The way money leaves the household has changed more in the last seven years in India than in the previous seventy. The same monthly grocery, fuel, and dining outlay that used to flow through a wallet of physical notes and one or two cards now flows through three or four UPI apps with two-tap confirmations. Behavioural research from across India and internationally consistently suggests that cash vs upi spending india produces measurably different outcomes for the same person buying the same goods: more transactions, smaller average ticket size, and lower recall at month-end. This guide unpacks the psychology, the use-case matrix, and the digital alternatives to old-school envelope budgeting.

The aim is not to argue that cash is better or that UPI is worse. The aim is to give a salaried Indian household a practical framework for choosing the right method for the right category of spend, with awareness of how each method nudges behaviour, so that the convenience of UPI does not quietly translate into a higher monthly burn rate at the same income level.

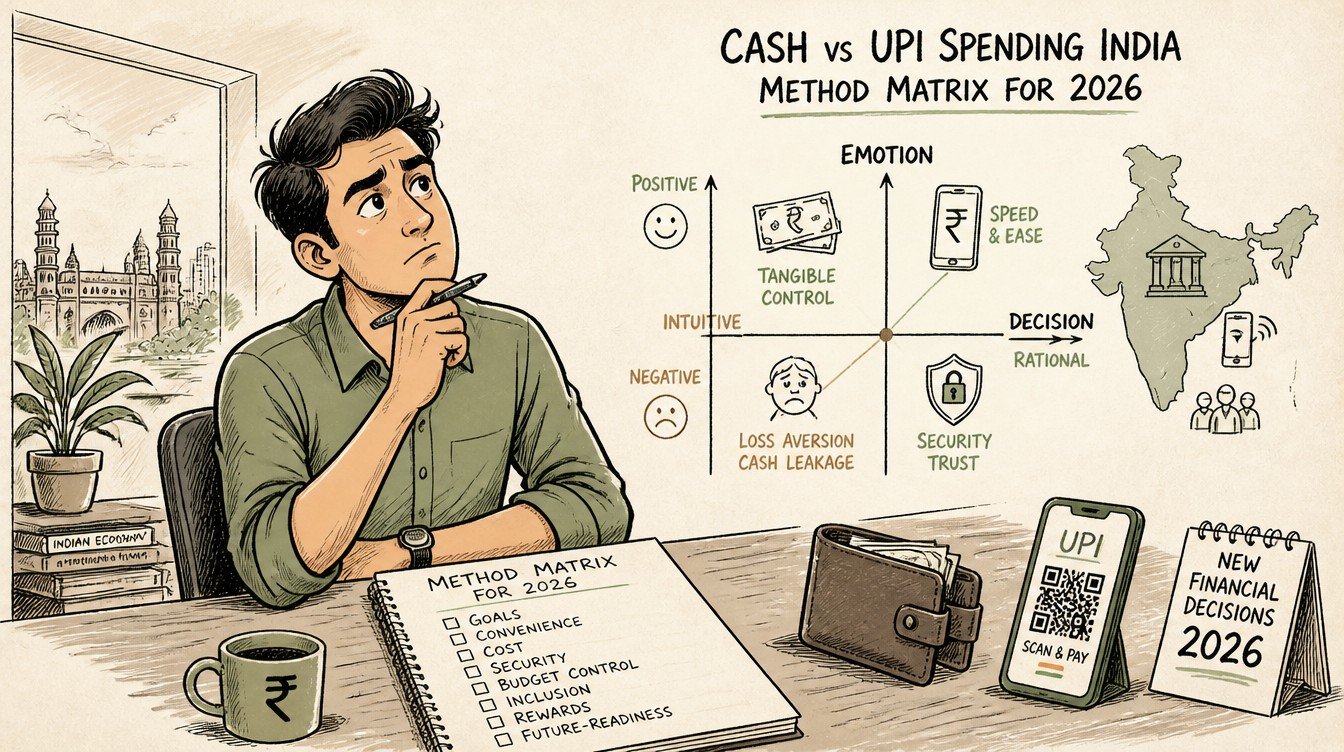

The Pain of Payment: Why the Method Matters

The “pain of payment” is a well-documented concept in behavioural research: the psychological friction associated with handing over money. Cash creates the highest pain, because the physical transfer of notes is visible, tangible, and final. Cards create moderate pain, because the swipe and the PIN are deliberate acts that take a few seconds. UPI creates the lowest pain, because the entire transaction is a two-second QR scan and a single tap.

Why low pain leads to more spending

When the pain of payment falls, the brain’s natural braking system on discretionary spend weakens. Studies of Indian UPI users have suggested that a majority report higher overall spending after adopting UPI as the primary payment method, and a meaningful share report having exceeded their budget specifically because of UPI’s frictionless nature. The same person buys more often, for smaller amounts, at categories where the cash version would have prompted a pause.

The recall problem

A second consistent finding is that UPI users have weaker recall of their monthly spending without consulting the transaction history. The brain encodes physical-cash transactions more durably because the tactile experience leaves a memory trace; UPI transactions are encoded weakly and fade. The end-of-month surprise at the bank statement is the symptom.

The transaction-count multiplier

UPI also changes the velocity of transactions. The average household that ran 60 to 80 cash transactions a month before 2018 routinely runs 250 to 400 UPI transactions a month in 2026. Many of those are micro-spends (Rs.20 chai, Rs.40 auto fare, Rs.80 snack) that the cash-era version would have either skipped or batched. The aggregate is rarely small.

How Cash Disciplines Spending

Cash is the oldest budgeting tool because it has a structural property that no digital method replicates: the wallet is a hard constraint.

The visible-balance effect

A person who starts the day with Rs.2,000 in the wallet sees the balance fall with every spend. The visible-balance effect produces a continuous, low-grade reminder of how much remains for the rest of the day or week. UPI replaces this with an invisible balance that is only known when the app is opened, which usually happens after the spend, not before.

The withdrawal as a budget moment

The act of withdrawing cash from an ATM is itself a small budget moment. The user has to decide how much to withdraw, and the decision is made deliberately rather than reactively. UPI removes this moment entirely, because there is no withdrawal step between the bank account and the spend.

Where cash still wins for discipline

Categories like household-help payments, small daily groceries from the local kirana, eating-out budgets for the week, and personal discretionary spends (the monthly “for me” budget) often work better in cash because the constraint is automatic. The household that wants to cap dining at Rs.6,000 a month has an easier time enforcing it if dining is paid in cash from a labelled envelope.

Where Cards Sit on the Pain Spectrum

Credit cards and debit cards occupy a middle position between cash and UPI on the pain spectrum, but the two card types behave very differently and deserve separate treatment.

Debit cards: cash-adjacent, with a delay

Debit cards draw from the bank balance directly, similar to UPI, but the swipe-and-PIN step adds a small friction. The pain is lower than cash but higher than UPI, particularly for in-person transactions. Online debit-card payments lose this friction and feel more like UPI than like cash.

Credit cards: deferred pain

Credit cards introduce a fundamentally different dynamic: the pain is deferred to the statement date, which is usually 20 to 50 days after the spend. The brain’s evaluation of the transaction happens in the absence of pain, which is why credit-card holders consistently spend more per transaction than debit-card or cash users on the same category. The reward-points layer adds a subtle positive nudge that further offsets pain.

The minimum-due trap

Credit cards become structurally dangerous when the household pays only the minimum due. APRs on Indian credit cards typically range from 36 to 42 percent annualised. A revolving Rs.50,000 balance left untouched for a year produces an interest cost well above any reasonable household budget. The pain of payment is permanently deferred, and the debt compounds.

UPI: The Lowest-Friction Method India Has Ever Had

UPI’s design is optimised for speed, interoperability, and merchant acceptance, which makes it the most efficient payment rail in India. Monthly UPI transaction volumes per NPCI statistics are now consistently in the tens of billions, with the share of low-value transactions growing year over year.

What UPI does brilliantly

UPI is excellent for known, planned spends: utility bills, monthly subscriptions, rent payments, insurance premiums, SIP investments, fixed-amount transfers to family. In these categories, the low friction is a feature, not a bug, because the spend amount is already decided.

What UPI does poorly from a budgeting view

UPI is structurally weak for discretionary spends: dining, impulse purchases, late-night online orders, casual snack purchases, and weekend entertainment. The same low friction that helps with bills hurts with category-creep, and the lack of a visible balance allows over-spend to accumulate silently.

The auto-pay layer

UPI auto-pay (e-mandates) is a powerful tool for committed flows like SIPs and utility bills, where automation removes the risk of missed payments. The same auto-pay used for streaming subscriptions, ride-hailing wallets, and impulse subscriptions becomes a quiet leak that the household never notices until the annual review. Periodic audit of every active UPI mandate is essential.

The Use-Case Matrix: Which Method for Which Spend

A practical framework matches the payment method to the category, not the other way around. The matrix below is the working version most Indian households can adapt.

| Category | Best method | Why |

|---|---|---|

| Rent, EMIs, SIPs, insurance premiums | UPI auto-pay or NACH | Fixed amount, low decision risk, automation prevents missed payments |

| Utility bills (electricity, gas, broadband) | UPI or credit card | Predictable amount, occasional reward-point benefit on card |

| Monthly groceries (large supermarket run) | Credit card (paid in full) | Reward points, return-policy backstop, single statement entry |

| Daily groceries (local kirana) | UPI or cash | Small amounts, vendor preference often matters |

| Dining out (planned, restaurant) | Credit card (paid in full) or cash | Hard category cap easier in cash; reward points on card |

| Impulse dining and snacks | Cash | Hard wallet limit creates natural cap; UPI accelerates over-spend |

| Online shopping (Amazon, Myntra) | Credit card (paid in full) | Return-window protection, dispute resolution, cashback |

| Travel and large discretionary | Credit card (paid in full) | Insurance benefits, reward redemption, fraud protection |

| Cash to household help, parking, tips | Cash | Vendor preference, fast, no transaction history clutter |

| Investment transfers (SIPs, FDs) | UPI or net-banking | Direct from bank, no intermediate card |

The category-cap principle

The matrix works only if each row has an associated monthly cap that the household has actually decided on. UPI for utilities is fine because the amount is fixed by the bill; UPI for dining is dangerous because there is no natural cap. The cap is the budgeting layer; the payment method is the enforcement layer.

Why credit card “paid in full” matters

The credit card recommendations above assume the household pays the statement balance in full every month. Any revolving balance changes the math entirely: the reward points are negligible compared to the 36 to 42 percent interest cost on the unpaid principal. The rule is simple: spend on credit card only what can be paid off on the statement date in full.

Digital Envelope Budgeting for the UPI Era

The traditional envelope-budgeting method splits monthly cash into labelled envelopes (groceries, dining, transport, entertainment, miscellaneous) and treats each envelope as a hard category cap. The method works in cash because the envelope is physically empty when the spend exceeds the budget. Reproducing this in a UPI-first household needs a digital adaptation.

The multi-account envelope

The cleanest digital envelope is a multi-account setup: one bank account for fixed monthly commitments (rent, EMIs, SIPs, utilities), one account for variable household spend (groceries, dining, fuel), and one account for personal discretionary spend. The salary credit is split across the three accounts on day 1 of the month, in fixed percentages. Each account is a digital envelope.

The pre-loaded wallet method

For categories that already attract UPI heavily (dining, food delivery), pre-loading a fixed amount into a UPI wallet (PhonePe wallet, Google Pay balance) at the start of the month creates a hard cap. The wallet runs dry when the category cap is exhausted, and the household has to make a conscious decision to top up.

The weekly cash allowance

A weekly cash withdrawal of a fixed amount (e.g., Rs.3,000 for personal discretionary spend) creates a tactile envelope that compensates for the UPI default. The withdrawal happens on the same day every week, and the amount is fixed regardless of how much remained from the previous week. The cash itself enforces the cap.

The end-of-month review

Whatever the digital envelope method, the monthly review covers the same four steps each time.

- Pull statements from the main bank account, secondary account, and credit card.

- Compare actual category spend against the envelope or cap that was set.

- Identify the two or three categories that overflowed the cap.

- Adjust the cap, the payment method, or the underlying habit for the next month.

Common Mistakes in Mixing Cash, Card, and UPI

The same mistakes show up across most Indian households that have not consciously designed their payment-method mix.

Using UPI for everything because it is fastest

Default-UPI is the most common pattern in urban Indian households in 2026, and it is the single largest driver of category creep. The fix is not to abandon UPI but to consciously route certain categories away from it (dining, impulse, personal discretionary) into either cash or a credit card with a cap.

Treating credit card as a payment method without paying in full

Credit cards are useful as a payment method only when paired with a discipline of paying the statement balance in full. Households that revolve a balance pay a structural interest cost that exceeds any plausible benefit from the cards. If the discipline is hard to maintain, the credit card should be downgraded to debit card or UPI for daily use.

Ignoring the auto-pay leak

UPI auto-pay subscriptions accumulate quietly: streaming services, food-delivery memberships, app subscriptions, cloud-storage plans, micro-investment apps. The household that does not audit auto-pay mandates at least once a year ends up paying for two or three services it does not actively use. The annual audit is a 30-minute exercise that often saves Rs.10,000 to Rs.20,000 a year.

Confusing convenience with discipline

UPI is convenient, not disciplined. The two qualities are independent, and the household has to provide the discipline through caps and category routing. Convenience without discipline is just faster spending; discipline without convenience is just slower spending. The goal is convenience plus discipline, which the matrix and envelopes provide.

Designing the Household Payment Stack

The final piece is the household-level payment stack: the set of accounts, cards, UPI apps, and cash arrangements that together implement the matrix.

The minimum viable stack

For most salaried Indian households, the minimum viable stack contains five pieces.

- One salary account for fixed commitments (rent, EMIs, SIPs, utilities).

- One secondary account for variable household spend (groceries, fuel, dining).

- One credit card for online and large planned purchases, paid in full monthly.

- One primary UPI app linked across both accounts for general payments.

- A small weekly cash allowance for personal discretionary spend.

The dual-account split

The salary-account-plus-secondary-account split is the foundation of digital envelope budgeting. The salary account funds rent, EMIs, SIPs, and utilities through standing instructions and UPI auto-pay. The secondary account holds the variable-spend allocation for the month and is replenished only on the next salary day.

The annual stack review

Once a year, audit the entire stack. List every active UPI app, every credit card, every auto-pay mandate, every standing instruction, and every linked merchant. Cancel anything not actively used. Consolidate where possible. The reduced stack is easier to manage and harder to leak from.

When to add a payment method back

Adding a new payment method (a new credit card, a new UPI app, a new digital wallet) should require a specific reason that cannot be served by the existing stack. The default answer to “should I get this card” is no, unless the card delivers a category benefit (travel, fuel, dining) that the household actually uses heavily.

FAQ

Does using UPI really make me spend more than cash?

Behavioural research from Indian and international studies consistently suggests that lower-friction payment methods are associated with higher spending frequency, smaller average ticket size, and weaker recall of monthly spend. Whether the absolute monthly total rises depends on the household’s category mix and budgeting discipline. The cleanest test is to track three months of UPI-default spending against three months of mixed-method spending with explicit category caps.

Should I switch back to mostly cash for daily spending?

A complete switch is rarely practical because UPI acceptance has become the default in urban India. A more useful approach is selective cash use for high-leak categories (personal discretionary, dining, impulse) and UPI for fixed-amount categories (bills, rent, EMIs, SIPs). The hybrid model captures most of the discipline benefit without losing the convenience benefit.

Is a credit card always worse than UPI for spending discipline?

Not always. A credit card paired with strict “pay in full on the statement date” discipline can be neutral or positive for net wealth because of reward points, dispute protection, and cleaner monthly statements. The same credit card paired with a revolving balance is structurally damaging at typical Indian APRs of 36 to 42 percent. The discipline determines the outcome, not the card.

How do I track auto-pay mandates across multiple UPI apps?

Each UPI app (Google Pay, PhonePe, Paytm, the bank’s app) maintains its own list of active mandates under a section usually labelled “Autopay” or “Subscriptions”. Reviewing each app once a quarter and cancelling unused mandates is the simplest approach. The bank statement shows the actual debits, which is the cross-check against the in-app list.

What is the easiest first step if I feel my UPI spending is out of control?

Start with a single category cap: pick the category with the highest UPI burn (often dining or food delivery), set a monthly Rs. amount that is 70 percent of last month’s spend in that category, and route any spend above the cap to cash for the remainder of the month. The friction of the cash route either prevents the spend or makes it conscious. One category at a time is enough to learn the pattern; ten at once is unmanageable.

Related guides on this topic are coming to learnfinedge.com soon.