A belated return is the third-best option in the Indian tax calendar, behind an on-time return and a revised return. The belated itr penalty india 2026 framework rests on three statutory pillars: a Section 234F late-filing fee that caps at Rs.5,000, a Section 234A interest layer at 1% per month on unpaid tax, and an absolute December 31 cutoff after which only ITR-U is available. For FY 2025-26, the belated return window for most filers runs from August 1, 2026 (one day after the salaried deadline) to December 31, 2026, and missing it is more expensive than the headline Rs.5,000 fee suggests.

This guide breaks the cost into its components, walks through the 234A, 234B and 234C interest math, and explains why the December 31 cutoff still leaves an ITR-U fallback open for the next four years. References are to the Income Tax Act sections in force; filers should reconfirm any rate or threshold change against incometax.gov.in or the latest CBDT circular.

How the belated itr penalty india 2026 framework works

The framework has been redesigned over the last few years to be both progressive and forgiving up to a point.

Section 234F: the fixed late-filing fee

Section 234F imposes a flat fee at the time the return is filed late. The amount is capped, but it applies even when no tax is owed, as long as the return was required to be filed.

Section 234A: interest on unpaid tax

If self-assessment tax was due at the time of the original deadline but not paid, Section 234A interest applies from the day after the original due date until the date of actual payment. The rate is 1% per month or part of a month.

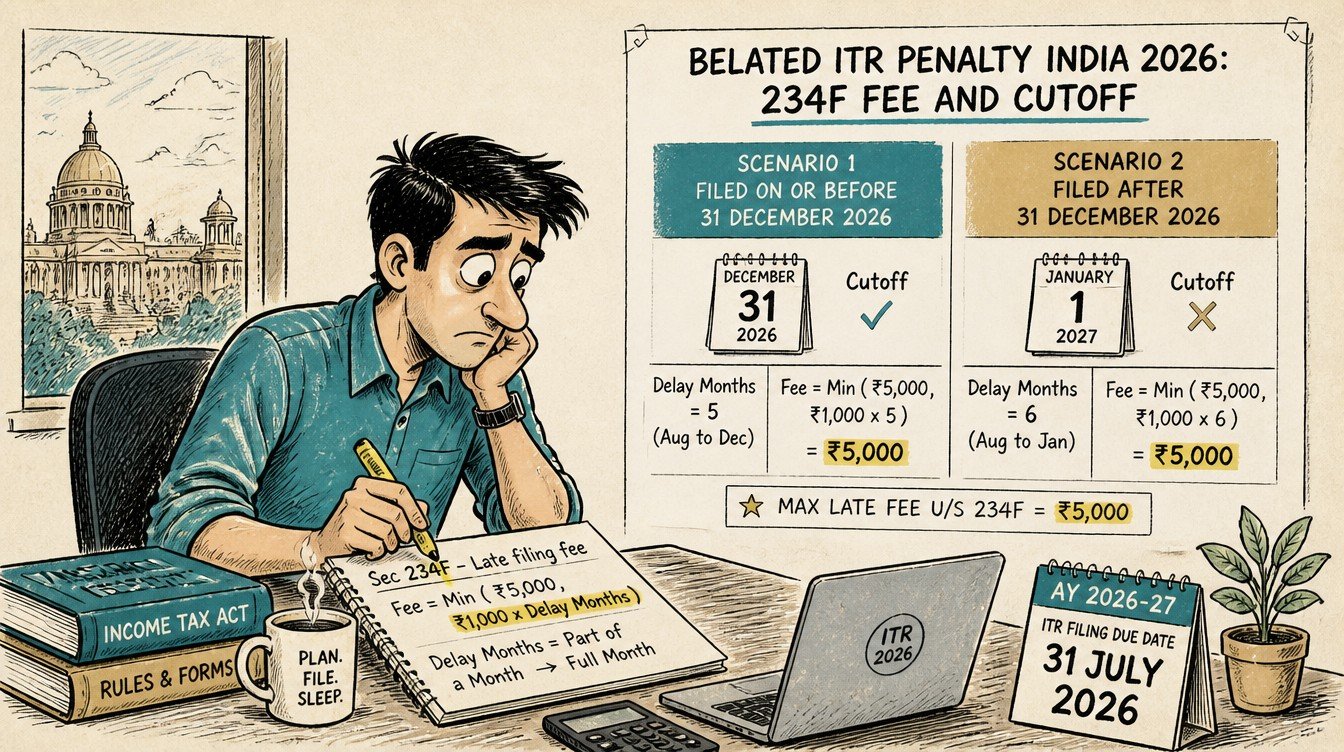

December 31 cutoff for belated returns

The belated return window closes on December 31 of the assessment year. After that, the only voluntary route is ITR-U under Section 139(8A), with its escalating 25% to 70% additional tax rates.

Section 234F fee structure

The 234F fee is the simplest component to compute.

Fee tiers

| Total income for the year | Section 234F fee |

|---|---|

| Up to Rs.5,00,000 | Rs.1,000 |

| Above Rs.5,00,000 | Rs.5,000 |

| Below basic exemption limit (and return not otherwise required) | Nil |

What triggers the fee

The 234F fee is triggered the moment the return is filed after the applicable original due date. The portal computes the fee automatically and includes it in the tax payable summary. Payment is mandatory before e-verification can be completed.

Who is exempt

Filers below the basic exemption limit who are not otherwise required to file (no foreign assets, no specified high-value transactions) are not liable for the 234F fee. The fee applies only when a return is statutorily required.

Section 234A interest: the bigger cost

234A interest often dwarfs the 234F fee for filers with unpaid liability.

Rate and computation

Interest under Section 234A is 1% per month or part of a month on the unpaid self-assessment tax. A 14-day delay counts as one full month for interest purposes, because the law treats any part of a month as a full month.

Worked example

Assume a salaried filer with self-assessment tax of Rs.40,000 due on July 31, 2026 but actually paid on October 15, 2026. The delay covers August, September, and October (three months counted at part-of-month basis). Interest = Rs.40,000 multiplied by 1% multiplied by 3 = Rs.1,200.

Where 234A bites the hardest

For filers with large unpaid liability, 234A compounds rapidly. A Rs.5,00,000 unpaid tax delayed by six months attracts Rs.30,000 of interest in addition to the Rs.5,000 234F fee, taking the total cost of delay to Rs.35,000.

Section 234B and 234C: the advance tax interest layers

Sections 234B and 234C predate the original filing deadline. They sit on top of 234A in the late-filing scenario.

Section 234B

Section 234B interest applies when advance tax paid during the year is less than 90% of the final assessed tax liability. The interest is 1% per month on the shortfall, computed from April 1 of the assessment year until the tax is finally paid.

Section 234C

Section 234C interest applies for deferment of specific advance-tax instalments through the year. The four instalments are due on June 15, September 15, December 15 and March 15, in cumulative percentages of 15%, 45%, 75% and 100% of the year’s tax. Missing any milestone attracts 1% per month interest for the deferral period.

Why these matter even for salaried filers

For salaried filers, TDS usually covers advance-tax requirements. But once capital gains or freelance income enters the picture, the advance-tax obligation re-emerges and 234B/234C can quietly add to the cost of a belated return.

Total cost of a belated return: a stacked example

Combining the layers gives a realistic picture.

Setup

Salaried filer with FY 2025-26 gross income of Rs.18,00,000. After deductions, taxable income Rs.15,50,000. Final tax liability Rs.2,30,000. TDS already deducted: Rs.1,80,000. Self-assessment tax shortfall: Rs.50,000. Filer also had Rs.3,00,000 of equity STCG in March 2026 that was not covered by TDS, leading to a Section 234C shortfall in the March instalment. Return filed on October 15, 2026.

Stacked computation

- Section 234F late fee: Rs.5,000 (income above Rs.5,00,000)

- Section 234A interest on Rs.50,000 unpaid tax for 3 months: Rs.1,500

- Section 234B interest on Rs.50,000 shortfall from April 1, 2026 to mid-October: roughly Rs.3,500

- Section 234C interest for the missed March instalment on STCG-related tax: roughly Rs.600-Rs.900

Total cost of delay

The aggregate cost of being roughly 75 days late is approximately Rs.10,500-Rs.11,000 in fees and interest, on top of the Rs.50,000 of unpaid tax itself. Filing the same return on the original July 31 deadline would have cost zero in 234F, while 234B and 234C interest may still have applied depending on advance-tax compliance during the year.

The December 31 cutoff and what lies beyond

The belated return window closes on December 31, 2026 for FY 2025-26.

What is allowed up to December 31

Filers can submit any pending FY 2025-26 return as a belated return under Section 139(4) up to December 31, 2026. They can also revise a previously filed return under Section 139(5) up to the same deadline, and the revision window is then extended to March 31, 2027 for FY 2025-26 returns under the Finance Act 2025 changes.

What happens on January 1, 2027

From January 1, 2027 onwards, no belated return for FY 2025-26 can be filed. The only voluntary route to declare missed income is ITR-U under Section 139(8A), which carries the 25% to 70% additional tax schedule on top of regular tax and interest.

The ITR-U fallback

ITR-U is available for FY 2025-26 income up to March 31, 2031 under the four-year extended window. The cost rises sharply each year, but the option exists. ITR-U cannot create a refund or reduce tax, only add to it.

Loss carry-forward: the hidden penalty

The biggest cost of a belated return often is not a fee, but a forfeited loss.

What losses are forfeited

A belated return cannot carry forward most loss categories, including business losses, capital losses (short-term and long-term), and speculation losses. Filers who book losses in a financial year and miss the original due date lose the right to offset those losses against future income.

The one loss category that survives

House property loss is the only loss that can be carried forward even from a belated return. All other loss categories require filing within the original due date for carry-forward eligibility.

Practical impact

For an F&O trader with a Rs.5,00,000 business loss in FY 2025-26 who files belatedly, the loss carry-forward is lost. If that loss could have offset Rs.5,00,000 of profits in FY 2026-27 at the 30% slab, the foregone tax benefit is Rs.1,50,000. This is several multiples of the 234F fee.

Refund delay and the practical workflow

Refunds on belated returns travel in a separate queue at CPC.

Typical processing timelines

On-time returns are typically processed in two to six weeks. Belated returns often take six to ten weeks, particularly when capital gains and other complex schedules are involved. Larger refunds attract additional verification and can take longer.

Interest on refund

Section 244A interest is paid on the refund at 0.5% per month. For belated returns, this interest is computed only from the date of filing the return, not from the start of the assessment year. Filing late therefore reduces the interest the taxpayer receives on the refund.

Verification still required

A belated return, like any other, must be e-verified within 30 days. An unverified return is treated as not filed, and the late-fee clock continues. The verification step is non-optional.

Common mistakes filers make with belated returns

Most belated-return errors fall into one of four buckets.

Paying self-assessment tax without 234A interest

Filers often compute and pay just the tax due, forgetting the 234A interest layer. The portal then flags a shortfall after submission. Add 234A interest in the challan before filing to avoid the rejection cycle.

Submitting without e-verification

A submitted but unverified return is not a filed return. The 234F fee and 234A interest continue to accrue until verification completes. The most common pattern is submission on December 30, followed by e-verification missed until January, which can render the entire effort moot.

Confusing revised and belated returns

A revised return under Section 139(5) requires an original return to revise. A belated return under Section 139(4) is the first return for the year, filed after the original due date. Selecting the wrong category in the portal is a common error.

Filing belated with the wrong ITR form

A belated return is still subject to the same form-selection logic as an on-time return. Filing in the wrong form triggers a Section 139(9) defective return notice, and the cure cycle eats into the limited window.

How to minimise penalty even when you are late

A few practical moves can reduce the cost when an on-time filing is not possible.

Pay self-assessment tax before filing

The 234A interest clock stops on the date tax is paid, not the date the return is filed. Paying the entire self-assessment tax through the e-pay tax facility before submission cuts off the interest accrual at that point.

File as early in the belated window as possible

234A and 234B both accrue monthly. Filing in August costs less than filing in November or December. The cost difference between an August belated return and a December belated return can be five or six times the 234F fee.

Avoid the December 31 cliff

Filing on December 31 carries higher risk because portal congestion late in the day can lead to submission failures. Build at least a week of buffer; a December 23 filing is materially safer than a December 31 filing.

Use the revision window even after belated filing

If the belated return has errors, the revised return route remains open until March 31 of the next year (for FY 2025-26, that is March 31, 2027). A revised return can fix mistakes without re-triggering 234F.

Edge cases worth knowing

Three edge cases shape the cost more than most filers realise.

Refund-only belated returns

If a refund is owed and no tax is unpaid, 234A interest does not apply. The 234F late fee still does, unless the filer is below the basic exemption threshold and not otherwise required to file. Refund-only filers should still file as early as possible to start the 244A interest clock for the refund itself.

Filers with TDS in excess of liability

Some filers have TDS already covering all liability, with even a small excess pending as refund. The 234F fee still applies if income exceeds the threshold, but the 234A interest layer drops to zero because no tax is unpaid.

Foreign-asset holders

Resident filers holding foreign assets are required to file a return even if income is below the basic exemption. Missing the deadline triggers Section 234F. For Black Money Act exposures, the consequences extend well beyond Section 234F into a separate penalty regime that this article does not cover.

FAQ

What is the last date to file a belated return for FY 2025-26?

The belated return for FY 2025-26 can be filed up to December 31, 2026 under Section 139(4). After that, only ITR-U under Section 139(8A) is available, with the year-wise additional tax of 25% to 70%.

How much is the Section 234F fee?

Rs.1,000 for total income up to Rs.5,00,000 and Rs.5,000 for total income above Rs.5,00,000. Filers below the basic exemption limit who are not otherwise required to file are exempt from the fee.

Does Section 234A interest apply if there is no unpaid tax?

No. Section 234A interest is computed on unpaid self-assessment tax. If TDS plus advance tax fully covers the final liability, 234A interest is zero, although Section 234F may still apply.

Can a belated return be revised later?

Yes. A belated return can be revised under Section 139(5) up to March 31 of the assessment year for FY 2025-26 returns under the Finance Act 2025 changes. The revision does not re-trigger Section 234F.

What happens if the December 31 deadline is missed?

The only voluntary disclosure route after December 31 is ITR-U under Section 139(8A), available for up to 48 months from the end of the relevant assessment year. The additional tax escalates from 25% in the first 12 months to 70% in the fourth year.

Related guides on this topic are coming to learnfinedge.com soon.