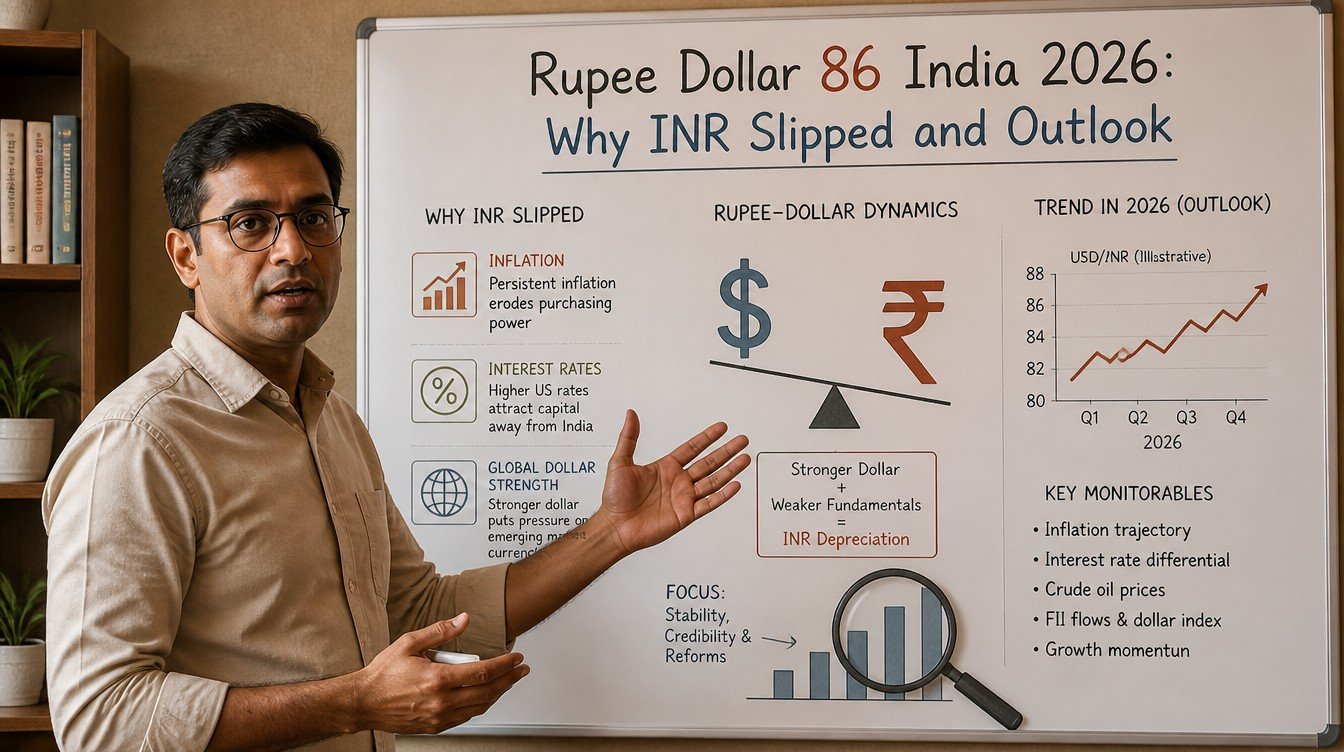

The Indian rupee crossed the psychologically loaded Rs.86 per US dollar mark in 2026 and has stayed under pressure for much of the year. This rupee dollar 86 india 2026 guide walks through the four forces driving the move (FII flows, the trade gap, oil prices, and the US Federal Reserve’s path), the Reserve Bank of India’s intervention pattern, and what an Indian household or retail investor can sensibly do about it.

Currency moves rarely make daily household budgets shift overnight. They do, however, drive imported inflation, FX-sensitive equity sectors, NRI remittance economics, and the relative attractiveness of dollar-denominated assets. Salaried Indians, NRIs sending money home, parents funding foreign education, and retail investors with US ETF holdings all have a real stake in the rupee.

The thesis is simple. The rupee’s path past 86 in 2026 reflects a confluence of cyclical and structural pressures, RBI is actively managing the slide rather than fighting it absolutely, and households can hedge selectively without trying to predict the next big figure.

Rupee Dollar 86 India 2026: What Actually Happened

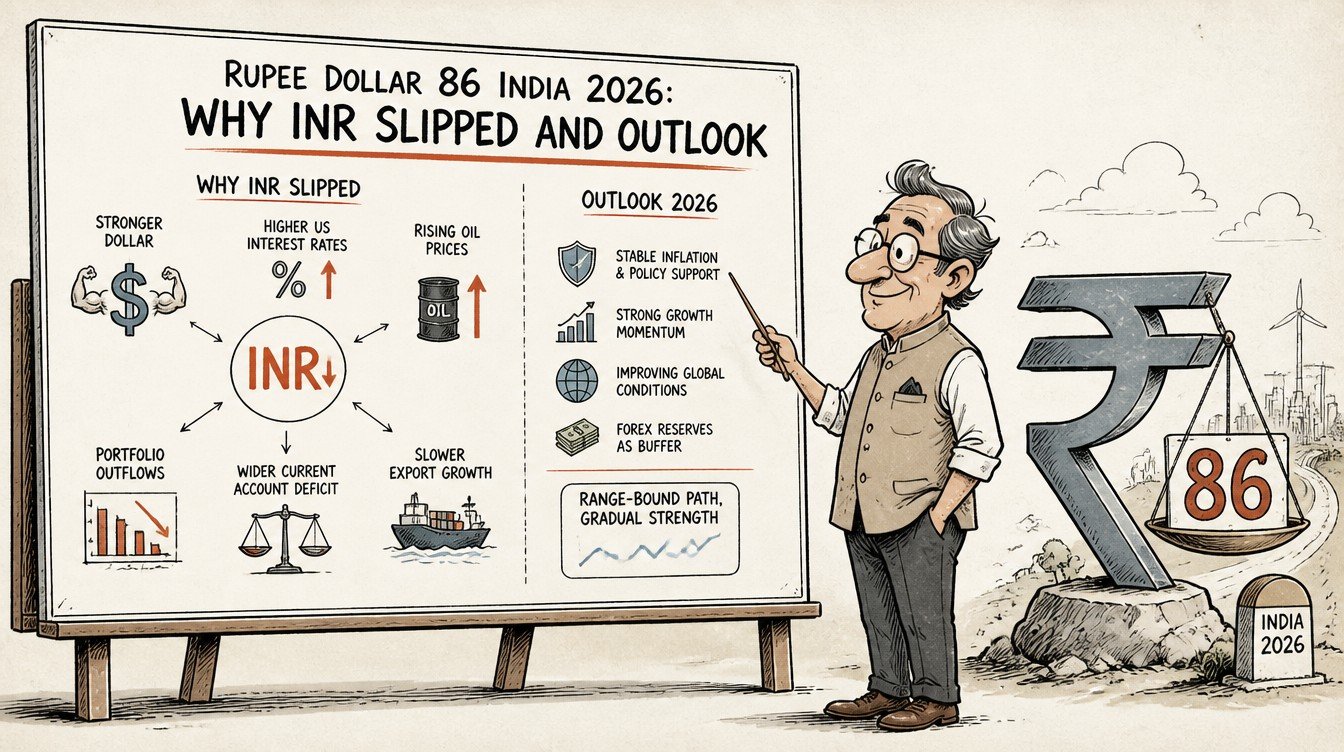

Through 2025, the rupee held a relatively stable range around the Rs.83 to Rs.85 per dollar zone. Through early 2026, the currency steadily depreciated, breaching Rs.86 and then drifting lower as the year progressed under a combination of capital outflows, a persistent trade deficit, and a strong-ish US dollar against a basket of emerging market currencies.

The RBI has been active in the foreign exchange market through this period, selling dollars from reserves and conducting dollar-rupee swap auctions to smooth volatility. The central bank’s stated objective is to manage excessive volatility rather than defend a specific level.

Why 86 matters as a psychological line

Currency markets do not respect round numbers, but financial commentary and household psychology do. The Rs.86 line was the previous resistance through 2025, and breaching it triggered headline coverage that itself nudged behaviour: importers hedged more aggressively, exporters delayed conversions, and household sentiment toward INR weakened modestly.

Where INR sits in the broader EM context

The rupee has not been alone. Other Asian emerging market currencies have also weakened against the dollar through 2026, though to varying degrees. On a real effective exchange rate (REER) basis (which accounts for inflation differentials), the rupee’s depreciation is less stark than the nominal headline suggests.

Force 1: FII Flows and the Capital Account

Foreign Institutional Investor (FII) equity flows are the single largest swing factor for the rupee in any given quarter. When FIIs buy Indian equities, they convert dollars to rupees, supporting INR. When FIIs sell, they convert rupees to dollars, pressuring INR.

The 2026 outflow pattern

FII equity flows have been net negative for stretches of 2026. The pull factors that previously drew FIIs to Indian equities (relative growth premium, predictable earnings) have not disappeared, but the push factor (higher US Treasury yields, dollar strength) has been winning the short-term tug of war.

FPI debt flows

FPI debt flows under the Fully Accessible Route (FAR) and other windows have been a partial offset. The inclusion of Indian government bonds in major global EM bond indices has brought structural inflows over multi-year horizons, though month-to-month flows still oscillate.

What FII flows look like for retail to track

FII daily and monthly flow data is published by NSDL and CDSL and tracked widely in financial media. Retail investors do not need to predict flows, but watching the cumulative monthly net flow gives a useful read on the rupee’s tailwind or headwind.

Force 2: Trade Deficit and Current Account

India’s trade deficit (goods imports minus goods exports) has consistently exceeded its services trade surplus and remittances combined in some quarters, leading to a current account deficit (CAD). The bigger the CAD, the more imported dollars are needed monthly, and the more sustained pressure on the rupee.

Why imports keep pressuring INR

India’s import basket is dominated by crude oil, gold, and electronic goods. All three are dollar-denominated commodities or imports. A heavier import bill mechanically pulls the rupee lower because the daily demand for dollars rises.

Why exports do not fully offset

India’s goods export basket (refined petroleum products, gems and jewellery, engineering goods, pharmaceuticals, textiles) has grown but not at the pace of imports. Services exports (IT, business services) are stronger but volatile.

The remittance buffer

Remittances from the Indian diaspora are a sizeable inflow line, often estimated at over USD 100 billion annually in recent years. These provide a structural buffer that has kept the current account from widening too dramatically.

Force 3: Oil Prices and the Energy Bill

India imports a significant share of its crude oil requirement. Even a small movement in global crude prices (say Brent moving from USD 75 to USD 90) translates into billions of dollars of additional import bill annually, directly worsening the trade deficit.

The Russia discount window

India has benefited from discounted Russian crude purchases through parts of 2024-2026, partially insulating it from full price exposure. This discount window has narrowed over time as supply patterns normalised.

What an oil spike does to the rupee mechanically

A USD 10 per barrel sustained rise in crude prices roughly adds about USD 15-18 billion to India’s annual oil import bill (depending on import volumes). That widens the trade deficit and pressures the rupee in proportion.

Why oil is the most-watched macro variable for INR

If you can watch only one macro variable to predict INR direction, watching Brent crude is a reasonable choice. Currency desks routinely model INR with a strong oil-price coefficient.

Force 4: The US Federal Reserve and the Rate Differential

The interest rate differential between US Treasury yields and Indian government bond yields drives carry-trade flows. When the differential narrows, carry trade demand for INR weakens.

Where rates sit in 2026

The US Federal Reserve has been cautiously easing through 2025 and into 2026, but its pace has been slower than markets initially priced. With 10-year US Treasury yields hovering in the 4% range and Indian 10-year G-Sec yields around 7%, the differential of about 3% remains positive for INR but narrower than the historical average.

What a hawkish Fed surprise does

A hawkish surprise from the US Fed (delaying further cuts, hinting at hikes) typically strengthens the dollar against EM currencies including INR. A dovish surprise (signalling faster cuts) eases pressure on INR.

The dollar index (DXY) as a quick proxy

The DXY measures the dollar against a basket of major currencies (euro, yen, pound, etc.). A rising DXY usually means a softer INR even if no India-specific news has dropped. DXY at elevated levels in 2026 has been a persistent headwind.

RBI Intervention Pattern: How the Central Bank Manages the Slide

RBI’s stated FX policy is to manage excessive volatility, not to defend a fixed exchange rate. The central bank has multiple tools and uses them in combination.

Spot market intervention

RBI sells dollars (and occasionally buys) in the spot FX market via state-owned banks, smoothing intra-day moves. Reserves are the firepower. India’s foreign exchange reserves remain among the largest globally even after intervention through 2026.

Forward and swap auctions

The RBI conducts dollar-rupee buy-sell swap auctions, dollar-rupee forwards, and similar instruments to influence forward rates and manage liquidity simultaneously. These are surgical tools used at moments of stress.

NRI deposit incentives

FCNR(B) and NRE deposit windows can be calibrated to attract NRI dollar inflows. Past episodes of rupee stress have seen RBI use these windows aggressively. Similar discussions and measures have been part of the 2026 toolkit.

Verbal guidance and communication

RBI communications, including the Governor’s commentary and the post-MPC press conference, signal the central bank’s tolerance band. Markets read this carefully.

What the Rupee at 86+ Means for Indian Households

A weaker rupee has a layered impact on different parts of household finance.

Imported inflation pinch

Petrol, diesel, LPG (partially), cooking oils, electronics, and luxury imports all become costlier in rupee terms when INR weakens. The full pass-through is often muted by government tax adjustments and corporate margin compression, but the directional pressure is real.

Foreign education and travel

Indian students studying abroad and families paying tuition or living expenses in dollars feel the move directly. A tuition fee of USD 30,000 a year that cost about Rs.24,90,000 at Rs.83 per dollar now costs roughly Rs.25,80,000 at Rs.86 per dollar, and more at further INR levels.

Foreign holidays

Travel to the US, UK, or Europe becomes more expensive in rupee terms. Even intra-Asia travel feels the move through hotel and airline pricing.

NRI remittances become more valuable

Money sent home from the Gulf, the US, the UK, or Singapore buys more rupees when INR is weaker. For Indian families receiving NRI remittances, this is a partial silver lining.

Imports of consumer goods

iPhones, premium consumer electronics, luxury fashion, and imported wines all see selective price revisions over time. Demand for these is relatively inelastic in the urban affluent segment, so brands sometimes pass through more of the move.

USD-Hedge Options for Indian Retail Investors

Retail investors who want some dollar exposure (whether to hedge education plans, to diversify, or to participate in US equity returns) have multiple legitimate routes within Indian regulations.

Liberalised Remittance Scheme (LRS)

Each Indian resident can remit up to USD 2,50,000 (2.5 lakh) per financial year under LRS for permitted purposes, including overseas investment. TCS at 20% applies above certain thresholds for specified categories. LRS is the primary direct route for retail to take US dollar exposure beyond domestic vehicles.

India-listed international ETFs and mutual funds

Several Indian mutual fund schemes and ETFs track US indices (Nasdaq 100, S&P 500). These provide dollar exposure indirectly: rupee weakness boosts rupee-denominated returns over time. SEBI has applied periodic caps on overseas investment limits for Indian MFs, so check the scheme’s open-or-closed status.

Sovereign Gold Bonds and physical gold

Gold has historically had a meaningful negative correlation with INR strength. When the rupee weakens (and global gold rises), domestic gold prices in INR tend to rise faster than international gold in dollars. Sovereign Gold Bonds (when available) and gold ETFs are the regulated retail routes.

NRE/FCNR deposits (for NRIs)

NRIs holding dollars can park them in FCNR(B) deposits earning interest in foreign currency, or convert and hold INR-denominated NRE deposits with full repatriability. The choice depends on the NRI’s view on future INR moves and tax residency.

Hedging via Indian exchange-traded currency derivatives

Retail traders can use USD-INR currency futures and options on NSE and BSE to hedge specific dollar exposures or to take a directional view. These instruments carry leveraged risk and are unsuitable for most retail investors without a clear hedging need.

How RBI Repo Rate Interacts with the Rupee

The MPC’s rate decisions affect the rupee through the interest rate differential and the carry trade.

A rate cut narrows the differential

Each RBI repo cut, all else equal, narrows the rate differential between Indian and US sovereign yields, making INR less attractive in carry-trade terms. This is one reason a rupee under stress can constrain how aggressively the MPC eases.

The April 2026 pause and the rupee

The RBI MPC’s pause at 5.25% in April 2026 with a neutral stance preserves optionality. If rupee stress eases, room reopens for further cuts. If rupee stress persists, the MPC may stay paused longer.

A rate hike is the rupee defender of last resort

If rupee depreciation becomes disorderly and threatens financial stability, the MPC has the option (rarely used in recent cycles) to hike rates to defend the currency. The bar for this is high. Markets price it as a tail risk rather than a base case.

Approximate USD-INR Levels and What They Imply (Illustrative)

The table below is an illustrative framing, not a forecast.

| USD-INR Range | What it typically signals | Likely household feel |

|---|---|---|

| Rs.82 to Rs.84 | Calm INR, healthy FII inflows, stable oil | Foreign travel and education feels reasonable |

| Rs.84 to Rs.86 | Mild pressure, neutral global backdrop | Marginal imported inflation, minimal household disruption |

| Rs.86 to Rs.88 | Active RBI intervention, sustained outflows or oil pressure | Education and travel costs visibly higher in INR |

| Beyond Rs.88 | Significant stress, possible policy response | Real bite on imports, electronics, premium consumer goods |

How to read this table

The bands are not predictions and do not imply that any specific level is sustainable, defended, or imminent. They show how the rupee’s environment is typically described and what each band implies for daily life.

Common Mistakes Indian Households Make About the Rupee

Panic-buying dollars at the highs

Some families convert all their LRS quota to dollars when INR weakens dramatically, reasoning that the slide will continue. This is the same mistake as buying any asset purely on momentum. A more disciplined approach is to spread LRS conversions over the year for goals (education funding, overseas investment).

Stopping foreign equity SIPs at weak INR

SIPs into international funds should not be paused because INR is weak. The point of SIPs is to average out the entry over time. Pausing during weakness defeats the rupee-cost-averaging benefit.

Holding too much in foreign currency without a clear use

Holding excess dollars without a defined goal (education, migration, US asset purchase) generates currency volatility for no productive purpose. Match the currency holding to the actual liability.

Ignoring forex transaction costs

Bank-to-bank forex spreads and TCS components can erode 1% to 3% of a remittance. Comparing two or three remittance providers (banks vs specialised remittance services) is worth a few minutes for any meaningful amount.

Where the Rupee Could Head: Three Plausible Paths

None of these paths is a forecast. They are framings to help readers think about the range of outcomes.

Path 1: Stabilisation

If oil prices ease, FII flows turn supportive, and the Fed cuts faster than expected, INR could stabilise in a band and recover modestly. This scenario depends on multiple external factors aligning.

Path 2: Range-bound depreciation

If oil and FII flows remain mixed, INR could drift in a modestly weaker band with periodic RBI intervention. This is a continuation scenario.

Path 3: Further weakness

A combination of an oil spike, sustained FII outflows, and dollar strength globally could push INR further. The RBI would likely intervene more aggressively, and the MPC’s room for rate cuts would narrow.

What households should actually do

Match currency exposure to currency liabilities. Stay invested in domestic SIPs. Use LRS for goals, not for speculation. Watch oil and FII flows as the two leading indicators.

FAQs on the Rupee-Dollar Outlook

Why did the Indian rupee cross Rs.86 against the US dollar in 2026?

The rupee crossed Rs.86 per dollar in 2026 due to a combination of FII equity outflows, a persistent trade deficit, sustained dollar strength globally, and oil price pressure on the import bill. The RBI has been intervening to smooth volatility but its stated policy is to manage excessive moves rather than defend a specific level.

What is RBI doing to support the rupee?

The RBI uses a combination of spot dollar sales from reserves, dollar-rupee swap auctions, forward market intervention, and verbal guidance. The central bank has also explored measures to attract NRI inflows (FCNR/NRE deposit incentives). The objective is to manage volatility, not to fix the exchange rate at any specific level.

How does a weaker rupee affect my household budget?

A weaker rupee adds imported inflation pressure on petrol, diesel, electronics, edible oils, and consumer imports. It makes foreign education, foreign travel, and dollar-denominated purchases more expensive in INR terms. NRI remittances to Indian families gain value, which is a partial silver lining.

Should I move my savings to US dollar assets?

For a salaried Indian resident, moderate diversification into US equity through India-listed international funds or LRS-based US accounts can make sense if it matches a real goal (education funding, planned migration). Switching the majority of savings to dollars purely on a currency view is rarely sensible and exposes you to unhedged INR appreciation risk.

Will RBI raise rates to defend the rupee?

A rate hike to defend the currency is technically possible but unlikely in the near term. RBI prefers FX market intervention, swap operations, and inflow measures over rate hikes. A hike would only be considered if rupee depreciation became disorderly and threatened broader financial stability. The MPC has emphasised data dependence, and rate decisions are not pre-committed.

Related guides on LRS rules and TCS, US ETF tax treatment in India, and Sovereign Gold Bonds are forthcoming on LearnFineEdge.