rs.1,25,000 and there are no other capital gain transactions or carry-forwards. Any STCG, debt fund redemption, crypto sale, or property sale rules out ITR-1.

What form should a freelancer with a Rs.10 lakh annual receipt file?

If the receipts qualify under Section 44ADA (specified professions, presumptive), ITR-4 is available with 50% assumed profit. Otherwise, ITR-3 with regular books of accounts and profit-and-loss schedule.

What happens if I file ITR-1 by mistake when I should have filed ITR-2?

CPC issues a Section 139(9) defective return notice. You have 15 days to file a revised return under Section 139(5) using the correct form. Failure to cure the defect makes the return invalid.

Does selling crypto on a foreign exchange change my form choice?

Yes. Foreign assets and foreign income trigger Schedule FA, which is available only in ITR-2 and beyond. ITR-1 is not eligible.

How long does CPC take to send a defective return notice?

Defective return notices typically arrive within four to eight weeks of submission, depending on processing load. Filers should check the e-filing portal inbox regularly even before any email notification arrives.

Related guides on Schedule VDA, Schedule FA reporting, and revised return filing under Section 139(5) are forthcoming on this site.