SIP vs Lumpsum: What Rs 10,000 Looks Like After 20 Years in Each

The SIP vs lumpsum question has become a near-monthly debate in Indian personal finance circles, especially with SIP inflows now consistently crossing Rs 26,000 crore per month and equity markets at levels that make every lumpsum buyer second-guess the entry. The intuitive answer is that SIP smooths the entry and lump sum maximises time in the market, but the actual rupee outcome depends on the path of returns, the timing of contributions, and the maths of rupee-cost averaging in a way that is worth working out properly with real Indian data.

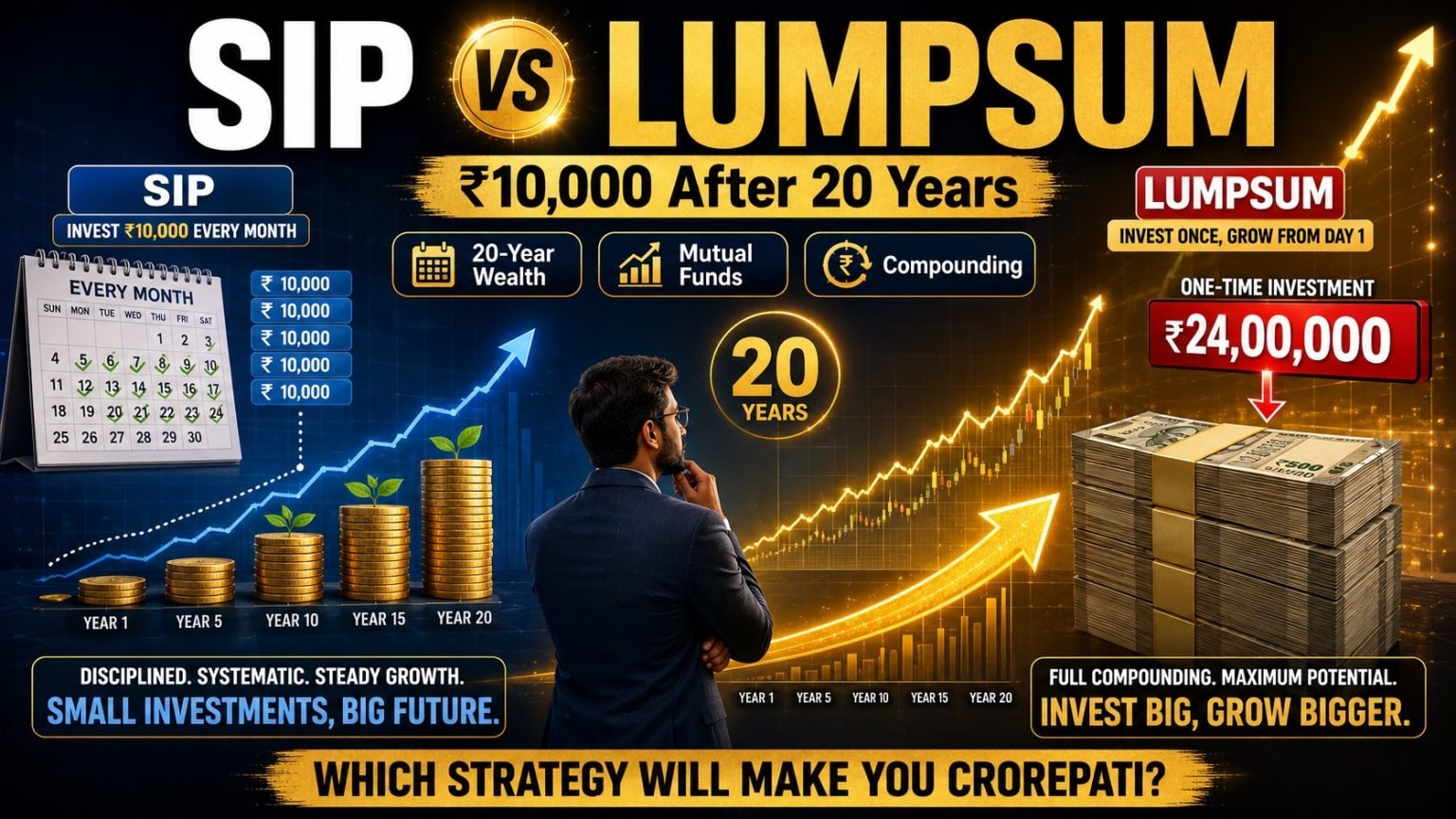

This guide runs a backtest of an Rs 10,000 per month SIP versus a Rs 24 lakh lump sum (matched total contribution) over a 20-year window on Nifty 50 TRI data, explains the rupee-cost averaging math from first principles, shows when a lump sum beats an SIP and when an SIP beats a lump sum, and explains why a systematic transfer plan often outperforms both. The point is to let an investor decide, with full information, whether the next Rs 5 lakh or Rs 50 lakh of investable cash should be deployed at once or over time.

The Maths of Rupee-Cost Averaging

A systematic investment plan deploys a fixed rupee amount every month into a mutual fund, buying a varying number of units depending on the NAV at that month’s purchase. When the NAV is low, the same rupee buys more units. A high NAV means that the same rupee buys fewer units. Over a long enough period, the average cost per unit ends up below the simple average of the NAVs, which is the mathematical edge of rupee-cost averaging.

A lump-sum investment deploys the full amount on a single day and rides the NAV from that point forward. There is no averaging effect because there is only one entry NAV. The total return is determined entirely by the entry NAV, the exit NAV, and the path of dividends or distributions in between.

Why the SIP advantage is path-dependent

The cleanest way to see the SIP advantage is to consider two extreme paths. In a strictly rising market where the NAV climbs every month, the lumpsum wins because every later SIP purchase is at a higher price than the lumpsum’s single entry. In a strictly falling market followed by a recovery to the starting level, the SIP wins because the later purchases buy more units at lower prices, and the recovery lifts more units than the lumpsum’s fixed-unit position.

Real Indian markets do not run cleanly on either path. They oscillate, with drawdowns of 20 to 50 percent interspersed with strong recovery and trend phases. The 20-year rupee-cost averaging math in Indian markets has historically produced a small but real edge for the SIP in some windows and a small but real edge for the lump sum in others, depending entirely on whether the early years contained a meaningful drawdown.

Backtest: Rs 10,000 SIP vs Rs 24 Lakh Lumpsum on Nifty 50 TRI

The matched comparison is to deploy Rs 10,000 per month for 20 years, which sums to Rs 2.4 million in total contributions, against a single lump sum of Rs 2.4 million on the first day of the SIP. The historical Nifty 50 TRI (Total Return Index) data from January 2006 to December 2025 provides a rolling 20-year window suitable for this exercise.

Over the full 20-year window starting January 2006, Nifty 50 TRI delivered a CAGR of approximately 13 percent. A Rs 24 lakh lump sum on day one of this window grew to approximately Rs 27.5 crore by December 2025. The Rs 10,000 monthly SIP across the same window contributed the same Rs 24 lakh total and accumulated to approximately Rs 1.05 crore, with an IRR of approximately 13.5 percent.

Why the lump sum dollar outcome is larger

The lump sum gets the full Rs 24 lakh compounding for the entire 20 years, while the SIP only has the first month’s Rs 10,000 compounding for the full 20 years and the final month’s Rs 10,000 compounding for one month. The total rupee exposure to the market, measured in money-weighted time, is meaningfully larger for the lump sum. The IRR for the SIP is actually slightly higher because the SIP captured better averaging through the 2008 drawdown, but the dollar outcome is naturally smaller, as the average money-in-market duration is half that of the lump sum.

The 2008 entry window

A more instructive backtest is to deploy the lump sum at the absolute top of January 2008 against an SIP that starts in the same month. The lump sum sat at a 60 percent drawdown by March 2009 and took until late 2010 to recover. The SIP, in contrast, accumulated cheap units throughout 2008 and 2009 and emerged from the recovery with a substantially larger unit count for the same average cost. By 2025, the SIP outcome was approximately 12 to 15 percent higher than the lump sum starting at the 2008 top, despite the lump sum’s longer compounding window.

This scenario is the structural case for SIPs: they protect the investor from poor entry timing. The protection has a measurable cost in markets that trend up cleanly, but it has substantial upside in markets that draw down before they trend.

When someone wins

A lump sum wins decisively in three scenarios. The first is when the entry happens immediately after a substantial drawdown, when prices are already depressed and the recovery delivers the bulk of the return in the first few years. The second is when the entry happens early in a long secular uptrend, when every subsequent year’s NAV is higher than the previous and there is no opportunity for rupee cost averaging to reduce the average cost.

The third scenario is when the lump sum is large enough that the alternative is to leave the cash in a low-yielding instrument while the SIP plays out. A Rs 1 crore inheritance held in a savings account at 3 percent incurs a substantial opportunity cost on the residual cash that is not yet deployed while a Rs 1 lakh monthly SIP plays out over eight years.

The behavioural problem with lump sums

The mathematical case, which is genuinely mixed, does not explain why most retail investors receive advice to choose SIPs rather than lumpsums. The reason is the behavioural case. An investor who deploys a lump sum on day one and watches a 30 percent drawdown is far more likely to capitulate at the bottom than an investor who is steadily SIPing through the drawdown. Research shows that investor behaviour, not market timing, is the single largest determinant of long-term returns.

When SIP Wins

SIP wins decisively in volatile markets that include meaningful drawdowns in the early years of the investment window. SIP also wins in flat markets where the average cost matters more than the entry timing. SIP is better for any investor who has not previously held a substantial equity allocation through a deep drawdown, because the SIP cadence builds the psychological capital needed to stay invested.

SIP also wins for investors who do not have a lump sum to begin with. For a salaried professional building wealth from monthly income, the SIP is not a strategy choice; it is the natural cadence of how the money becomes available. The SIP-vs-lump sum question only arises when there is a meaningful pool of cash already accumulated, such as from a bonus, an exit, or an inheritance.

The Systematic Transfer Plan Hybrid

A Systematic Transfer Plan (STP) deploys a lump sum into a liquid or ultra-short debt fund and transfers a fixed amount each month into an equity fund. The lump sum earns debt-fund yield (typically 6 to 7 percent) while waiting to be deployed, and the rupee-cost averaging effect is captured on the equity side.

For an investor with a Rs 24 lakh lump sum, an STP across 24 months deploying Rs 1 lakh per month into an equity fund typically outperforms both the pure lump sum and the pure SIP in markets with meaningful interim drawdowns. The reason is that the residual cash continues to earn debt yield rather than sitting in a savings account, and the equity exposure builds gradually with the rupee-cost averaging benefit.

How to size the STP duration

A 12-month STP is appropriate when the equity markets are at neutral valuations and there is no specific reason to expect a drawdown. When valuations are stretched, an investor may want to extend the averaging window with a 24-month STP. Beyond 24 months, the residual cash drag becomes meaningful enough that the STP loses much of its advantage over a SIP funded by fresh income.

The tax treatment of STP transfers

Each STP transfer from the debt fund to the equity fund is technically a redemption from the debt fund, which triggers tax on the accumulated gains in the debt unit. With debt funds losing the indexation benefit in 2023, the gain on the debt fund is now taxed at the investor’s slab rate as a short-term capital gain (since most STPs run for less than 36 months). The tax drag on the debt side is real and should be incorporated into the STP-vs-lumpsum comparison.

Common Mistakes Investors Make on the SIP vs Lumpsum Question

The first mistake is to treat the lump sum as inherently riskier than the SIP. The risk is identical at the end of the holding period; only the path of returns differs. An investor who deploys a Rs 24 lakh lump sum and an investor who SIPs Rs 10,000 monthly are both fully invested in equity by year 20, and their portfolios are equally exposed to whatever drawdown the market produces in year 20.

The second mistake is to pause SIPs during drawdowns. The entire mathematical advantage of the SIP comes from buying more units when prices are low. An investor who panics and pauses their SIP at the bottom is converting the SIP into a poorly timed lump sum that has already been deployed during the falling phase. The discipline to continue the SIP through the drawdown is what produces the IRR advantage.

The third mistake is to chase the maximum-return version of the wrong question. The right question is not “Which option gives the highest expected return?” But, “Which option lets me stay invested for the full 20 years without capitulating?” Industry experts agree that behaviour, not math, overwhelmingly drives the difference between the highest-expected-return strategy and the highest-actually-realised-return strategy for retail investors.

Step-by-step decision framework

- Identify whether the investable amount is a lump sum (one-time) or fresh income (monthly).

- If it’s fresh income, the SIP is the only option. The question collapses.

- If lump sum, assess current equity valuations against long-term averages.

- If valuations are neutral or low, deploy a lump sum or use a short STP of 6 to 12 months.

- If valuations are stretched, use an STP of 12 to 24 months.

- If valuations are at extreme highs, hold the lump sum in debt for longer and let a slower STP play out.

- In all cases, continue any existing SIP from fresh income alongside the STP or lump-sum decision.

- Please review the deployment annually and adjust it based on actual market conditions rather than predictions.

SIP, Lumpsum, and STP Compared

| Parameter | SIP | Lumpsum | STP |

|---|---|---|---|

| Initial deployment | Small monthly amount | Full amount on day one | Full amount in debt, transferred monthly to equity |

| Source of funds | Fresh income | Existing pool of cash | Existing pool of cash |

| Rupee-cost averaging | Yes | No | Yes (on equity side) |

| Idle cash drag | None | None | Earning debt yield |

| Time in market | Builds gradually | Full from day one | Builds over STP period |

| Best for | Salaried investors | Stable markets, low valuations | Stretched valuations |

| Behavioural protection | High | Low | Medium |

| Tax efficiency | Equity LTCG only | Equity LTCG only | Debt slab tax on each transfer |

Advanced Strategy: Combining SIP, Lumpsum, and Tactical Top-Ups

An investor with both fresh income and an occasional lump sum (year-end bonus, equity vest, and real estate exit) can run a layered structure. The fresh income drives a permanent monthly SIP at a level that fits the household budget. The annual bonus is deployed either as a lump sum at the time of receipt if valuations are neutral or as an STP if valuations are stretched. A tactical top-up SIP is added during significant drawdowns to accelerate the unit accumulation when prices are below long-term averages.

The layered structure captures the behavioural discipline of the SIP for the permanent allocation, the time-in-market benefit of the lump sum for the bonus, and the contrarian unit accumulation of the tactical top-up. Over a 20-year window, this structure has historically delivered IRRs 1 to 2 percentage points above a pure-SIP strategy, with most of the outperformance coming from the tactical top-up component during drawdowns.

Pairing this with regime and goal-based planning

The investor’s choice between SIP and lump sum is regime-neutral on the income tax side. Equity LTCG and STCG rates apply identically in the new and old regimes, and the choice between tax regimes for FY 2026-27 does not change the SIP-vs-lumpsum math. The decision is a pure mutual-fund cadence question, separate from the broader tax planning conversation.

Common Mistakes During the 20-Year Holding Period

The most common mistake is to chase fund performance and switch out of the chosen fund during a period of relative underperformance. Equity funds go through 3- to 5-year cycles of relative under- and outperformance. Switching at the wrong moment in the cycle locks in the underperformance and starts the new fund just as its cycle is about to reverse. Sticking with a well-chosen fund through the full 20 years is structurally challenging but mathematically beneficial.

The second mistake is to redeem partially for non-emergency needs. A 20-year SIP that is partially redeemed for a car, a renovation, or a wedding loses far more than the redeemed amount because the redeemed portion would have compounded for the remaining years. Ring-fencing the long-term SIP from short-term consumption is the discipline that converts theoretical returns into actual wealth.

The third mistake is failing to step up the SIP amount over time. A ₹10,000 SIP in 2006 represented a meaningful slice of monthly household income. By 2026, the same Rs 10,000 represents a much smaller slice due to wage inflation. Stepping up the SIP annually by 8 to 10 percent keeps the savings rate constant in real terms and substantially improves the eventual corpus.

Frequently Asked Questions

Should I pause my SIP if the market falls 30 percent?

No. A 30 percent drawdown is precisely the environment in which the SIP delivers its rupee-cost averaging benefit. Pausing the SIP at the bottom converts a disciplined accumulation strategy into a poorly timed sale of future opportunity. The right behaviour is to continue the SIP and, if cash flow permits, add a small top-up to accelerate the unit accumulation while prices are depressed.

Is it better to SIP into one fund or to split it across multiple funds?

For a SIP amount under Rs 25,000 per month, a single well-chosen large-cap or flexi-cap fund is usually sufficient and avoids unnecessary complexity. Above Rs 25,000, splitting across two or three funds (typically a large-cap, a flexi-cap, and a mid-cap) provides modest diversification benefits without diluting the focus. More than three funds in a SIP portfolio tend to underperform a simpler structure due to overlap and effort drag.

Can I run a SIP and a lump sum simultaneously in the same fund?

Yes, and this practice is operationally common. The SIP and the lump sum are tracked as separate transaction streams within the same folio but contribute to the same total holding. There is no tax disadvantage or operational penalty. The combined position is treated as a single holding for capital gains computation under the FIFO rule.

How much should my monthly SIP be with a Rs 1 lakh monthly salary?

A reasonable starting point is to target a savings rate of 25 to 30 percent of gross income, of which 60 to 70 percent should flow into equity SIPs and the balance into debt, gold, or emergency funds. For a Rs 1 lakh monthly salary, this figure implies an equity SIP in the range of Rs 18,000 to Rs 22,000 per month, stepped up annually with salary growth. The exact split depends on age, dependants, and other goals.

Does the SIP returns calculation include the LTCG tax?

The advertised SIP returns and IRR are pre-tax. The actual post-tax return for the investor is reduced by the equity LTCG of 12.5 percent on gains above Rs 1.25 lakh per year, which, for a Rs 1 crore corpus at exit, is a real but moderate drag. The pre-tax IRR of 13 percent typically translates to a post-tax IRR closer to 11.5 to 12 percent for a 20-year SIP, which is still highly competitive with any alternative asset class in India.

Related Articles

- Crypto Tax India: 30% Rule and Schedule VDA

- REIT Investment India: Complete Guide

- NPS Vatsalya Scheme: Complete Guide for Parents