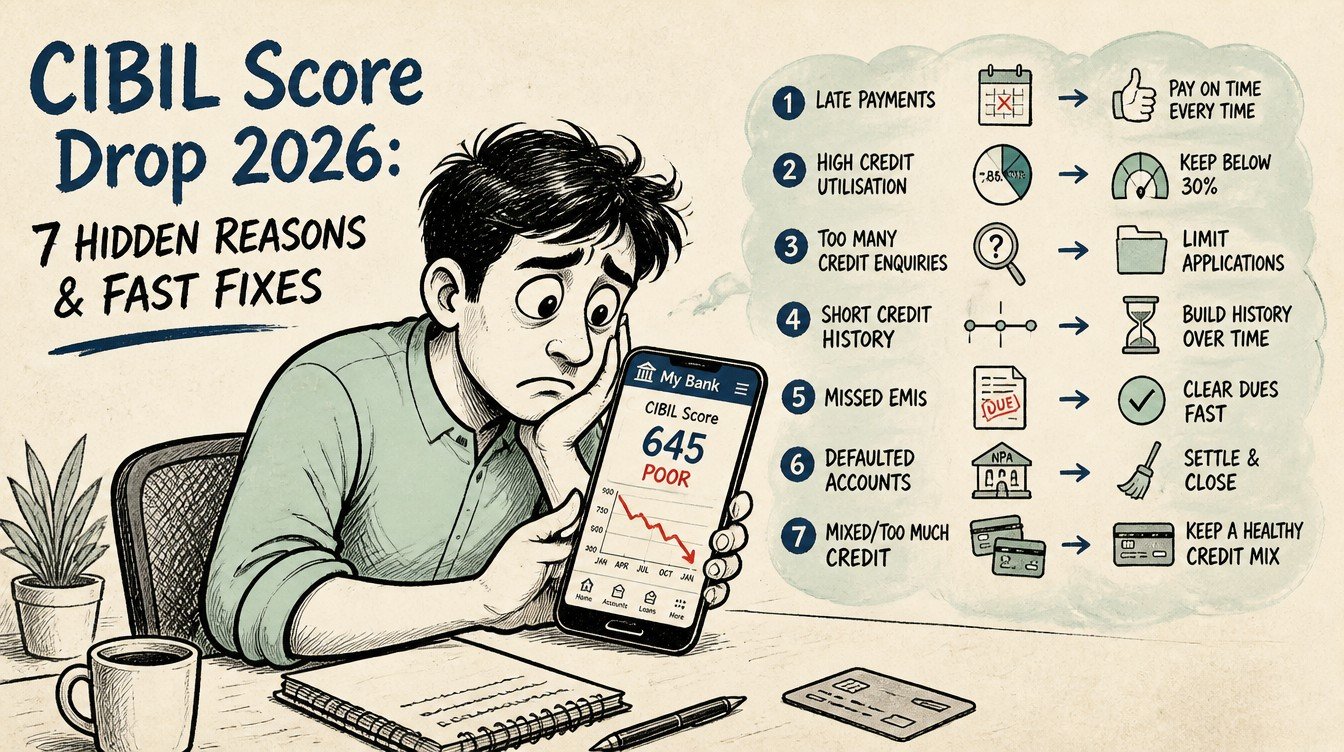

A sudden CIBIL score drop feels personal. The salary went in on time, the EMI did not bounce, and yet the score has slipped twenty or thirty points. Searching for cibil score drop reasons 2026 usually returns the obvious villains: missed payments and credit card defaults. The more interesting story is the second layer of triggers that most salaried Indians never get a clear explanation for, even from their own bank.

This guide unpacks seven of those less-obvious reasons your CIBIL score may have fallen in 2026, paired with one-line fixes that can move the needle within 90 days. It also lists five free ways to pull your CIBIL report, walks through the dispute process step by step, and ends with FAQs that address the cases borrowers most commonly write to financial helplines about.

How CIBIL scoring actually works and why small actions move it

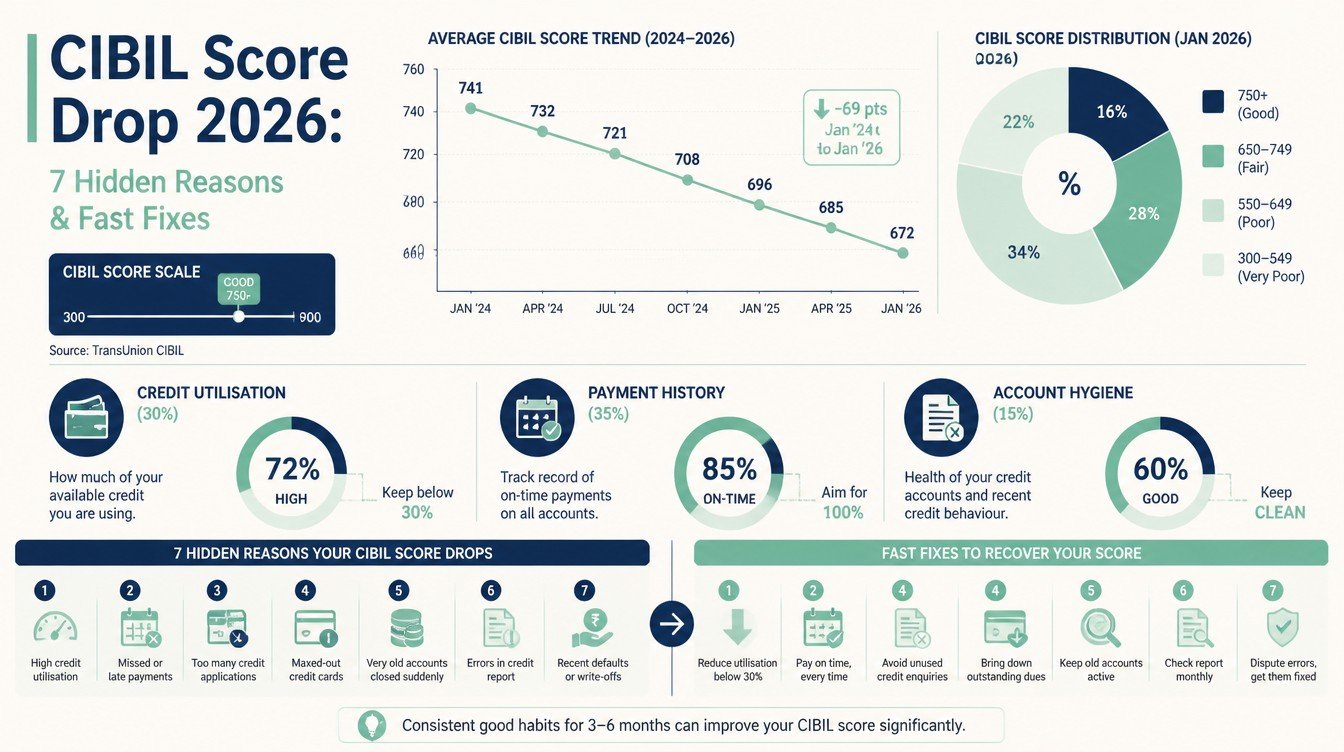

The CIBIL score is a three-digit number between 300 and 900, generated by TransUnion CIBIL using the credit information report (CIR) that banks and lenders submit. A score above 750 is generally treated as healthy by lenders for unsecured credit. A score above 800 unlocks the best spreads on home loans and credit cards.

Roughly five behavioural inputs shape the score: payment history, credit utilisation, credit mix, length of credit history, and the velocity of new credit inquiries. Each input has a different weight, and the score is sensitive to changes in inputs that borrowers rarely think to monitor.

The five inputs at a glance

- Payment history: the single largest contributor, typically around one-third of the score.

- Credit utilisation: the share of your total revolving credit limit currently being used.

- Length of credit history: the average age of all credit lines.

- Credit mix: the blend of secured and unsecured credit.

- New credit inquiries: hard pulls in the recent past, usually six to twelve months.

Why monthly volatility is normal

Even a stable borrower sees the score move by five to fifteen points each cycle. Banks report data once a month at slightly different dates, so a perfectly paid bill may not yet be visible. A statement that closes with a temporarily high balance can pull the score down for a single reporting cycle even if the bill is paid in full the next day.

Where the 90-day rule comes in

Most of the fast fixes in this guide cluster around a 90-day window. Bureau data refreshes monthly, so three reporting cycles give enough room to register the change in utilisation, reduce inquiry density, or close a successful dispute. Quick fixes are real, but they need at least one full quarter to land.

Reason 1: Credit utilisation crept above 30% without you noticing

Utilisation is the most under-recognised score killer for salaried Indians. The bureau looks at the balance on the statement date, not the balance after you pay. A credit card with a Rs. 1,50,000 limit that runs up to Rs. 90,000 across the month and is paid in full each cycle still reports a 60% utilisation on the statement date.

A long-standing guideline in Indian personal finance is to keep utilisation below 30% of the total revolving limit, and ideally closer to 10% for the strongest score impact. The math is simple: a total limit of Rs. 5,00,000 across three cards should typically not show more than Rs. 1,50,000 in balances on any statement date.

One-line fix

Pay a part of the bill before the statement-generation date, not the due date, to push reported utilisation below 30%.

Why this works

Bureaus see the statement balance, not the running balance. A partial pre-statement payment lowers the snapshot they receive and shows up at the next bureau refresh.

The total-limit lever

A request for a credit limit enhancement on an existing card can cut utilisation without changing actual spending. A jump from a Rs. 2,00,000 limit to Rs. 3,00,000 at the same spend lowers utilisation from 50% to 33%, without any change in behaviour.

Reason 2: A closed credit card just aged out your credit history

Closing the oldest credit card in your wallet feels disciplined. The bureau sees it as a shortened credit history and a reduction in total available limit. Both push the score down.

The length-of-credit-history input is built on the average age of all open accounts. Closing a card opened in 2014 in a wallet whose other cards were opened in 2022 collapses the average age. The drop is real, often sharper than borrowers expect.

One-line fix

Keep the oldest credit card open with a small recurring spend, even if it is just one OTT subscription paid in full each month.

Closed loans matter too

A personal loan or auto loan that closes drops off the credit mix and the active history. The score may dip mildly even though the closure is a positive event. The cure is patience and a steady mix of revolving and instalment credit.

What about closing a free card that just became chargeable?

If the card now carries an annual fee, ask the issuer to convert it to a lifetime-free variant or migrate it to a no-fee card with the same vintage retained. Many issuers will do this on request rather than lose a long-tenured customer.

Reason 3: Rate-shopping created a cluster of hard inquiries

Every credit application creates a hard inquiry on your CIBIL report. A flurry of inquiries within sixty days flags the bureau’s algorithm as a potential signal of distress, even if you were simply price-shopping a home loan or a balance transfer.

Five hard inquiries in three months can push a clean 780 score down to 740. The dip usually heals within six to twelve months, but it is a real reason borrowers see scores drop after a season of price comparison.

One-line fix

Cluster all credit applications for the same product within a 14-day window so the bureau can treat them as a single rate-shopping event.

Pre-approved offers and soft pulls

A pre-approved offer from your existing bank is a soft inquiry and does not affect the score. A formal application based on that offer, however, becomes a hard inquiry. Be selective about converting offers into applications.

Aggregator websites and their fine print

Some loan aggregator websites trigger hard pulls from multiple lenders in parallel. Read the disclosure before clicking the final “apply” button. A single comparison click can become five hard inquiries on your report.

Reason 4: A small unpaid amount on an old card you forgot about

A Rs. 350 balance on an old credit card, accidentally left unpaid, is the kind of detail that quietly hollows out a score. Late charges accumulate, interest compounds, and after ninety days the account is reported as a default or written off.

This is one of the most common write-off cases TransUnion CIBIL sees: a small amount on a low-use card that the customer believed was settled. The bureau does not distinguish between Rs. 350 and Rs. 35,000 when classifying a default. The hit to the score is the same.

One-line fix

Download your CIBIL report and reconcile every line item; settle any old dues in writing and request the lender to update the bureau within thirty days.

Why the score does not bounce back immediately

Even after the settlement is reported, the historical late-payment marker remains on the report for up to seven years. The score recovers gradually as fresh on-time payments dilute the old negative.

Settled versus closed

A “settled” tag on a closed account is worse for the score than “closed”. Always negotiate a “closed” or “paid in full” status with the lender when clearing an old default. The wording matters.

Reason 5: A guarantor or co-applicant has missed payments

Acting as a guarantor on a friend’s loan or being a co-applicant on a sibling’s home loan is treated by the bureau as your own credit responsibility. If the primary borrower misses an EMI, the missed payment is reported against you as well.

This is often the most painful reason for a sudden CIBIL drop, because the borrower has done nothing wrong on their own accounts. The damage is real and the recourse is limited.

One-line fix

If you are a guarantor and the primary borrower is unreliable, pay the missed EMI yourself and recover it from them directly to protect your score.

How to avoid the trap

Treat any guarantee as a personal liability that lives on your credit report for the life of the loan. Decline guarantees casually given to friends or distant relatives, especially for unsecured personal loans.

Removing yourself as guarantor

Once a guarantee is given, banks rarely allow it to be withdrawn unless the loan is foreclosed or a fresh guarantor of equivalent profile is substituted. The escape hatches are narrow.

Reason 6: A reporting error or identity mix-up on your CIR

The credit information report is built from data the lenders submit. Lenders make mistakes. A common one is reporting a closed loan as active, an EMI as missed when it was actually paid, or two accounts in your name that you never opened.

Some errors are benign. Others, like an unfamiliar loan account or a wrongly tagged default, can drag the score by a hundred points and signal possible identity fraud.

One-line fix

Raise a dispute on the CIBIL portal within thirty days of spotting the error and attach supporting documents.

What CIBIL must do under the rules

Under the RBI’s framework for credit information companies, the bureau must investigate every dispute within thirty days. If the lender does not respond, the disputed line must be updated to reflect the borrower’s claim.

Common identity errors

Look for variants of your name and date of birth merged with another consumer. PAN-linked KYC has reduced this dramatically, but the legacy data from before universal PAN linkage still produces stray records.

Reason 7: A new loan or card just dropped your average account age

A brand new credit card lowers the average age of credit, even though it adds to the total limit. The score may dip in the month the card is reported and slowly recover over the next two to four quarters as the new account ages.

This is the most counter-intuitive reason for a score drop: a positive event (more credit available, more diversification) producing a temporary negative score move. Understanding it prevents panic.

One-line fix

If you have already opened the new card, hold off on any more new credit for at least six months to let the average age stabilise.

The grouping advantage

When several new accounts open close together (a car loan, a co-branded card, a balance transfer), the average age drops sharply. Spacing major credit decisions by six months each is a quiet but effective discipline.

How long until the score recovers?

For a salaried borrower with a clean payment history, the score typically recovers to the pre-event level within two to three reporting cycles. The recovery is slower if utilisation also creeps up at the same time.

Five free sources for your CIBIL report and credit score

Indian borrowers are entitled to one full CIBIL report each calendar year free of charge under the RBI’s directives. Several channels make that report easy to access, and a handful of additional bureaus and aggregators offer free score views more often than that.

| Source | What you get | Frequency |

|---|---|---|

| CIBIL official website | Full CIR and score, free once per year, with paid premium options for monthly refresh | Once per calendar year free |

| Experian India | Full credit report and score with monthly refresh on the basic plan | Monthly refresh available |

| Equifax India | Credit report and score; one full report each year is free under RBI rules | Annual free; paid for more |

| CRIF High Mark | Credit report and score; one free report each year | Annual free |

| Bank or fintech app (Paytm, PhonePe, Cred, NetBanking dashboards) | Score view sourced from a partner bureau; useful for monitoring | Often monthly |

Why pull from more than one bureau

Lenders do not all report to every bureau in real time. A loan disbursed by one bank may show up at Experian a week before CIBIL or vice versa. Cross-checking across two bureaus is the cheapest fraud-detection tool a salaried Indian has.

What to look for on first read

- Personal details (name, DOB, PAN, address) match yours exactly.

- List of accounts matches your actual loans and cards.

- Account status (active, closed, written off) is correct for each line.

- Recent enquiries are all initiated by you.

- Payment history columns show no surprise late markers.

How to read the inquiry section

The inquiry section lists every hard pull on your report in roughly the last twenty-four months. A pull you do not recognise is a red flag for either identity misuse or a lender adding you to their pre-approval base without consent.

Dispute process step by step

The dispute process is more clinical than borrowers expect. The bureau is the referee, not the rule-maker. The lender that submitted the data has to confirm or correct it. The borrower’s job is to provide enough documentary evidence to make the correction obvious.

The steps below apply to TransUnion CIBIL; Experian, Equifax, and CRIF have similar flows on their own portals.

Step 1: Locate the error

Read your full CIR, not just the headline score. Highlight every line that does not match your own records: account status, last payment date, credit limit, outstanding amount.

Step 2: Gather supporting documents

Pull receipts, bank statements, EMI debit proofs, and any closure or NOC letters from the lender. Screenshots of internet-banking transactions and email confirmations from the lender count as evidence.

Step 3: File the dispute online

Log in to the CIBIL consumer portal and use the online dispute resolution form. Select the specific line you are disputing and provide a brief written reason. Upload all evidence in PDF format.

Step 4: Track the dispute and respond promptly

CIBIL forwards the dispute to the lender, which has thirty days to respond. If the lender requests additional documents, respond within the bureau’s deadline. Save the dispute reference number throughout the case.

Step 5: Confirm the correction

Once the dispute is resolved, pull a fresh CIR within sixty days to confirm the corrected line is reflected and the score has updated. If not, escalate to the lender’s grievance officer and then to the RBI Integrated Ombudsman.

Common mistakes that quietly damage a score in 2026

Some habits look harmless and even prudent on the surface but actively hurt the score. The list below covers the missteps that show up most often in real CIRs.

Paying only the minimum due each month

Minimum due payments avoid a late marker but signal heavy revolving usage. The interest compounds at 36% to 42% per year on the carried balance, and the score stays under pressure as utilisation never drops.

Settling old defaults instead of clearing them

A “settled” tag on a credit card or personal loan often hurts more than a “closed” or “paid in full” tag. Negotiate the wording with the lender before parting with the money.

Frequent gold loan or short-tenure top-ups

Stacking short-tenure secured loans inflates inquiry counts and creates a busy mix of small accounts. Each one is reported individually and the cumulative effect drags the score.

Co-signing for adult children’s first credit card

Add-on cards under a parent’s account are usually fine. Becoming the primary co-applicant on an adult child’s first loan, however, lands the child’s payment behaviour squarely on the parent’s CIR.

Ignoring the score because it was great two years ago

A 2024 score above 800 says nothing about today. Pull the report at least once a year, ideally just before any major credit decision such as a home loan, a balance transfer, or a top-up.

Fast fixes that move the score within 90 days

The 90-day window aligns with three bureau refresh cycles. The most reliable score-lifters in this window are utilisation cuts, dispute resolutions, and inquiry cooling.

Bring utilisation under 30% on every card

Pay down statement balances strategically so that each card’s reported utilisation sits at 30% or below. The score impact often shows up within forty-five to sixty days.

Close the dispute loop on any errors

Any disputable line on the CIR is a free score-recovery opportunity. The thirty-day investigation window plus a one-cycle refresh fits comfortably inside ninety days.

Skip new applications for the full window

No new credit cards, no fresh personal loan, no balance transfer applications for ninety days. Let inquiry counts age and the score breathe.

Set up auto-pay on every EMI and bill

Auto-pay through a high-balance savings account or salary account removes the most common cause of late markers: an overlooked due date. The mandate needs to be live for at least one full cycle to count.

Add a secured credit line if the file is thin

For young salaried borrowers with a short credit history, a credit card secured against a fixed deposit is a low-risk way to build a positive payment track in twelve to twenty-four months.

Advanced moves once the basics are in place

Once utilisation is tamed and the file is clean, a second layer of moves can lift the score from 760 into the 800-plus zone, where the best loan spreads sit.

Diversify the credit mix

A file with only credit cards is thinner than a file with a card, an auto loan, and a small consumer loan. The diversification benefit is real but small, so do not borrow purely to engineer it.

Watch the per-bureau score, not just CIBIL

Some lenders pull Experian or CRIF, not CIBIL. A salaried borrower with a strong CIBIL but weak Experian can be turned down for a personal loan because the lender pulled the weaker file. Keep all four bureaus tracked once a quarter.

Use the spouse’s CIBIL as a household lever

For joint home loans, both applicants’ scores influence the rate. A spouse with a stronger CIBIL can be added as the primary applicant to capture a better spread. Tax planning and EMI sharing need to be modelled alongside this decision.

Avoid maxed-out limits even briefly

A single statement that hits 95% or 100% utilisation can drag the score even if it is paid in full the next month. Heavy spending months (weddings, festivals, travel) deserve a deliberate plan to split spend across multiple cards or use a debit card.

Time large purchases around the statement cycle

Buying a big-ticket appliance just after the statement closes gives almost a full month before the next reporting snapshot, allowing time to repay before utilisation appears high.

How a low CIBIL score actually costs you in rupees

The cost of a low score is rarely visible until a borrower applies for a loan. Then the rate quoted, the spread offered, and the eligibility computed all carry the score as a hidden multiplier.

Home loan spread differential

A borrower with a CIBIL score above 800 may receive a spread of 2.25% over the EBLR. The same lender may quote 3.00% to a borrower with a score in the 700-740 range. On a Rs. 75 lakh, 20-year loan, the difference compounds into several lakh rupees of additional interest over the life of the loan.

Personal loan rate differential

A salaried borrower with a strong 800-plus score may see personal loan rates around 10.5% to 12%. A 720 score can see the same lender quote 16% to 18%. The score, not the salary, often decides the rate.

Credit card rejection costs

A premium card rejection over a low score forces the applicant into entry-level cards with lower limits and weaker rewards. Limits below Rs. 1,00,000 also keep utilisation higher for any given spend, creating a feedback loop.

Insurance premium proxies

Some insurers in 2026 use credit-bureau-style indicators as proxies for risk pricing on motor and health policies. The exact use varies and is not always disclosed, but a thin or damaged file rarely helps.

Renting in metro cities

A handful of premium property managers now ask for a CIBIL printout as part of tenant verification. A weak file occasionally translates into a larger deposit demand or an outright rejection.

FAQ

Why did my CIBIL score drop after I paid off my credit card?

A full pay-off followed by closing the card often shortens the average credit history and reduces the total available limit. Both push the score down temporarily. Keep the card open with a small recurring spend instead.

How long does a dispute take to resolve on CIBIL?

The bureau is required to investigate within thirty days. Once the lender confirms or corrects the data, the change reflects in your CIR at the next refresh, typically within forty-five to sixty days from the start of the dispute.

Does checking my own CIBIL score reduce it?

No. A self-pull is a soft inquiry and does not affect the score. Only lender-initiated hard inquiries (when you apply for credit) can lower it.

Can I improve my CIBIL score from 650 to 750 in 90 days?

A jump of one hundred points in ninety days is unusual but possible if the starting score was depressed by a fixable error or a one-off utilisation spike. For score drops driven by genuine missed payments, recovery typically takes nine to eighteen months of disciplined behaviour.

What if my CIBIL report shows a loan I never took?

Treat it as a possible identity-misuse case. File a dispute with the bureau, file a written complaint with the lender’s branch manager, and consider lodging a police complaint if the amount is material. Freeze your CIBIL alerts and monitor the report monthly until the issue is closed.

Related guides on this topic are coming to learnfinedge.com soon.