Standard Deduction New Tax Regime: Rs 75,000 Explained for Salaried Employees

The standard deduction new tax regime was enhanced to Rs 75,000 in Budget 2024, up from Rs 50,000 in the old regime. This change significantly improved the attractiveness of the new tax regime for salaried employees. Understanding exactly how this deduction works, who gets it, and how it compares to the old regime’s deduction is essential for making the right tax regime choice. This guide covers all aspects of the standard deduction in both regimes.

What Is the Standard Deduction?

The standard deduction is a flat deduction from salary income available to all salaried employees and pensioners. It requires no documentation, no investment, and no proof – it is automatically applied to your gross salary before tax calculation. The deduction was reintroduced in the Indian income tax system in Budget 2018 (it existed earlier, was removed in 2005, and was brought back).

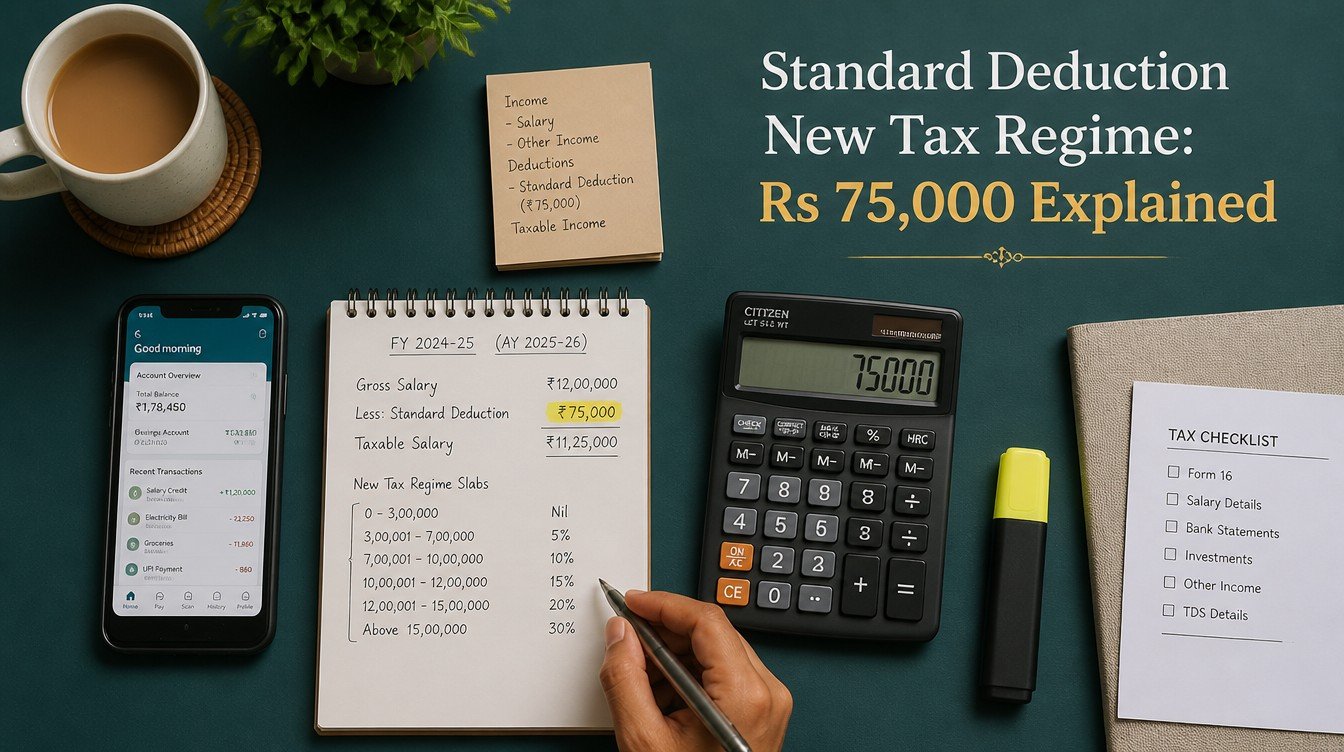

For FY 2024-25 and FY 2025-26: Rs 75,000 under the new tax regime and Rs 50,000 under the old tax regime. This means the new regime now has a higher standard deduction than the old regime, which is a reversal from the earlier position where both regimes had the same Rs 50,000 standard deduction.

Who Gets the Standard Deduction?

- Salaried employees: All salaried individuals receive the standard deduction automatically.

- Pensioners: Pensioners receiving pension from a former employer (not NPS/PPF) also receive the standard deduction from their pension income.

- Family pensioners: Budget 2024 extended the standard deduction to family pensioners (those receiving pension after a deceased pensioner) at Rs 15,000 or one-third of pension, whichever is lower – under both regimes.

- Who does NOT get it: Freelancers, self-employed professionals, and business owners do not receive the salary standard deduction (they have their own business expense deduction mechanism).

Standard Deduction: New Regime vs Old Regime

| Item | New Tax Regime | Old Tax Regime |

|---|---|---|

| Standard deduction amount | Rs 75,000 | Rs 50,000 |

| Applicable to | All salaried, pensioners | All salaried, pensioners |

| Documentation required | None | None |

| Additional deductions allowed | Very limited (80CCD(2), employer EPF) | 80C, 80D, HRA, home loan interest, and more |

The Rs 25,000 additional deduction in the new regime (Rs 75,000 vs Rs 50,000) translates to Rs 7,500 saved at 30% tax bracket. This is relatively small compared to the Rs 1.5 lakh+ deductions the old regime allows for active investors. The standard deduction enhancement was designed to make the new regime more attractive but does not by itself close the gap for taxpayers with significant 80C and HRA deductions. For a complete 2026 comparison including all slabs and deductions, the standard deduction is just one factor.

How Standard Deduction Reduces Tax Liability

Example: Salaried employee with Rs 15 lakh gross salary.

New regime calculation:

- Gross salary: Rs 15,00,000

- Minus standard deduction: Rs 75,000

- Taxable income: Rs 14,25,000

- Tax on Rs 14,25,000 under new regime slabs: approximately Rs 1,72,500 (before cess)

Old regime calculation (same employee, no other deductions):

- Gross salary: Rs 15,00,000

- Minus standard deduction: Rs 50,000

- Taxable income: Rs 14,50,000

- Tax on Rs 14,50,000 under old regime slabs: approximately Rs 2,22,500 (before cess)

Even with no other deductions, the new regime saves approximately Rs 50,000 in tax for this income level. The old regime only becomes better when 80C, HRA, and other deductions bring the old regime tax below Rs 1,72,500.

Standard Deduction and the Rs 12 Lakh Rebate

The new regime’s standard deduction interacts with the Section 87A rebate in an important way. The rebate makes effective tax zero for income up to Rs 12 lakh. With the Rs 75,000 standard deduction, a salaried employee with gross salary up to Rs 12,75,000 effectively pays zero income tax under the new regime:

- Gross salary: Rs 12,75,000

- Minus standard deduction: Rs 75,000

- Taxable income: Rs 12,00,000

- Tax before rebate: Rs 60,000 (new slabs)

- Section 87A rebate: Rs 60,000 (full rebate since tax is below Rs 60,000)

- Net tax: Zero

This makes the effective nil-tax threshold for salaried employees under the new regime Rs 12,75,000 gross salary. This is a significant advantage over the old regime, where the nil-tax threshold is much lower. Employees who also contribute to NPS through employer can further reduce their taxable income under the new regime via Section 80CCD(2).

Is the Standard Deduction Automatic or Does It Need to Be Claimed?

The standard deduction is automatic for salaried employees. Your employer deducts it when computing TDS on your salary each month – you do not need to submit any documents or proof. When filing your ITR, the standard deduction is pre-filled in the salary schedule. You simply verify that the correct amount (Rs 75,000 for new regime, Rs 50,000 for old regime) has been applied and move on. No investment required, no deadline to meet, no form to fill.

Frequently Asked Questions

Can I claim standard deduction under both new and old regime?

Yes, but the amount differs. Under the new regime, the standard deduction is Rs 75,000. Under the old regime, it is Rs 50,000. You claim the relevant amount based on whichever regime you choose for the assessment year. There is no option to claim more than the prescribed amount or to claim it multiple times.

Does the standard deduction apply to pension income?

Yes, for pensioners receiving salary-like pension from former employers. The standard deduction applies to pension income just as it does to salary. For NPS pension (from Tier 1 annuity after retirement), the treatment is different – the standard deduction may apply to the pension portion depending on how the pension is classified. Consult a tax advisor if you have both salary-based pension and NPS annuity income, as the interaction can be complex.

Was the standard deduction available in earlier years?

The standard deduction was reintroduced in Budget 2018 at Rs 40,000. It was raised to Rs 50,000 in Budget 2019. It remained at Rs 50,000 under both regimes until Budget 2024 raised it to Rs 75,000 specifically for the new tax regime. The old regime standard deduction remains at Rs 50,000. This asymmetry is intentional – it incentivizes taxpayers to choose the new (government-preferred) regime.

If I have two jobs in a year, do I get two standard deductions?

No. The standard deduction is Rs 75,000 per financial year per individual, regardless of the number of employers. If you changed jobs during the year, each employer computes TDS with the standard deduction. When you file your ITR combining salary from both employers, only Rs 75,000 total standard deduction applies. If both employers each deducted a standard deduction, you may have effectively claimed double deduction through their TDS – when consolidating in your ITR, apply only one Rs 75,000 deduction and ensure your total tax calculation is correct.

Is there a standard deduction for interest income or capital gains?

No. The Rs 75,000 standard deduction applies only to salary and pension income. There is no standard deduction for interest income, rental income, capital gains, or business income. Each of these income types has its own deduction mechanisms – interest income has no standard deduction (full amount is taxable); rental income has a 30% standard deduction under Section 24(a) for repairs and maintenance; capital gains have the Rs 1.25 lakh exemption for LTCG on equity.

Related Articles

- New Tax Regime vs Old Tax Regime 2026

- NPS Vatsalya Scheme: Complete Guide

- SIP vs Lumpsum: 20-Year Backtest