The textbook advice on emergency funds is simple: keep three to six months of expenses in a liquid account. The Indian reality is messier. CPI inflation has hovered between roughly 4 and 7 percent recently, per RBI bulletins; healthcare costs have inflated faster than that, and the gig economy has expanded the share of Indian earners with irregular income. The right emergency fund size in India for 2026 is not a single number; it is a sliding scale that depends on household structure, income stability, and the realistic time it would take to find new earnings after a setback.

This guide rebuilds the emergency-fund math for an Indian salaried or gig-earning household in FY 2025-26. It covers how to size the fund for singles, married couples, and single-income families, how the stability of income changes the number, where to park the corpus, and how post-tax returns compare across savings accounts, sweep-in fixed deposits, and liquid mutual funds. It is a planning framework, not personalized investment advice; SEBI-registered advisers remain the right channel for individual portfolios.

What an Emergency Fund Is and Why the Indian Context Matters

An emergency fund is a dedicated pool of money set aside to cover essential household expenses when income stops or a large unplanned cost arrives. It is neither an investment account nor the same as a contingency reserve for predictable lumpy expenses like insurance renewals. The defining feature is liquidity at short notice with minimal loss of principal.

The Indian context shapes the answer differently from a U.S. or U.K. household for three reasons: faster inflation, less social insurance, and a labor market where a job loss can take 90 to 180 days to convert into a new role of similar pay. Each of these widens the band of “how much is enough.”

The three jobs of an emergency fund

The fund handles three categories of shock: income shocks like a job loss, business downturn, or extended health-driven leave; large expense shocks like a major medical event above insurance limits, a sudden home repair, or a family emergency requiring travel; and policy or market shocks like a sudden tax demand or a delayed bonus. A single pool with the same liquidity profile handles all three.

What an emergency fund is not

The fund is not a vacation account, a wedding fund, or a home down-payment corpus. Mixing those goals with the emergency fund defeats its purpose because the corpus is drawn down on planned expenses and is not available when an actual emergency hits. Goal-based investing keeps each pool separate.

Why India needs a slightly larger buffer

Indian households face a higher real-cost shock from health emergencies because out-of-pocket healthcare spending remains substantial despite the rise of health insurance. The fund has to absorb co-payments, sub-limits, room rent caps, and any procedure that falls outside the insurance scope. The international 3-month rule often understates what the Indian household actually needs.

The Base Question: What Counts as “Essential Expenses”

The emergency-fund target is a multiple of essential monthly expenses, not of in-hand income. Most households mis-size because they use the wrong base. The essential-expenses base strips out the wants bucket entirely.

The essential-expense floor for a household

Essential expenses include rent or home loan EMI, groceries, utilities, school fees for currently enrolled children, transport to work, mobile and broadband, term life and health insurance premiums, and the contractual minimum on any other EMI. Discretionary spending like dining out, OTT subscriptions, holidays, and shopping is excluded.

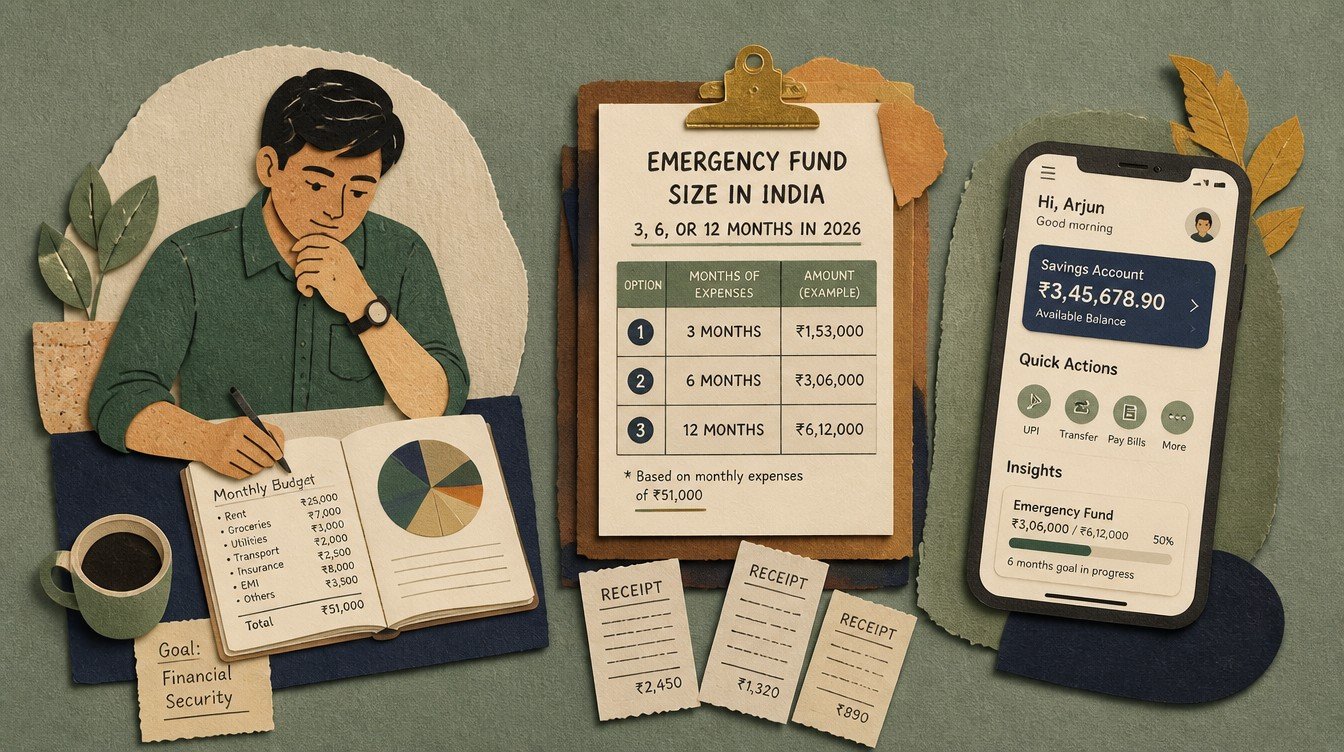

A sample essential-expense computation

For a salaried earner who takes home Rs.100,000 each month, the typical base for essential expenses is closer to Rs.55,000 to Rs.70,000, rather than the full Rs.100,000. The emergency fund sizes are based on this Rs. 55,000 to Rs. 70,000 base, not on take-home pay. Using take-home as the base inflates the target unnecessarily and pulls capital away from long-term investments.

How to handle EMIs in the base

The contractual minimum EMI on home loans, car loans, and other secured debt sits inside essential expenses because non-payment carries severe consequences. Credit-card minimum payments do too. Any voluntary prepayment above the contractual minimum is not part of essential expenses; it is a savings choice that can pause during a crisis.

How to handle insurance premiums

Insurance premiums paid annually should be divided by twelve and included in the monthly essential base. Treating insurance premiums as a once-a-year lump sum is one of the most common sizing errors, especially since the renewal can occur during the crisis itself.

The 3-6-12 Sizing Matrix by Household Type

The textbook advice of 3 to 6 months is best understood as a range that resolves into a specific number once household type and income stability are layered in. The matrix below applies for FY 2025-26.

| Household type | Income stability | Recommended size (months of essential expenses) |

|---|---|---|

| Single, no dependents | Stable salaried, large employer | 3 to 4 months |

| Single, no dependents | Gig, freelance, or variable | 6 to 9 months |

| Married, dual income | Both stable salaried | 3 to 5 months of combined essentials |

| Married, dual income | Mixed (one salaried, one variable) | 5 to 7 months of combined essentials |

| Married, single income, dependents | Stable salaried | 6 to 9 months |

| Married, single income, dependents | Variable / business | 9 to 12 months |

| Pre-retiree / retiree | Mixed pension and capital gains | 12 months or higher |

Single, no dependents

The lowest sizing applies because the household has the most flexibility: lower fixed costs, willingness to move to a smaller flat, and the ability to take temporary lower-paying work. Three to four months of essential expenses is generally enough for stable salaried earners. Gig workers in this category bump up to six to nine months because the income variance is higher even without dependents.

Married, dual-income household

The risk of both incomes stopping at the same time is lower than for a single-income household, which is why the recommended buffer is at the lower end of the range. The combined essential expense base is used. If one spouse is salaried and the other has variable income, the buffer creeps up to absorb that volatility.

Single-income family with dependents

This is the highest-risk profile in the matrix. A single source of income covers school fees, family insurance, and dependent care. A 6 to 9 month buffer is the floor; for variable-income earners in this category, 9 to 12 months is more defensible.

Pre-retirees and retirees

Retired households need a larger emergency reserve because the path back to employed income is narrow if a corpus drawdown hits unexpectedly. Twelve months of essential expenses, often parked separately from the investment corpus, is a common practice.

Stable Salaried vs Gig Worker: Why the Number Differs

Income stability is the single biggest factor in sizing an emergency fund. The same household with the same expenses but different income profiles arrives at very different target corpora.

The salaried stability premium

A stable salaried earner at a large employer benefits from notice periods (typically 30 to 90 days), severance norms (often one to three months of salary for tenured employees), and the predictability of monthly credits. Job loss is not zero-day; the employer typically offers a notice period during which job hunting can begin. This arrangement effectively reduces the period the emergency fund needs to cover.

The gig and freelance discount on stability

Gig workers, consultants, and freelancers face a different shock profile. There is no notice period; a contract ends on its scheduled date or earlier if either party invokes a termination clause. Receivables can run 30, 60, or 90 days behind invoicing, which lengthens the cash-flow gap before the next inflow. The buffer compensates for both the variance and the receivable lag.

The business-owner profile

Owner-operated businesses sit at the higher end of the buffer spectrum because expenses can persist even when revenue stops, and personal cash flow is intertwined with business cash flow. Many financial planners recommend separating personal emergency funds from business operating reserves, with the personal fund sized at 9 to 12 months of essential personal expenses.

What government-sector stability looks like

Government-sector salaried earners often carry the highest job stability and predictable annual pay scales. Even so, a three-month buffer is the minimum because medical and family-emergency shocks remain real regardless of job stability. The lower end of the matrix applies, not zero.

Where to Park the Emergency Fund

An emergency fund earning 2.5 percent in a savings account is losing value to inflation each year. A fund parked entirely in equity is too volatile to fund essential expenses on short notice. The right answer is a layered allocation across three instrument types.

Savings account: the first layer

The first one to two months of essential expenses should be kept in the salary or family savings account that the household already uses. Returns are modest, typically 2.5 to 4 percent gross depending on the bank, but access is instantaneous. The cost of that liquidity is the low yield; the benefit is zero friction at the moment a real emergency hits.

Sweep-in fixed deposit: the middle layer

The next two to three months can sit in a sweep-in fixed deposit linked to the savings account. Most major Indian banks offer this product under names like Auto Sweep or MoneyMaxx. Balances above a threshold automatically convert into FDs at the prevailing FD rate, and a withdrawal request then breaks the FD without any manual intervention. A sweep-in FD is essentially a savings account that quietly earns FD rates on idle balances.

Liquid mutual fund: the third layer

The remaining months can sit in a liquid mutual fund. These are debt mutual funds investing in instruments with residual maturity up to 91 days under SEBI regulations, and they typically offer T+1 redemption. Returns are usually higher than savings accounts and broadly comparable to FDs over a rolling year, with the standard caveat that debt mutual funds carry credit and interest-rate risk and that past performance is not indicative of future results.

What not to use for the emergency fund

Equity mutual funds, stocks, real estate, and gold are inappropriate for the emergency fund. Equity is too volatile, real estate is too illiquid, and gold can move adversely against the rupee at the exact moment you need funds. The Public Provident Fund (PPF) has a 15-year lock-in with partial withdrawal only after the seventh year; the National Pension System (NPS) restricts withdrawals before age 60. Neither qualifies as an emergency fund.

Post-Tax Returns Comparison: FY 2025-26

Each parking option has a different tax treatment, which changes the effective return. The comparison below uses illustrative ranges for the financial year, not guaranteed numbers.

| Instrument | Indicative gross return | Tax treatment | Effective post-tax return (30% slab) | Access time |

|---|---|---|---|---|

| Savings account | 2.5% to 4% | Interest taxable at slab; first Rs.10,000 exempt under 80TTA (old regime only) | Approximately 1.7% to 2.8% | Instant |

| Sweep-in FD (savings + auto FD) | 5% to 7% | Interest taxable at slab; TDS above Rs.40,000 (Rs.50,000 for seniors) | Approximately 3.5% to 4.9% | Same day to T+1 |

| Liquid mutual fund | 5% to 7% | Capital gains taxed at slab rate per current debt-fund taxation rules | Approximately 3.5% to 4.9% | T+1 redemption |

| Short-duration debt fund | 5.5% to 8% | Capital gains at slab rate | Approximately 3.9% to 5.6% | T+1 to T+3 redemption |

The post-tax math worth memorising

For a taxpayer in the 30 percent slab, every gross 1 percent of yield translates to roughly 0.7 percent of post-tax return. The difference between savings (around 3 percent gross) and a sweep-in FD or liquid fund (around 6 percent gross) is about 2 percentage points of post-tax yield. On a Rs.500,000 emergency fund, that is roughly Rs.10,000 per year of difference, which is meaningful but not transformative.

Why chasing yield can be counterproductive

The emergency fund’s job is to be available on demand, not to maximize returns. Stretching for an extra 1 to 1.5 percent by moving into longer-duration debt funds or credit-risk funds increases the chance of a NAV drawdown at the exact moment funds are needed. The yield difference is rarely worth the access risk.

Taxation changes worth tracking

Debt mutual fund taxation has tightened materially in recent budgets, with indexation benefits revised and gains now generally taxed at slab rates regardless of holding period. The Income Tax Department portal and the latest Finance Act remain the authoritative references; figures move year to year, and any sizing decision should be refreshed against the prevailing rules at the time.

The Recommended Three-Bucket Allocation

A clean default allocation for the emergency fund across the three layers reflects both the need for instant access and the desire to keep the corpus growing at least at the pace of inflation.

The 30-30-40 split

A simple default is 30 percent in savings, 30 percent in sweep-in FD, and 40 percent in liquid mutual funds. For a six-month essential-expense fund of Rs.300,000, this is Rs.90,000 in savings, Rs.90,000 in a sweep-in FD, and Rs.120,000 in a liquid fund. The savings layer covers the first two weeks; the sweep-in covers the next four to six weeks; the liquid fund covers the remaining four to five months.

Adjusting the split for risk tolerance

Households more concerned about liquidity at any cost can shift to 50-30-20, keeping more in savings and less in liquid funds. Households that are more comfortable with T+1 redemption can shift the other way, with as much as 20-20-60. The exact split matters less than the principle of layering.

The single-account variant

For modest emergency funds (say under Rs.50,000), a single sweep-in FD account at the primary bank is often simpler than spreading across three instruments. The added return of a liquid fund is small in rupee terms at that scale, and operational complexity is a real cost.

The auto-refill discipline

When a household draws from the emergency fund, the corpus has to be replenished before any new long-term investment resumes. A clean rule is to suspend all incremental investments (SIPs, voluntary EPF, and additional PPF) until the corpus is restored to the target. This is the most important habit attached to the fund and the one most commonly skipped.

How Inflation Changes the Sizing Over Time

An emergency fund sized once and forgotten erodes against inflation. A Rs.300,000 fund built three years ago at then-current expense levels may now cover only four months instead of the original six, as expenses have risen but the corpus has not kept pace.

The annual review trigger

The simplest defense is an annual review, ideally aligned with the household’s other yearly financial reviews (insurance renewals, ITR filing in July, year-end tax planning). At the review, recompute essential monthly expenses, multiply by the target multiple, and compare against the actual corpus.

Topping up versus rebuilding

If the corpus has fallen behind by 10 to 15 percent, a single lump from a year-end bonus is usually enough to restore it. If it has fallen behind by more, a structured monthly top-up over three to six months keeps the budget from getting strained.

Healthcare inflation and the medical sub-fund

Healthcare costs in India have risen faster than headline CPI, according to industry estimates, and IRDAI consumer-education content highlights the growing importance of comprehensive health cover and super top-ups. Some households carve out a separate Rs.50,000 to Rs.100,000 medical sub-fund inside the emergency corpus to absorb deductibles, room-rent caps, and pre-authorization gaps. The sub-fund sits inside the same liquid pool, just earmarked.

What to do if income rises faster than expenses

When income jumps materially (e.g., promotion, new role, spouse going back to work), expenses often do not rise in proportion immediately. The window between an income increase and lifestyle inflation is a natural opportunity to top up the emergency fund first before scaling up discretionary spending.

Common Emergency Fund Mistakes

Most emergency-fund failures in the Indian context trace back to one of a small set of recurring errors. The list below is the working catalogue.

Mixing the emergency fund with goal funds

Combining the emergency fund with the holiday fund or the down-payment fund means the corpus is drawn down on planned expenses. The first defense is a separate savings account, a separate FD, and a separate liquid fund folio, so the boundary is operationally enforced and not just mental.

Parking the fund in equity or long-duration debt

Equity mutual funds and long-duration debt funds (gilt funds and dynamic bond funds) are not emergency-fund instruments. They can drop 5 to 25 percent in a single bad month. The drop is not the problem; the drop at the moment of withdrawal is the problem. Sticking to savings, sweep-in FDs, and liquid mutual funds is the structural defense.

Treating credit cards as the backup

A common (and dangerous) substitute for an emergency fund is a high credit-card limit. Credit-card interest in India typically runs in the 30 to 42 percent annualized range, according to RBI data on consumer credit pricing, making funded emergencies far pricier in the long run. The card is a bridge, not a substitute.

Not replenishing after withdrawal

The corpus is for use; using it is not the problem. Failing to replenish is the problem. A Rs.50,000 medical bill paid from the emergency fund creates an obligation to restore the corpus over the next two to three months. Skipping that step leaves the household exposed when the next emergency arrives.

Sizing against in-hand pay instead of essential expenses

Using take-home pay as the multiplier inflates the corpus target by 20 to 40 percent because it includes wants and savings contributions that are paused during a crisis. The clean base consists only of essential expenses.

Step-by-Step Plan to Build a Six-Month Fund

The hardest part of an emergency fund is not the math; it is the time it takes to accumulate the first three to six months of expenses. A staged plan makes the goal achievable over twelve to eighteen months.

The phased build

- Compute essential monthly expenses for the household. Use bank statement data from the past three months and tag every expense as essential or discretionary.

- Set the target multiple from the sizing matrix above.

- Set an interim milestone at one month of essential expenses, parked in the salary savings account. This is the absolute floor that should be in place within 60 to 90 days.

- Build to three months over the next six months. Park the second and third months in a sweep-in FD or a short-term FD.

- Build to six months over the following twelve months. The additional three months can sit in a liquid mutual fund for slightly better post-tax yield.

- Recalibrate annually against updated essential expenses.

Funding the build without crashing the budget

The simplest source of funding is to redirect the next pay raise entirely into the emergency fund for six to twelve months. The lifestyle does not change, the corpus grows, and the discipline gets installed. Annual bonus and tax refunds are the second-best sources.

Pausing other investments during the build

Households with no emergency fund and active equity SIPs should temporarily pause their SIPs until they have saved at least one month’s worth of essential expenses. The math of saving with a credit-card balance carrying 36 percent interest while investing at 12 percent expected equity returns is rarely in the household’s favor.

Special Situations: Single Parents, Joint Families, and Couples Planning a Child

Standard templates do not capture every household structure. This section provides a brief overview of three common household configurations in India.

Single parents

Single parents face the highest sizing requirement in the matrix because there is no second adult to absorb a shock. Twelve months of essential expenses is the defensible floor, supplemented by comprehensive term life insurance (with the child as beneficiary or through a trust) and family health insurance.

Joint families with shared expenses

In joint-family structures, multiple earners contribute to shared expenses, which reduces the individual sizing requirement modestly. The cleanest setup is one shared emergency fund based on shared essential expenses, plus a smaller individual fund for personal essentials, such as individual insurance premiums.

Couples planning a child

Couples planning to add a child in the next 12 to 24 months should pre-size the emergency fund for the expanded family. Maternity costs, paternity leave, and the first year of dependent care can add 30 to 50 percent to essential expenses. Building the new fund target before the child arrives is materially easier than building it after.

The Emergency Fund and the Rest of the Portfolio

The emergency fund interacts with the rest of the household’s financial portfolio in three specific ways. Each affects how much equity exposure and how much insurance the household carries.

The fund enables higher equity allocation elsewhere

A household with a robust emergency fund can credibly run a higher equity allocation in the long-term portfolio because the equity portion does not have to double as a liquidity reserve. SEBI-registered investment advisers commonly note that without an emergency fund, the long-term portfolio is forced to stay more conservative than the household’s actual time horizon would justify.

The fund reduces reliance on credit

A household with six months of essential expenses parked liquidly is far less likely to draw down a credit card, take a personal loan, or break long-term investments at unfavorable times. The shadow benefit is improved credit behavior and a lower lifetime interest cost.

The fund interacts with the insurance stack

Comprehensive health insurance reduces the size of the medical sub-fund that the household needs to maintain. Term life insurance protects the income side, which reduces the duration of income shocks the fund has to absorb. The two work together: better insurance lets the emergency fund be smaller; a larger emergency fund lets the household tolerate higher deductibles on insurance.

When the fund should grow beyond 12 months

For very specific profiles, the fund can credibly grow beyond 12 months: pre-retirees within three years of stopping work, business owners going through a major capital cycle, families with a member receiving long-duration medical treatment, and households planning a deliberate career break. Beyond 12 months, the marginal yield drag compared to the long-term portfolio becomes significant, so the fund size should be justified by a specific need rather than being set by default.

FAQ

Should an emergency fund be in the same bank as the salary account?

A common practice is to use the salary bank for the first one to two months of the fund (for instant access) and to spread the rest across at least one other bank or a mutual fund platform. The spread protects against a single-institution issue (frozen account, system outage, or fraud) at the moment funds are needed, and most banks now offer sweep-in FDs that retain the operational convenience.

Does the emergency fund count toward the household’s net worth?

Technically yes, but mentally it should not. The fund is committed capital, not investable capital. Including it in net worth calculations can create a false sense of investment progress. Some financial planners maintain a separate “reserves” line in household balance sheets so the long-term investment progress is visible without the emergency fund inflating the picture.

Is a credit-card limit a substitute for an emergency fund?

It is not. Credit card balances carry interest in the 30 to 42 percent annualized range, according to RBI data on consumer credit pricing, and that compounds quickly during the very period when an emergency has reduced income. A credit card can act as a 30-day bridge until the emergency fund is mobilized, but it should not be the primary backup. The fund provides time; the card does not.

Should HRA-eligible employees count rent in essential expenses?

Yes. Rent is essential regardless of the HRA tax shield. The HRA exemption reduces the effective tax cost of rent for old-regime taxpayers, but it does not change the monthly cash outflow that the emergency fund must be able to cover. The sizing base is the gross rent paid, not rent minus the tax saving.

How quickly can a typical Indian household actually access liquid mutual fund money in a crisis?

Liquid mutual funds typically settle on T+1 (next business day) for redemption requests placed before the cut-off, per SEBI norms. Many AMCs offer instant-access facilities up to Rs.50,000 or 90 percent of folio value, whichever is lower, with proceeds in the bank within minutes via UPI or IMPS. The combined effect is that the liquid-fund layer is operationally as fast as a sweep-in FD for the first slice and within 24 hours for the rest.

Related guides on this topic are coming to learnfinedge.com soon.

Related Articles