Most Indian credit card statements quietly highlight a single number: the minimum amount due. Pay just that, the card stays active, the account stays current, and no late marker hits the credit bureau. What the statement does not say in equal-sized type is the math behind the credit card minimum payment trap india: an effective APR of 36% to 42% on the rolled-over balance and a payoff horizon that stretches into decades for even moderate balances.

This guide walks through the math step by step using a real-world Rs. 50,000 balance, shows the five-year and full-payoff cost of paying only the minimum, and ends with smart partial-pay strategies that protect the credit score without donating the household budget to revolving interest. The aim is to make the numbers concrete enough that the next statement gets a different kind of attention.

What the Credit Card Minimum Payment Trap India Really Means

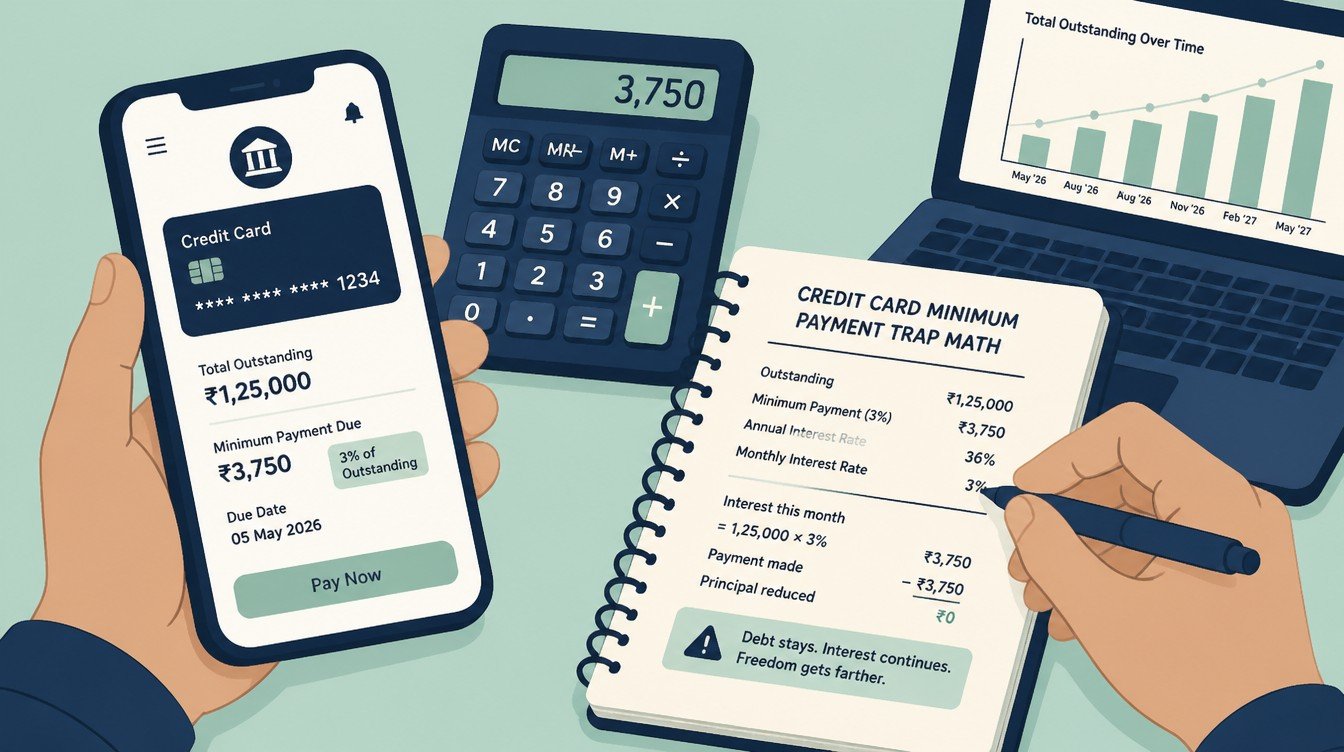

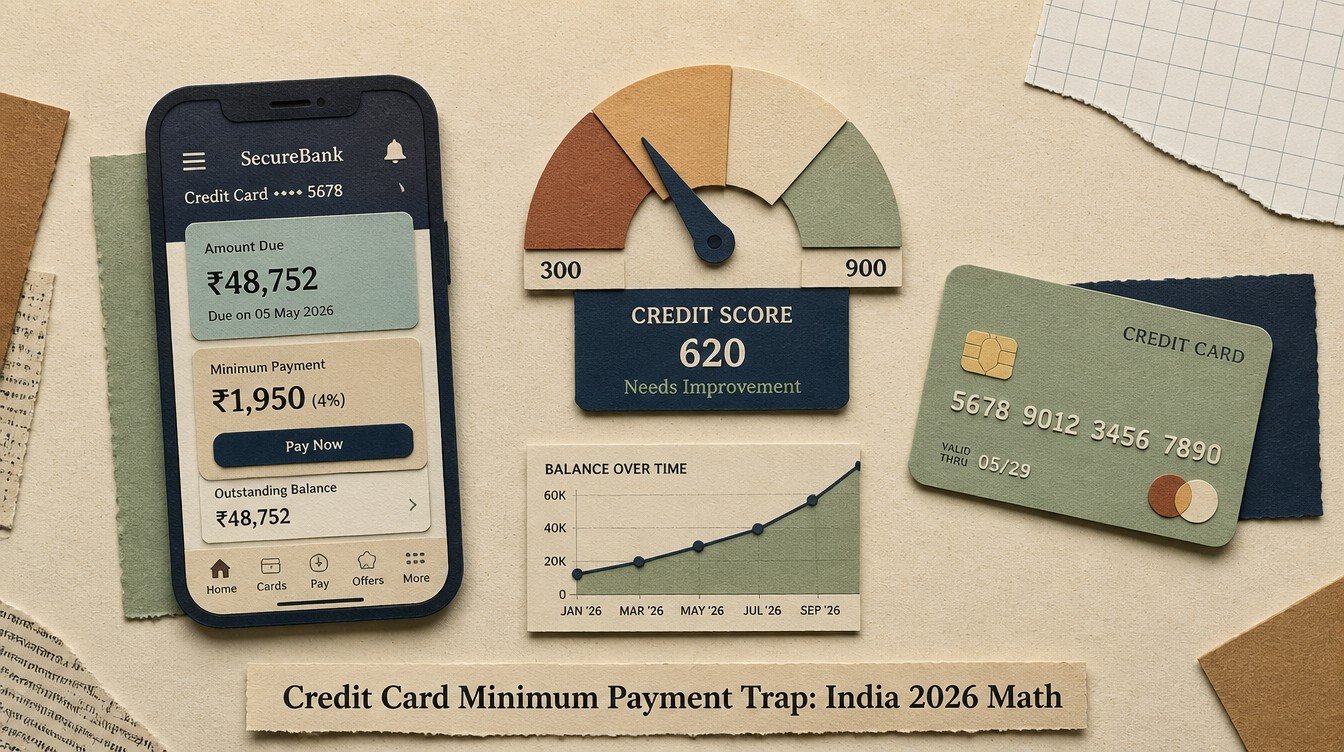

The minimum amount due (MAD) on an Indian credit card is usually computed as the higher of a flat amount (often Rs. 100 to Rs. 500) or a percentage of the total outstanding balance. The percentage is set by the issuer and typically falls between 5% and 10% of the statement balance, including any equated monthly instalments (EMIs) that have come due in that cycle.

The math the issuer uses is simple. The math the cardholder absorbs is not.

How the 5% rule plays out

A balance of Rs. 50,000 with a 5% MAD generates a minimum payment of Rs. 2,500 in the first month. After that payment, the outstanding principal is Rs. 47,500 plus accrued interest on the original Rs. 50,000. The next month’s MAD is again 5% of the new statement balance. The percentage stays constant, but the absolute rupees fall slowly because the balance is barely moving.

Why MAD does not equal “no interest”

Paying the MAD prevents a late fee and a 30-day-past-due marker on your CIBIL report, but it does not stop interest. The entire unpaid balance, including the portion of the original statement amount not cleared, attracts finance charges from the transaction date until full repayment.

The interest-free grace period collapses

The 20 to 50 day grace period that comes with a credit card disappears the moment a balance is revolved. Any new transaction made after the statement on which MAD was paid begins to accrue interest from day one. This is the part most cardholders underestimate.

What MAD does protect

It keeps the credit bureau report clean of late markers, preserves the credit limit, and avoids a one-time late payment fee of Rs. 400 to Rs. 1,300 depending on the slab. Those are real benefits. They simply come at a steep price when used as a long-term strategy rather than a one-off bridge.

The 36% to 42% APR engine running beneath the surface

Indian credit card issuers in 2026 typically quote monthly interest rates between 3.00% and 3.75%, which translates to an annualised 36% to 45% when compounded. Some premium cards advertise slightly lower rates; some entry-level co-branded cards run higher. The benchmark to keep in mind is around 3.5% per month, or 42% per year.

This rate applies daily on the average daily balance, not monthly on the statement balance. Once interest starts accruing, every additional day on the rolled-over balance compounds.

Why daily compounding matters

If a Rs. 50,000 transaction is made on the 1st and the statement is generated on the 15th, the issuer computes interest on Rs. 50,000 for 14 days. If only the MAD is paid on the due date, the issuer continues to compute daily interest on the unpaid balance from the original transaction date forward. The clock does not reset on the due date; it started on the day the transaction was made.

The retroactive interest twist

Once a balance is revolved, interest applies retroactively from the transaction date, not from the due date. A Rs. 30,000 purchase from the 3rd of the month, partially paid on the 20th, attracts interest from the 3rd onwards, not from the 20th. This is the single feature that distinguishes credit card debt from almost any other consumer credit in India.

GST on the finance charge

Goods and Services Tax at 18% applies on the finance charge. A monthly interest of Rs. 1,500 carries an additional Rs. 270 in GST. The effective cost of borrowing is closer to 49% per year once GST is layered in.

How that compares with other Indian credit

A typical 2026 personal loan rate is 11% to 18%. A consumer-durable EMI runs 14% to 22%. A gold loan sits at 9% to 15%. Credit card revolving credit at 42% to 49% is the single most expensive widely available consumer credit instrument in India.

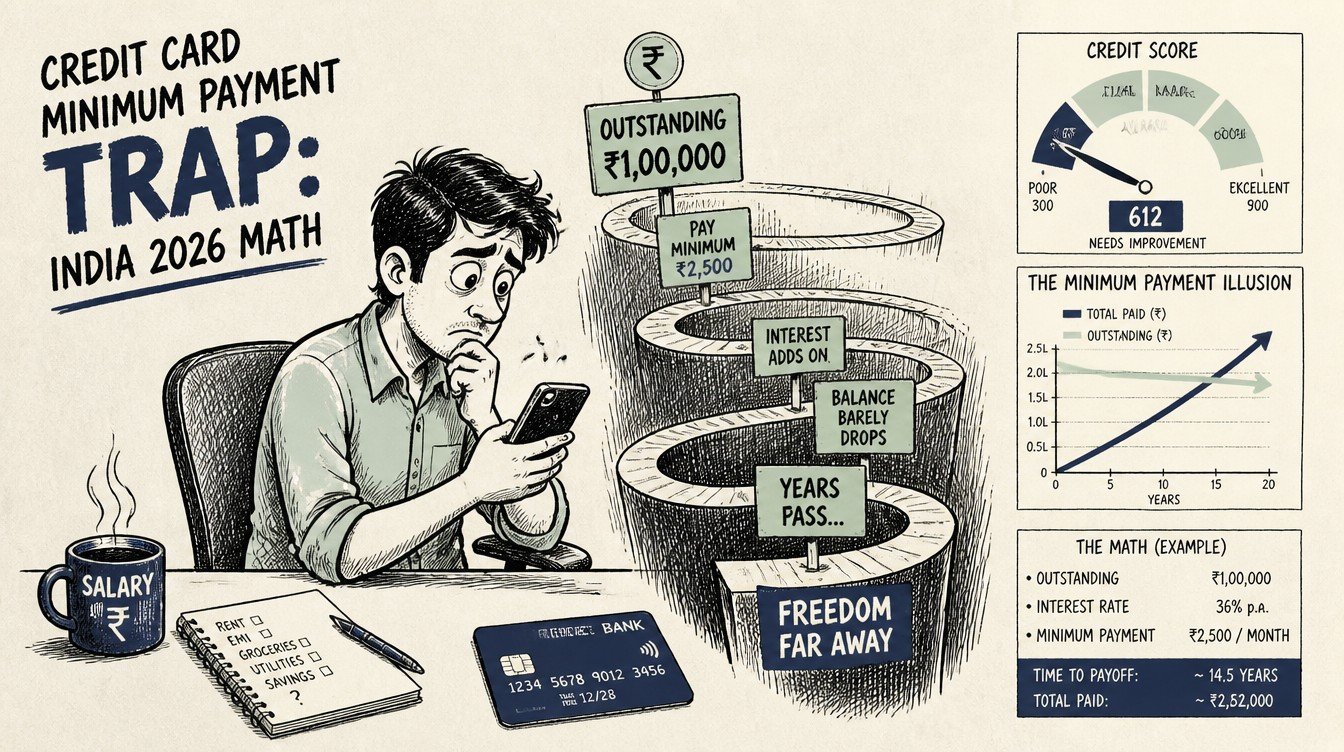

Worked example: Rs. 50,000 balance paid at the minimum for five years

Numbers convince in a way that warnings do not. The example below walks a Rs. 50,000 balance through a scenario where the cardholder pays only the minimum due each month, makes no further purchases on the card, and the issuer’s monthly interest rate is 3.5% (an APR of 42%). MAD is set at 5% of the outstanding balance, subject to a Rs. 200 floor.

| End of | Outstanding principal | Total interest paid (cumulative) | Total paid (cumulative) |

|---|---|---|---|

| Year 1 (month 12) | Rs. 41,820 | Rs. 19,540 | Rs. 27,720 |

| Year 2 (month 24) | Rs. 34,980 | Rs. 36,170 | Rs. 51,190 |

| Year 3 (month 36) | Rs. 29,260 | Rs. 50,210 | Rs. 70,950 |

| Year 4 (month 48) | Rs. 24,470 | Rs. 62,090 | Rs. 87,620 |

| Year 5 (month 60) | Rs. 20,470 | Rs. 72,160 | Rs. 1,01,690 |

After five full years of disciplined minimum payments and zero new spending, the principal is still above Rs. 20,000, more interest has been paid than the original purchase price, and the household has handed over more than Rs. 1,01,000 on a Rs. 50,000 balance. Numbers are rounded and ignore GST; including GST pushes the total outflow closer to Rs. 1,15,000.

How long until the balance hits zero?

At MAD-only payments, the same Rs. 50,000 takes roughly 16 to 19 years to fully clear, depending on the issuer’s floor amount. By that point, the total interest and GST paid is more than twice the original principal.

What changes if the rate is 3% per month instead

A monthly rate of 3.00% (an APR of about 36%) trims the total cost by roughly 12% to 15%. The trajectory is still ugly: more than Rs. 80,000 in cumulative payments over five years on a Rs. 50,000 balance, with the principal still over Rs. 17,000.

What changes if the cardholder keeps spending

The scenario above assumes no new purchases. In practice, most cardholders keep using the card. Each new transaction begins accruing interest from day one because the grace period is gone. The payoff horizon stretches further, often indefinitely.

Rollover finance charges, late fees, and the GST stack

The MAD trap is not built from interest alone. Three other line items pile on whenever a balance is partially carried or a payment is missed.

Rollover finance charge

This is the daily interest on the unpaid balance, computed from the transaction date. On a Rs. 50,000 rolled-over balance at 3.5% per month, the rollover charge alone is roughly Rs. 1,750 per month.

Late payment fee

If even the MAD is missed by the due date, a flat late fee applies. The slabs vary by issuer but typically run from Rs. 400 for balances below Rs. 10,000 to Rs. 1,300 for balances above Rs. 50,000. This fee is in addition to the interest charge.

GST on every fee and finance charge

An 18% GST sits on top of every finance charge, late fee, annual fee, and over-limit fee. The line item is often invisible in the headline statement total but appears once the statement is opened.

Over-limit fee

If a transaction pushes the balance above the credit limit, an over-limit fee of Rs. 500 to Rs. 700 plus GST applies. The credit bureau also sees a 100%+ utilisation snapshot, which damages the score.

How fees compound the trap

A single missed MAD payment can add a late fee, an over-limit fee, two GST line items, and an extra month of finance charges. On a Rs. 50,000 balance, one slip can cost Rs. 3,500 to Rs. 4,500 in a single statement cycle.

Smart partial-pay strategies that beat the minimum

Paying off the full balance every month is the textbook answer. When that is not possible, the next best moves are structured partial payments and a deliberate plan to retire the balance within a defined window. The goal is to cut the daily interest base as fast as possible.

Three strategies cover most household situations. Each one requires a clear decision about the priority of this card balance versus other goals in the budget.

Strategy 1: Aggressive monthly snowball

Commit to paying a fixed amount each month that is meaningfully larger than the MAD. On a Rs. 50,000 balance, paying Rs. 8,000 a month clears the entire balance in roughly nine to ten months and caps total interest at around Rs. 8,500 (including GST). Each extra rupee above the MAD compounds against future interest.

Strategy 2: One lump payment plus a closing run

If a bonus or tax refund arrives, treat it as a debt-killer for the card rather than discretionary spend. A Rs. 30,000 lump payment on the Rs. 50,000 balance cuts the remaining principal to Rs. 20,000 and clears it in three to four months of moderate payments. The interest saving versus the MAD-only path is in the order of Rs. 60,000 to Rs. 70,000 over the loan life.

Strategy 3: Convert the balance to an EMI plan

Most Indian credit card issuers offer a “balance conversion” or “EMI on outstanding” option. The balance is locked into a 6, 12, 18, or 24 month EMI at a rate that is often 13% to 18%, materially below the 36% to 42% revolving rate. A processing fee of 1% to 2% may apply. For a stuck balance with no realistic three-month payoff plan, this is usually the most cost-effective move.

Strategy 4: Replace the balance with a personal loan

A personal loan from a bank at 11% to 16% to pay off a credit card balance at 42% is straight arithmetic. The personal loan EMI is predictable, the rate is lower, and the credit utilisation on the card collapses, lifting the CIBIL score in the next reporting cycle. This works best when the personal loan is taken with a strict plan not to refill the card.

Strategy 5: Negotiate a one-time settlement only as a last resort

A negotiated one-time settlement leaves a “settled” tag on the credit bureau, which is worse for the score than “closed”. Use this route only if the household budget has no realistic path to repay even an EMI plan. If used, negotiate the tag to read “closed” in writing before parting with the funds.

Common mistakes Indian cardholders make in 2026

The minimum payment trap is rarely entered through one bad decision. It is usually a stack of small habits that compound. The list below covers the most frequent ones.

Treating MAD as the “real” bill

Many cardholders read only the minimum due line, set up an auto-pay for that amount, and never look at the full statement balance. The auto-pay protects the credit bureau but locks the household into the trap.

Using one card to pay another

A cash advance or balance transfer used to clear one card simply moves the debt to another, often at a higher rate plus a processing fee. The total revolving balance does not move.

Stacking new purchases on a revolved balance

Once a balance is revolved, every new swipe accrues interest from day one. Cardholders who do not pause spending on the card while clearing the old balance multiply their interest exposure.

Ignoring the EMI conversion option

Issuers rarely highlight the EMI conversion option proactively because the revolving rate is more profitable for them. Cardholders need to call and ask. The savings versus revolving credit are routinely 20 to 25 percentage points of APR.

Closing the card after the balance is cleared

After the hard work of paying off the balance, closing the card often shortens the credit history and reduces total available limit. Both lower the CIBIL score. Keep the card open with a small recurring spend instead.

How to protect the credit score while breaking out of the trap

Repayment alone is not enough. The CIBIL score is sensitive to utilisation snapshots and recent activity, so the way the balance is paid matters almost as much as the speed of repayment.

Bring utilisation below 30% by the next statement date

The bureau sees the statement-date balance. A lump payment a day before the statement closes can drop reported utilisation from 80% to 25% in one cycle, lifting the score even before the loan is fully clear.

Set up auto-debit for total amount due, not MAD

If the household budget allows, change the standing instruction from “Minimum Amount Due” to “Total Amount Due”. This is a single setting on most net-banking dashboards. The change permanently removes the trap risk.

Use a second card with conscious discipline

While paying down a revolved balance on Card A, route current spending through Card B and pay Card B in full each cycle. This protects the grace period on at least one card and keeps utilisation distributed.

Pull the CIBIL report after every reporting cycle

Confirm that the lender has reported the lower balance, that no late marker has slipped through, and that the utilisation snapshot reflects the new pay-down. Errors at this stage extend the score recovery unnecessarily.

Avoid new credit applications during the cleanup

Each new credit card or personal loan application is a hard inquiry. Stacking them during a balance-cleanup phase signals distress to the bureau. Hold all new applications for at least ninety days after the balance is cleared.

Step-by-step action plan to exit the trap in twelve months

The plan below is built for a salaried Indian with a Rs. 50,000 to Rs. 1,00,000 revolved balance and a net monthly take-home of at least Rs. 60,000. Adjust the numbers proportionally for other situations.

- Stop using the card with the revolved balance entirely for at least six months.

- Call the issuer and ask for the balance to be converted to an EMI plan at the lowest available rate.

- If the EMI rate offered is above 14%, compare with a personal loan from your salary-account bank for the same tenure.

- Set up auto-debit for either the EMI or the personal loan from the salary account.

- Redirect any side income, bonus, or tax refund into an additional principal prepayment.

- Pull a CIBIL report at the end of month four and month nine to confirm the utilisation has fallen and no negative marker remains.

- Once the balance is cleared, keep the card open with a single small recurring spend and pay the total amount due each month.

Budgeting alongside the plan

A working rule of thumb is to commit at least 15% of net monthly take-home to clearing the revolved balance until it is gone. Below 10%, the math rarely works in under eighteen months.

Emergency fund first or repayment first?

If there is no emergency fund at all, build a minimum buffer of one month of expenses in a savings account before going all-in on the card balance. Without a buffer, any unexpected expense forces a return to the card and undoes the progress.

Tax angle

Credit card interest is not tax-deductible for individuals. The savings from clearing the balance are pure, post-tax savings, which makes the effective return on prepayment even more attractive compared with market-linked investments at lower pre-tax yields.

Quick comparisons that put the cost in perspective

Visualising the cost of revolving credit alongside other Indian credit products is the fastest way to commit to a clean-up plan.

Credit card revolving vs personal loan

A Rs. 50,000 balance at 42% APR for two years costs roughly Rs. 23,000 in interest. The same Rs. 50,000 as a personal loan at 14% over two years costs about Rs. 7,500. The interest saving of Rs. 15,500 is essentially free money on the table.

Credit card revolving vs gold loan

A gold loan at 11% over two years on Rs. 50,000 costs about Rs. 5,800 in interest. The same balance revolved at 42% costs about Rs. 23,000. The trade-off is that gold has to be pledged, but for households with idle gold, the saving is substantial.

Credit card revolving vs overdraft against salary

Salaried overdrafts in 2026 sit in the 11% to 15% range, charged only on the drawn amount and only for the days drawn. For short-term cash crunches, an overdraft is usually a fraction of the cost of revolving credit on a card.

Credit card revolving vs prepaying a home loan

Even a borrower with an active home loan at 7.90% should never carry a credit card revolving balance at 42%. The post-tax saving from clearing card debt dominates any home loan prepayment math by a wide margin.

FAQ

Does paying the minimum amount due hurt my CIBIL score?

It does not directly add a late marker because the account stays current. It does, however, keep utilisation high, which is the second-largest input to the CIBIL score. Long-term MAD-only payment usually shows up as a stagnant or slowly declining score even without a single missed payment.

What is the typical APR on an Indian credit card in 2026?

Most issuers quote a monthly rate between 3.00% and 3.75%, which translates to an effective APR of roughly 36% to 45%. Add 18% GST on the finance charge and the all-in cost of revolving credit is closer to 42% to 53% per year.

Can I get the bank to lower the interest rate on my credit card?

Some issuers reduce the rate on request for long-tenured, high-credit-score customers, but the reduction is usually small (one or two percentage points). The bigger lever is to convert the balance into an EMI plan or refinance with a personal loan.

What happens if I miss the minimum due payment?

A late fee of Rs. 400 to Rs. 1,300 plus 18% GST is applied, interest continues to accrue, and after 30 days the missed payment is reported to CIBIL as a delinquency. One missed payment can drag a clean score by 50 to 80 points.

Is it ever rational to pay only the minimum due?

Only as a one-month bridge during a genuine cash crunch when the full balance cannot be paid. Even then, the EMI conversion option is usually a cheaper bridge than carrying the revolved balance for a single cycle.

Related guides on this topic are coming to learnfinedge.com soon.