The single most useful number in a salaried Indian household’s financial life is rarely the monthly salary. It is the net worth: the simple difference between everything owned and everything owed, computed once a year on a consistent basis. Yet most thirty-something Indian professionals have never sat down to do a clean net worth calculation india exercise, partly because the household balance sheet looks more complicated here than in most textbook examples. EPF and NPS sit in employer portals. Ancestral property has murky titles. Jewellery is valued anywhere between purchase price and market gold. Home loans run for two more decades. This guide builds the worksheet from scratch in the Indian context.

The aim is a template that any salaried professional in their thirties can fill in 60 to 90 minutes using statements already available across bank, demat, EPF, NPS, and policy portals. The output anchors every other financial decision for the next year.

What Net Worth Means in the Indian Household Context

Net worth is assets minus liabilities, valued on the same date for both sides of the balance sheet. The arithmetic is simple; the judgement is in deciding what counts as an asset, at what value, and what counts as a liability. The Indian context introduces several wrinkles that the standard textbook does not address.

The basic equation

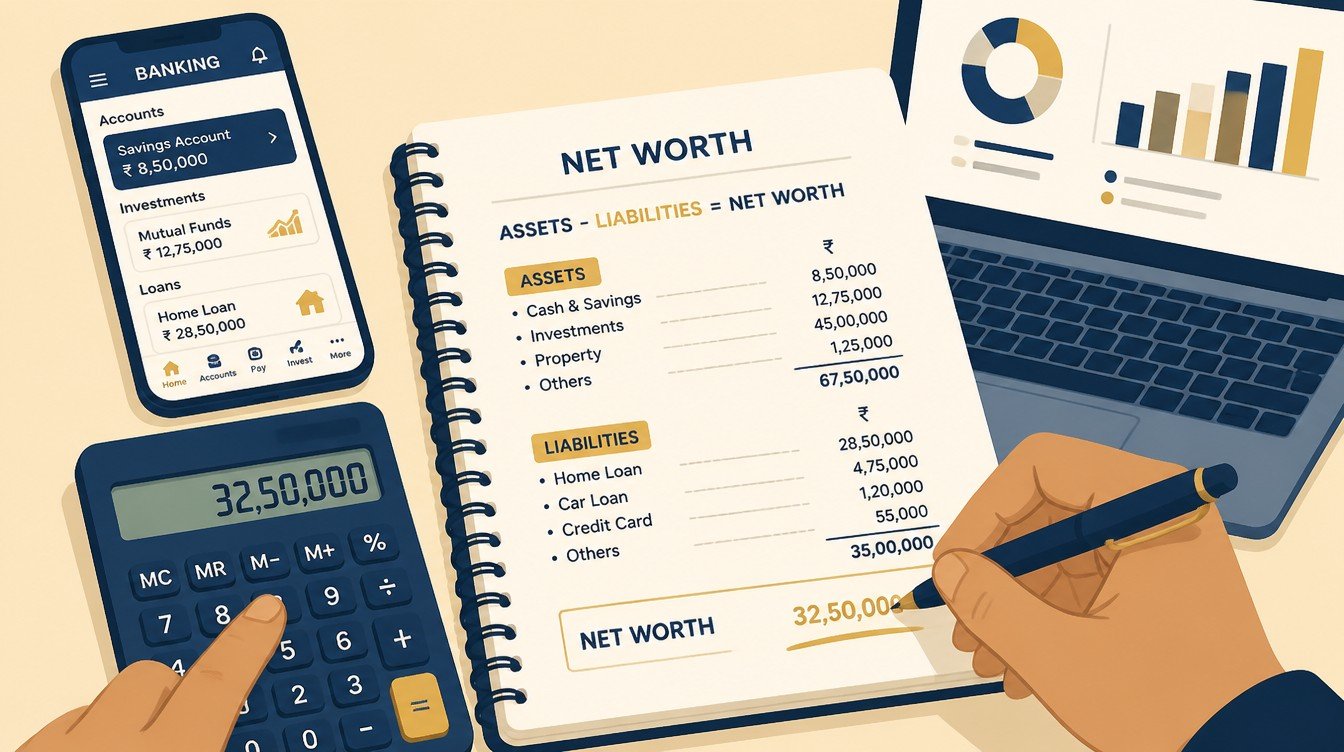

Net worth = total assets at market value – total liabilities at outstanding balance. The market-value rule is critical. Real estate held since 2010 should be valued at the current circle-rate or comparable-sale benchmark, not the purchase price. Gold should be valued at the current per-gram rate, not the rate on the day it was bought.

Why salaried 30-somethings need this number

The early-thirties decade is when most Indian salaried earners take on the largest single liability of their lives (a home loan) and accumulate the largest asset they will own for the next twenty years (EPF plus retirement equity). Without a net-worth baseline, the household drifts; with one, every appraisal cycle can be evaluated as a net-worth delta rather than an income delta.

The annual review rhythm

A common rule of thumb in Indian personal finance is to do the net-worth exercise once a year, in early April after the previous financial year closes. The timing aligns with EPF and NPS statements, Form 16, and year-end fund factsheets, so the data is fresh. The same date used every year keeps the year-on-year comparison clean.

The Asset Side: What Every Indian Household Should List

The asset list for a typical salaried thirty-something household in India runs across seven or eight categories. Each has its own valuation rule.

Liquid assets

Savings account balances across all banks, fixed-deposit balances at face value (or maturity value if the deposit matures within the next 12 months), recurring-deposit balances, and any money sitting in liquid or overnight mutual funds. These are valued at the current statement balance. Sweep-in FDs sitting inside a savings account get listed at their FD value, not the savings rate.

Market-linked financial assets

Equity mutual fund holdings at the latest NAV times units, debt mutual funds at NAV, direct equity holdings at the latest closing price on NSE or BSE, ELSS holdings, and any International Funds at INR-converted NAV. The CAMS or KFintech consolidated statement is the cleanest source for mutual-fund holdings across AMCs. Market-linked instruments carry market risk; read scheme-related documents carefully before drawing conclusions about future returns.

Retirement assets

EPF balance from the EPFO Member portal (statutory plus voluntary contributions plus interest credited to date), NPS Tier I balance from the CRA statement at current NAV, NPS Tier II if any, PPF balance at the current statement, Atal Pension Yojana corpus if applicable, and any superannuation or gratuity accruals. EPF and NPS are real and accessible assets and belong on the list at full statement value, even though the access is restricted until retirement.

Insurance with surrender value

Traditional endowment policies, money-back policies, and ULIPs at their current surrender value or fund value, not the sum assured. Pure-term life insurance has no surrender value and stays off the asset list (its value lives on the protection side of the plan, not the balance sheet). For ULIPs, the NAV-based fund value is the right number; the policy bonus is a future estimate, not a current asset.

The Tricky Indian Assets: Gold, Jewellery, and Ancestral Property

The three asset classes that derail most Indian net-worth exercises are gold jewellery, ancestral or jointly held real estate, and inherited assets with unclear paper title. Each needs a defensible valuation rule.

Gold and jewellery

List gold (coins, bars, ETFs, sovereign gold bonds) at the current per-gram market rate. For jewellery, list 85 to 90 percent of the per-gram rate to account for the making-charge differential that does not recover on resale. The weight is taken from the original invoice or a fresh assessment; the price is taken from the IBJA daily rate or a comparable benchmark. The result is the realistic resale value, not the insurance-replacement value.

Ancestral and jointly held property

If the property is ancestral and held jointly with siblings or parents without a partitioned share, the conservative rule is to list only the legal share at current market value, and only if the family has discussed and broadly agreed on the share. Properties with unresolved title or in dispute should be carried at zero or with an explicit note, not at the full optimistic market value.

Self-occupied home, second property, vehicles

The self-occupied home and any second property are listed at current market value from a comparable sale or registered-valuer estimate, with a 5 to 7 percent transaction-cost footnote so the net-of-cost figure is visible when needed. A car or two-wheeler is listed at the current Insured Declared Value (IDV) from the latest motor-insurance renewal. Electronics, furniture, and household items are excluded as consumption assets, not wealth assets.

The Liability Side: Every Rupee That Is Owed

The liability side is usually shorter than the asset side but deserves the same attention. Every active loan and every revolving credit facility shows up here.

Secured loans

Home loan outstanding principal from the latest sanction-letter statement or net-banking screen, plus any pending pre-EMI or moratorium interest. Loan against property at the principal outstanding. Auto loan at the outstanding principal, not the original sanctioned amount. Each loan is listed at its outstanding principal, not the EMI; the EMI is a cash-flow concept, not a balance-sheet concept.

Unsecured loans

Personal loans at outstanding principal. Education loans at outstanding principal (including any moratorium accrual). Credit-card revolving balance at the current outstanding (not the credit limit). Loan against fixed deposits or securities at outstanding principal. Any informal family loans that the household intends to repay are also listed here.

Tax liabilities and reserved cash flows

Any self-assessment tax dues from the last filed return, advance-tax pending from the previous financial year, and TDS shortfalls flagged in Form 26AS or AIS belong on the liability side. A school admission fee due in May or an insurance premium due in June, by contrast, are cash-flow timing items, not balance-sheet liabilities, and should be kept out of the net-worth statement to avoid double-counting against the same expense in the household budget.

The One-Page Net Worth Worksheet

The full template fits on a single A4 page or one tab of a spreadsheet. The layout below is the simplest version that survives a multi-year tracking effort.

| Category | Sub-line | Value (Rs.) |

|---|---|---|

| Liquid | Savings + FD + RD + liquid funds | … |

| Market-linked | Equity MF + debt MF + direct equity + ELSS | … |

| Retirement | EPF + PPF + NPS + superannuation | … |

| Insurance value | ULIP fund value + endowment surrender value | … |

| Gold and jewellery | Coins, bars, SGB, jewellery at 85-90 percent | … |

| Real estate | Self-occupied + second property at market | … |

| Vehicle | Car + two-wheeler IDV | … |

| Total assets | … | |

| Home loan | Principal outstanding | (…) |

| Other secured | LAP, auto loan | (…) |

| Unsecured | Personal loan, education loan, card | (…) |

| Tax dues | SA tax, advance tax, TDS shortfall | (…) |

| Total liabilities | (…) | |

| Net worth | Assets – liabilities | … |

How to populate the worksheet in 60 minutes

- Pull the latest CAMS or KFintech consolidated mutual fund statement.

- Pull the EPFO passbook from the Member portal and the latest NPS CRA statement.

- Pull a recent demat holding statement and latest closing prices for direct equity.

- Pull bank and FD balances across all banks via net-banking screens.

- Estimate real-estate value from a recent comparable sale or registered-valuer note.

- Estimate gold and jewellery weight from invoices, valued at the current IBJA rate.

- Pull loan outstanding principals from the bank or NBFC net-banking screen.

What to do with the final number

The single net-worth number is most useful when it is tracked over time. Save the worksheet with a date stamp, repeat the exercise on the same date next April, and compare year-on-year. A healthy salaried household sees the net worth grow faster than CPI, with the gap funded by savings and investment growth, not by adding new assets bought with new loans.

Rough Indian Net Worth Milestones by Age

Benchmarks are imprecise, vary by city tier, and depend heavily on family obligations, but rough milestones help calibrate progress. Treat the numbers below as directional, not prescriptive, and adjust for personal context like inherited assets, sole-earner households, or two-income households.

By age 30

A common informal benchmark in metro India is a net worth roughly equal to one year of gross annual income by age 30. For a salaried earner at Rs.12,00,000 (12 lakh) annual income, that suggests a net worth of about Rs.12,00,000. The dominant components are usually EPF, a starter mutual-fund SIP, and modest emergency savings. Home-loan EMIs have typically not started yet at this stage.

By age 35

By age 35, two to three times annual income is a reasonable target for households without major family-support obligations. For the same Rs.12,00,000 earner growing to Rs.18,00,000 (18 lakh), that suggests a net worth of Rs.40,00,000 to Rs.55,00,000. A home loan may have started, so the gross asset base is higher but the net is moderated by the loan principal.

By age 40

By age 40, five to six times annual income is a sensible target for a dual-income household, lower for a sole-earner household. The composition shifts toward retirement assets (EPF, NPS, equity mutual funds) and home equity as the loan principal amortises. Lifestyle inflation usually accelerates around this age, which is when net-worth tracking starts to do the most work.

How to Treat EPF, NPS, and Restricted Retirement Assets

EPF and NPS together usually form the largest single line on a salaried thirty-something’s asset side, often larger than mutual funds or direct equity. They deserve a clear treatment rule.

EPF at full balance

The EPF balance, including employer contribution, employee contribution, any voluntary provident fund (VPF), and interest credited, is listed at full passbook value. The interest rate is notified annually by EPFO and credited typically once a year. Partial withdrawals taken for permitted purposes (home, medical, education) reduce the balance and should be reflected at the latest statement.

NPS at current NAV

NPS Tier I corpus is listed at current NAV across the chosen asset-class mix (E, C, G, A). The CRA statement provides the consolidated value. NPS Tier II, if any, is also listed at NAV. The annuity-purchase requirement at retirement does not change the current balance-sheet value, but is worth noting as a footnote so the household understands the future liquidity profile.

PPF and the liquid vs total split

PPF balances across self, spouse, and children are each listed at current value; the 15-year lock-in constrains liquidity but not value. Once the worksheet is filled, splitting the total into “liquid net worth” (excluding retirement assets and real estate) and “total net worth” is a useful refinement. Liquid net worth drives emergency and discretionary decisions; total net worth drives retirement readiness.

Common Mistakes in Indian Net-Worth Calculations

The same handful of mistakes show up year after year in household net-worth exercises. A clean checklist avoids the worst of them.

Counting the sum assured of term insurance as an asset

A Rs.1,00,00,000 (1 crore) term plan is a protection instrument, not an asset. Adding the sum assured to the asset side inflates the net worth by the protection cover. Only ULIP fund value and endowment surrender value belong on the asset list. The pure-term cover is captured separately in the family’s protection plan, where it belongs.

Listing real estate at purchase price

A flat bought in 2014 at Rs.45,00,000 (45 lakh) is not worth Rs.45,00,000 in 2026; it is worth whatever the current comparable-sale price is. Listing at purchase price understates the household’s wealth in rising markets and overstates it in flat or declining markets. The current market value is the only defensible number.

Forgetting credit-card revolving balance

Credit-card revolving balance at typical APRs in the 36 to 42 percent range is one of the costliest liabilities. Households that pay the minimum due regularly forget to list the outstanding because the statement reads as a routine bill. The full outstanding belongs on the liability side until cleared.

Using the Net Worth Number to Drive Decisions

The annual net-worth exercise is only useful if it changes at least one decision in the next twelve months.

Insurance adequacy check

A rough rule of thumb is that life-insurance sum assured should be 10 to 15 times annual income for an earning member with dependents, adjusted for existing net worth (a household with Rs.2,00,00,000, or 2 crore, of net worth needs less life cover than a household with Rs.20,00,000, or 20 lakh). The net-worth number drives the adequacy check.

Asset allocation rebalancing

The percentage of total assets sitting in market-linked instruments versus retirement and real estate becomes visible only when the worksheet is filled. Households often discover that the equity allocation they thought they had is materially smaller because real estate dominates. The annual review is the moment to re-allocate the next year’s flows.

Debt acceleration decisions

Households at moderate net worth with a remaining home-loan principal of Rs.25,00,000 to Rs.40,00,000 (25 to 40 lakh) and surplus monthly cash flow can use the worksheet to evaluate a part-prepayment versus a fresh equity SIP. The decision depends on the loan rate, the expected equity return, and the household’s risk appetite; the worksheet provides the numbers.

FAQ

Should I include my parents’ jointly held property in my net worth?

List only the share that has been legally partitioned or that the family has explicitly agreed upon in writing. Properties in undivided estate or with ongoing succession should be carried at zero or with an explicit footnote, not at the full optimistic market value, until the legal share is clear. Mixing the household’s own assets with disputed inheritance produces misleading numbers.

Do I count the value of my term insurance in my net worth?

No. Pure-term life insurance has no surrender value and is a protection instrument, not an asset. Only the surrender value of endowment, money-back, or whole-life policies, and the fund value of ULIPs, belong on the asset side. The term-plan sum assured matters for the family’s protection plan, computed separately from net worth.

How do I value gold jewellery for the net-worth calculation?

Take the weight of pure gold (after deducting stones and impurities) from the original invoice or a fresh assessment by a hallmarked jeweller. Multiply by 85 to 90 percent of the current IBJA per-gram rate to account for the making-charge differential that does not recover on resale. The result approximates the realistic resale value, which is the correct net-worth measure.

Is EPF really my asset if I cannot withdraw it until 58?

Yes. EPF is real money credited to the member’s account and earning interest annually. The restricted access affects liquidity, not value. The cleanest treatment is to list EPF at full statement value on the total-net-worth line and exclude it from the liquid-net-worth line. Both numbers are useful for different decisions.

How often should I update the net-worth worksheet?

Once a year is enough for most salaried households, ideally in April after the previous financial year closes. Quarterly updates add noise without adding insight, because most retirement assets and real estate move slowly. The annual rhythm captures the meaningful changes (a raise, a part-prepayment, a major investment, a property purchase or sale) and avoids the temptation to react to monthly market movements.

Related guides on this topic are coming to learnfinedge.com soon.