If your home loan EMI dropped silently in early 2026 without you doing anything, you owe the credit to a quiet but powerful rule the Reserve Bank of India imposed on banks back in October 2019. That rule is the External Benchmark Lending Rate, and understanding how eblr home loan reset india 2026 works is the difference between getting the full benefit of every RBI cut and leaving money on the table.

This guide walks through what EBLR is, how it mechanically pegs new floating-rate retail loans to the RBI repo, why your EMI resets within 90 days of any policy move, and what to do if your bank has not delivered the reset you were promised. It contrasts EBLR with the older MCLR regime, walks through worked EMI examples, and gives a clean step-by-step recovery plan if you are still on a slower benchmark.

The thesis is simple. In 2026, EBLR is the most consumer-friendly retail lending rule India has ever adopted, and it has done its job during this easing cycle. But it only helps borrowers who know it exists and ask for what they are owed.

EBLR Full Form and Why RBI Introduced It

EBLR stands for External Benchmark Lending Rate. In September 2019, RBI mandated that banks must link all new floating-rate retail loans (home loans, personal loans, MSME loans) to one of four external benchmarks: the RBI policy repo rate, the 3-month Treasury Bill yield, the 6-month Treasury Bill yield, or any other benchmark published by Financial Benchmarks India Private Limited.

In practice, almost every major Indian bank picked the repo rate. So when retail borrowers see EBLR, they should read it as “repo plus spread”. The rule took effect for new floating-rate loans sanctioned from October 1, 2019.

Why RBI moved away from MCLR

Before EBLR, retail floating-rate loans were priced on Marginal Cost of Funds Based Lending Rate (MCLR), which is an internal benchmark each bank computes from its own cost of funds. RBI found that MCLR transmission was slow and uneven. Banks would cut MCLR slowly when the repo dropped but raise MCLR quickly when the repo rose, hurting borrowers.

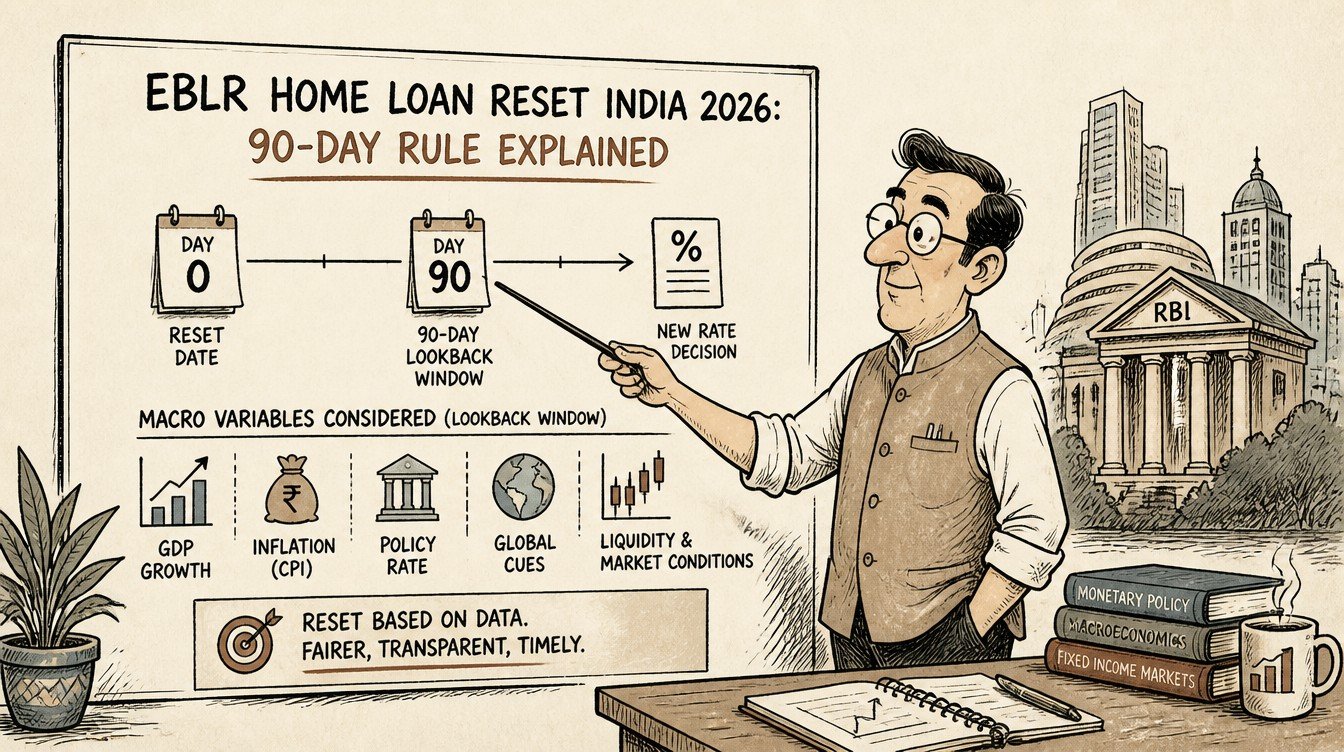

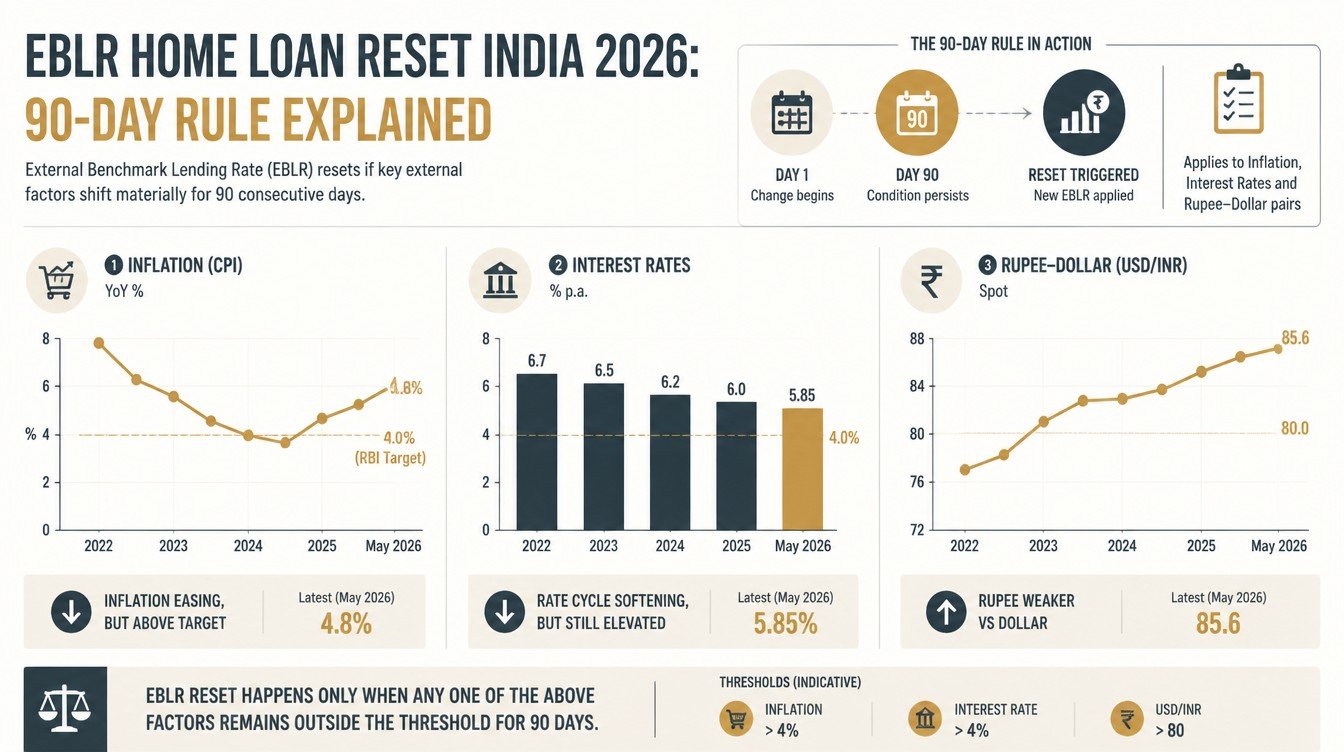

The 90-day reset rule

Under EBLR, banks must reset borrowers’ interest rates at least once every three months. So when the MPC cuts the repo, every EBLR-linked retail borrower must see a corresponding reduction in their effective rate within 90 days, with the new rate reflected in the next EMI or the same EMI over a shorter tenure.

Loans EBLR applies to

EBLR applies to floating-rate retail loans sanctioned from October 2019: home loans, top-up loans on EBLR home loans, personal loans, education loans, vehicle loans, and MSME loans. Fixed-rate loans and loans sanctioned before October 2019 (which sit on MCLR or older base rate) are outside EBLR’s scope unless the borrower switches.

How EBLR Mechanically Works

The lending rate under EBLR has two components: the external benchmark and the spread.

External benchmark = RBI repo rate (for most banks)

The repo rate sits at 5.25% as of May 2026. This is the benchmark every EBLR home loan at a typical Indian bank starts from.

Spread = bank’s margin + risk premium

On top of the benchmark, the bank adds a spread that includes its operating margin, business strategic spread, and a credit risk premium specific to each customer. The spread for prime salaried customers at large banks typically falls in the 2.5% to 3.5% range. Self-employed borrowers and lower-credit-score borrowers face higher spreads.

Net effective rate = benchmark + spread

So a salaried home loan borrower at a large bank in May 2026 might see an effective rate of 5.25% (repo) + 3.00% (spread) = 8.25%. Different banks and different customer profiles will land in slightly different bands but the arithmetic is identical.

Why your spread is locked but your benchmark moves

Once your spread is fixed at sanction, banks cannot arbitrarily widen it later (they can adjust only on credit events specified in the loan agreement). The benchmark, however, moves with every MPC decision. That is what makes EBLR so consumer-friendly: as the repo falls, your rate falls in lockstep, with the spread untouched.

EBLR Home Loan Reset India 2026: The 90-Day Math

The 90-day reset rule is the heart of EBLR. Here is how it plays out in practice when the MPC moves.

Reset cycle 1: the day of the MPC decision

When the MPC cuts the repo by, say, 25 basis points, the change is immediate for the policy rate. But your loan does not automatically reprice the next morning. Banks operate on monthly billing cycles.

Reset cycle 2: the next billing cycle

Most banks reset EBLR-linked loans on the first day of the month following the MPC decision, or on the contractual reset date specified in the sanction letter. The change reflects in either the EMI or the tenure or both, depending on what the borrower opted for at sanction.

Reset cycle 3: the 90-day backstop

Even if some banks delay, RBI rules require the reset to happen at least once every 90 days. If your bank has not reset by the 90-day mark, you have a regulatory case to escalate.

A worked EMI walkthrough

Take a borrower with a Rs.50,00,000 (50 lakh) home loan, 18 years left, at an effective EBLR rate of 8.50% before the cuts. After a cumulative 125 bps cut cycle, the new rate is 7.25%. The EMI on the old rate is roughly Rs.45,200. The EMI on the new rate (same tenure) is roughly Rs.41,700. That is a saving of roughly Rs.3,500 per month, or about Rs.42,000 a year, just from the reset.

MCLR vs EBLR: Which Benchmark Are You On?

Many borrowers are still unsure which benchmark their loan sits on. Here is a clean comparison.

| Feature | MCLR | EBLR |

|---|---|---|

| Full form | Marginal Cost of Funds Based Lending Rate | External Benchmark Lending Rate |

| Type of benchmark | Internal to the bank | External (RBI repo or T-Bill) |

| RBI rule effective from | April 2016 | October 2019 |

| Reset frequency | Annual (sometimes 6 months) | At least once every 90 days |

| Transmission speed | Slow and uneven | Fast and mechanical |

| Borrower visibility | Bank-determined, opaque | Tied to publicly announced repo rate |

| Applies to new loans from | 2016 to October 2019 | October 2019 onwards |

How to confirm which one you are on

Pull your sanction letter or the latest provisional interest certificate. Look for the lending rate clause. It will say either MCLR-linked (with a one-year or 6-month MCLR reference) or EBLR-linked (with a repo rate or T-Bill reference). If the loan was sanctioned after October 2019 and is floating, it should be EBLR.

If you are still on MCLR after October 2019

Some borrowers were given the option in 2019-2020 to migrate from MCLR to EBLR but chose to stay on MCLR. If you are in this group, it is worth running the switch math now. The transmission gap between MCLR and EBLR has widened over the easing cycle.

Switching from MCLR to EBLR

Most banks allow a one-time conversion from MCLR to EBLR (or sometimes to a different EBLR product within the same bank) for a fee. The fee is usually a small percentage of the outstanding loan or a flat amount, depending on the bank’s policy. Check the latest schedule of charges before assuming. The conversion is irreversible.

What to Do If Your Bank Has Not Reset Your EMI

If 90 days have passed since the most recent MPC move and your EMI has not changed, you have a legitimate complaint. Here is the practical escalation path.

Step 1: Pull the documents

Download the provisional interest certificate from the bank’s online portal for the most recent month. Note the current effective rate. Cross-check against the bank’s published EBLR plus spread for your customer category.

Step 2: Email the relationship manager

Send a written email to the relationship manager (or branch home loan desk) asking for confirmation of (a) the current effective rate, (b) the date of the most recent reset, and (c) the impact of the most recent MPC moves on the loan. Banks are obliged to respond within their stated SLA.

Step 3: Escalate to the bank’s grievance redressal officer

Every Indian bank has a nodal grievance officer for retail lending. If the relationship manager’s response is unsatisfactory, send a formal complaint to the grievance officer citing RBI’s EBLR rules. Reference the relevant RBI master direction in the email.

Step 4: RBI Ombudsman

If the bank’s grievance officer does not resolve the issue within 30 days, file a complaint with the RBI Ombudsman through cms.rbi.org.in (the centralised online portal). Ombudsman complaints on EBLR reset failures are typically actioned quickly because they reference a clear rule.

EMI Walk-through with Real Numbers

Numbers ground the concept. Here are three borrower profiles to make the math tangible. None of the numbers should be treated as a recommendation for any specific lender or product.

Profile A: First-time buyer, Rs.30,00,000 loan

A salaried first-time home buyer with a Rs.30,00,000 (30 lakh) 20-year EBLR home loan at 8.25% (repo 5.25% plus spread 3.00%) pays an EMI of roughly Rs.25,560. If the repo drops by another 25 bps to 5.00%, the new rate becomes 8.00% and the EMI (same tenure) drops to roughly Rs.25,090, saving about Rs.470 a month.

Profile B: Mid-career upgrader, Rs.75,00,000 loan

A mid-career buyer with a Rs.75,00,000 (75 lakh) 20-year EBLR home loan at 8.50% (repo 5.25% plus spread 3.25%) pays an EMI of roughly Rs.65,140. A cumulative 25 bps further cut to 5.00% takes the EMI (same tenure) to about Rs.63,930, saving roughly Rs.1,200 a month.

Profile C: Top-up + home loan combination

Profile C borrows a base home loan plus a top-up two years in. If both are EBLR-linked at slightly different spreads, both reset within 90 days of an MPC move, but the bank’s reset windows may not be identical. Verify each separately.

Why EMI versus tenure choice matters

When a cut comes through, the bank’s default is usually to shorten the tenure rather than reduce the EMI. Borrowers who want the cash flow relief in pocket should explicitly request EMI reduction. Borrowers focused on early loan closure should accept the default tenure cut.

EBLR for Non-Home-Loan Retail Loans

EBLR applies to several other floating-rate retail products as well, though the spreads vary.

Personal loans

Floating-rate personal loans are typically priced at much wider spreads over EBLR than home loans (often 5% to 10% over repo, reflecting unsecured credit risk). The 90-day reset still applies on the benchmark portion, but the wide spread means the rate change is felt less proportionally.

Vehicle loans

Some banks offer floating-rate vehicle loans linked to EBLR. The spread sits between home loans and personal loans. Many vehicle loans, however, are fixed-rate; in that case EBLR is irrelevant for that loan and only an early closure or refinancing changes anything.

MSME loans

MSME cash credit, working capital, and overdraft facilities are predominantly EBLR-linked at most banks. Small business borrowers should treat the post-MPC reset window as an opportunity to renegotiate the spread along with absorbing the benchmark cut.

Education loans

Education loans are mostly EBLR-linked. Borrowers in the moratorium phase still see the rate movement but typically without immediate EMI consequences because the moratorium structure deferred payments.

Should You Lock in a Fixed Rate Instead?

Some banks offer fixed-rate or part-fixed-part-floating home loan products. With the repo at 5.25% after a 125 bps cycle of cuts, the temptation to lock at the floor is real. The trade-off, however, is not straightforward.

The case for fixed-rate

If you believe the easing cycle is fully over and the next move is up, locking the fixed rate now insulates you from future hikes. The fixed-rate option also gives certainty for budgeting.

The case against fixed-rate

Fixed-rate home loans in India are typically priced 50 to 100 basis points higher than EBLR floating-rate loans at sanction. So you are paying a premium for certainty. If the MPC cuts further (even one more 25 bps), the floating-rate borrower benefits while the fixed-rate borrower does not.

The middle path: hybrid loans

Some banks offer hybrid products where the rate is fixed for an initial period (3-5 years) and then converts to floating. These can suit borrowers who want short-term certainty but long-term flexibility.

What most experienced borrowers do

For long-tenure home loans (15+ years), most experienced Indian borrowers stay on EBLR floating because over that horizon, the average rate has historically been lower than the rate fixed at sanction. Past patterns are not a guarantee but they inform the default.

Common Mistakes Borrowers Make Around EBLR

Assuming the bank will reset automatically

The 90-day reset is a rule, but borrowers should still verify it has happened. Many borrowers discover later that a reset was applied to tenure rather than EMI, or that the reset reflects a different effective rate than expected.

Not asking about the spread at sanction

The spread is the lifelong portion of the rate. A 50 basis point lower spread saves lakhs over a 20-year loan. Negotiate it at sanction, especially if you have a strong credit profile.

Refinancing without doing the math

Some borrowers refinance to a different bank attracted by a slightly lower headline rate. By the time you factor in conversion fees, MOD charges, and the loss of the relationship history, the actual benefit can be far smaller than expected.

Ignoring the MCLR-to-EBLR switch

Borrowers on MCLR continue to pay above-market rates because they have not actioned the one-time switch. Run the math for your specific outstanding and residual tenure before assuming the switch is not worth it.

The 2026 Outlook: What EBLR Borrowers Should Watch

With the repo paused at 5.25% in April 2026 and the next MPC scheduled for June 3-5, 2026, EBLR-linked borrowers face a quieter window than the active easing cycle months. What to watch:

The June MPC outcome

A further cut would mean another 25 bps EMI relief within 90 days. A hold means no fresh relief; focus shifts to absorbing the cuts already delivered.

Bank-specific spread movements

Some banks tweak their spreads on new sanctions even when the benchmark is unchanged. Refinancing a high-spread legacy loan to a fresh sanction at a lower spread is a legitimate optimisation in this environment.

Liquidity and CRR signals

Even when the repo is unchanged, RBI’s liquidity management can ease or tighten short-term funding costs for banks, which indirectly impacts deposit and lending behaviour over the medium term.

FAQs on EBLR Home Loan Reset 2026

What is the EBLR full form?

EBLR stands for External Benchmark Lending Rate. It is the RBI-mandated benchmark, effective October 2019, against which all new floating-rate retail loans (home, personal, MSME, education, vehicle) must be priced. For most large banks, the benchmark is the RBI policy repo rate, so EBLR effectively means “repo plus the bank’s spread”.

How fast must my bank reset my EMI after an RBI cut?

RBI rules require EBLR-linked retail loans to reset at least once every 90 days. Most banks reset within the next billing cycle after a repo move. If 90 days have passed and your effective rate has not changed, you can file a written complaint with the bank’s grievance officer and escalate to the RBI Ombudsman if unresolved.

What is the difference between MCLR and EBLR?

MCLR is an internal benchmark computed by each bank from its own cost of funds. EBLR is an external benchmark (typically the repo rate). EBLR resets at least every 90 days; MCLR resets annually or every 6 months. EBLR transmits RBI policy moves to borrowers faster and more mechanically than MCLR did.

Should I switch from MCLR to EBLR in 2026?

If your home loan is on MCLR and the spread between your current rate and the prevailing EBLR rate for your profile is more than 25 to 50 basis points, the switch typically pays back within a year for a residual tenure of 10+ years. Run the specific math (one-time conversion fee versus annualised savings) before deciding.

Does EBLR apply to my fixed-rate home loan?

No. EBLR applies only to floating-rate retail loans sanctioned from October 2019. Fixed-rate loans are outside its scope. If you want EBLR benefits and you are on a fixed-rate loan, you would have to either refinance to a floating-rate product or wait for the fixed-rate period to end if your loan has a hybrid structure.

Related guides on home loan prepayment math, the MPC reading framework, and FD vs home loan prepayment trade-offs are forthcoming on LearnFineEdge.