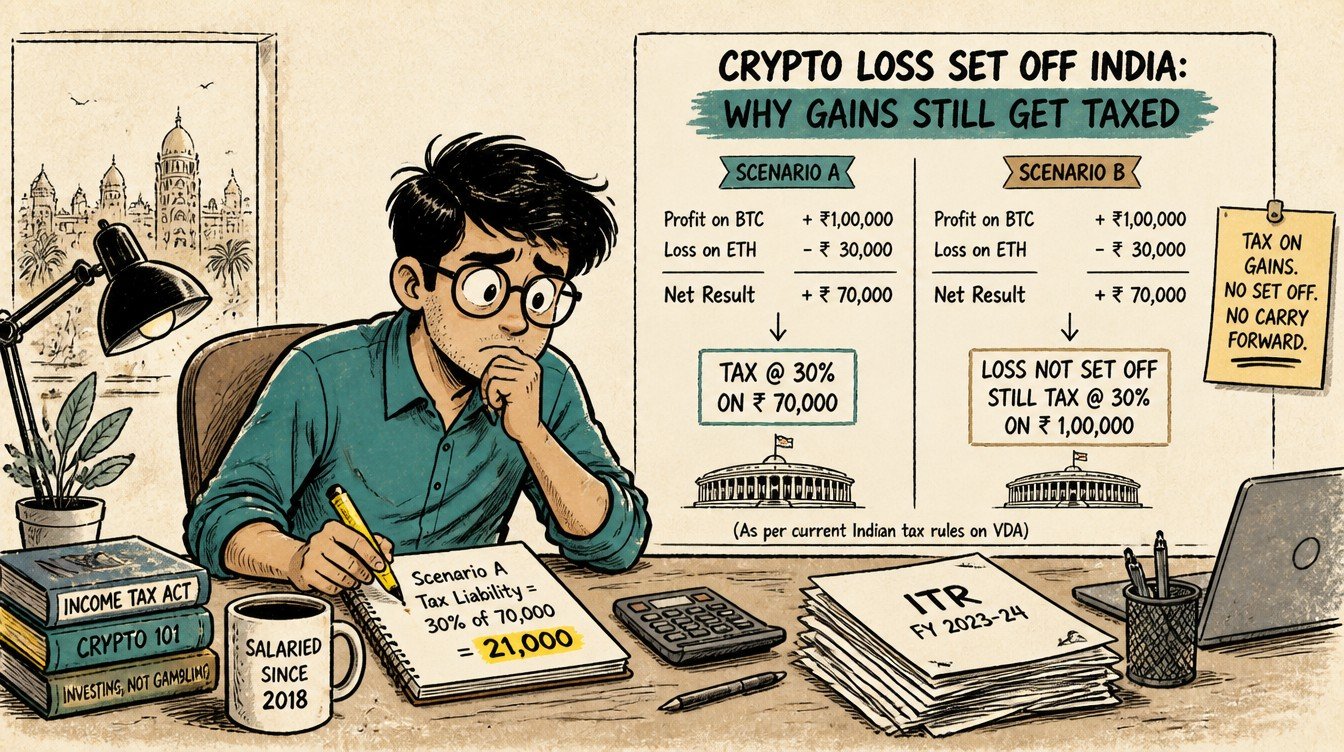

Every new crypto investor in India eventually runs into the same painful arithmetic. You make a Rs.1,00,000 profit on Bitcoin, you take a Rs.50,000 loss on Ether, you net Rs.50,000 in your bank balance, and then the Income Tax Department charges you 30% on Rs.1,00,000 anyway. That is the crypto loss set off India rule in one sentence: there is no set-off, there is no carry-forward, and the cost-of-acquisition is the only deduction the law allows.

This guide is for the investor who looked at a quarterly portfolio statement, saw a small net profit, and is now stunned by the tax notice. Section 115BBH of the Income Tax Act is unusually blunt for an Indian tax statute, and understanding why it works the way it does is the only path to filing a clean Schedule VDA. Crypto carries leveraged volatility risk; do not invest more than you can afford to lose, and do not assume the equity-market loss rules apply here.

The Statutory Language: Section 115BBH(2)

The starting point of any crypto loss set off India discussion is the bare text of the law, not a tax advisor’s summary. Section 115BBH was inserted by the Finance Act 2022 and tightened in the Income Tax Act 2025. Its second sub-section is the one that breaks set-off.

What sub-section (2) actually says

The provision states that no deduction in respect of any expenditure (other than the cost of acquisition) or allowance is allowed in computing the income from the transfer of a virtual digital asset, and that no set-off of any loss is allowed against the income computed under this section. It also prohibits the loss from being carried forward to any subsequent assessment year.

Why the language is unusually strict

Most Indian tax provisions allow at least intra-head set-off under Section 70 (loss from one source against another in the same head) and inter-head set-off under Section 71 (loss from one head against another). Section 115BBH overrides both, creating a tax silo where every profitable VDA transaction is taxed in isolation. The CBDT clarified in 2022 that even loss from one VDA cannot offset gain from another VDA.

How Budget 2026 reaffirmed it

The recodified Income Tax Act 2025, which took effect from April 1, 2026, preserved Section 115BBH(2) verbatim. Industry representations asking for parity with equity (where short-term losses can offset short-term gains) were declined again. The political signal is that the no-set-off rule is permanent for the foreseeable future.

The Worked Example That Makes It Concrete

Numbers settle arguments. Consider the textbook case the topic itself names: a Rs.1,00,000 Bitcoin gain and a Rs.50,000 Ether loss in the same financial year.

The setup

In FY 2025-26, an investor named Karthik bought Bitcoin for Rs.5,00,000 (5 lakh) in May 2025 and sold it for Rs.6,00,000 in November 2025, realising a Rs.1,00,000 gain. In the same year, he bought Ether for Rs.3,00,000 in July 2025 and sold it for Rs.2,50,000 in December 2025, taking a Rs.50,000 loss. His broker statements show a net economic profit of Rs.50,000 across the two trades.

What common sense expects

Most investors instinctively net the two figures and compute tax on the net Rs.50,000. At 30% plus 4% cess, that would yield Rs.15,600 in VDA tax. Karthik builds his cash flow expectations around this number and is content.

What Section 115BBH actually does

The law ignores the Ether loss completely. Tax is computed only on the Bitcoin gain of Rs.1,00,000. The math is: 30% of Rs.1,00,000 = Rs.30,000, plus 4% cess on Rs.30,000 = Rs.1,200, giving a total of Rs.31,200. The Ether loss of Rs.50,000 does not reduce the gain, does not carry forward, and does not offset any other income head.

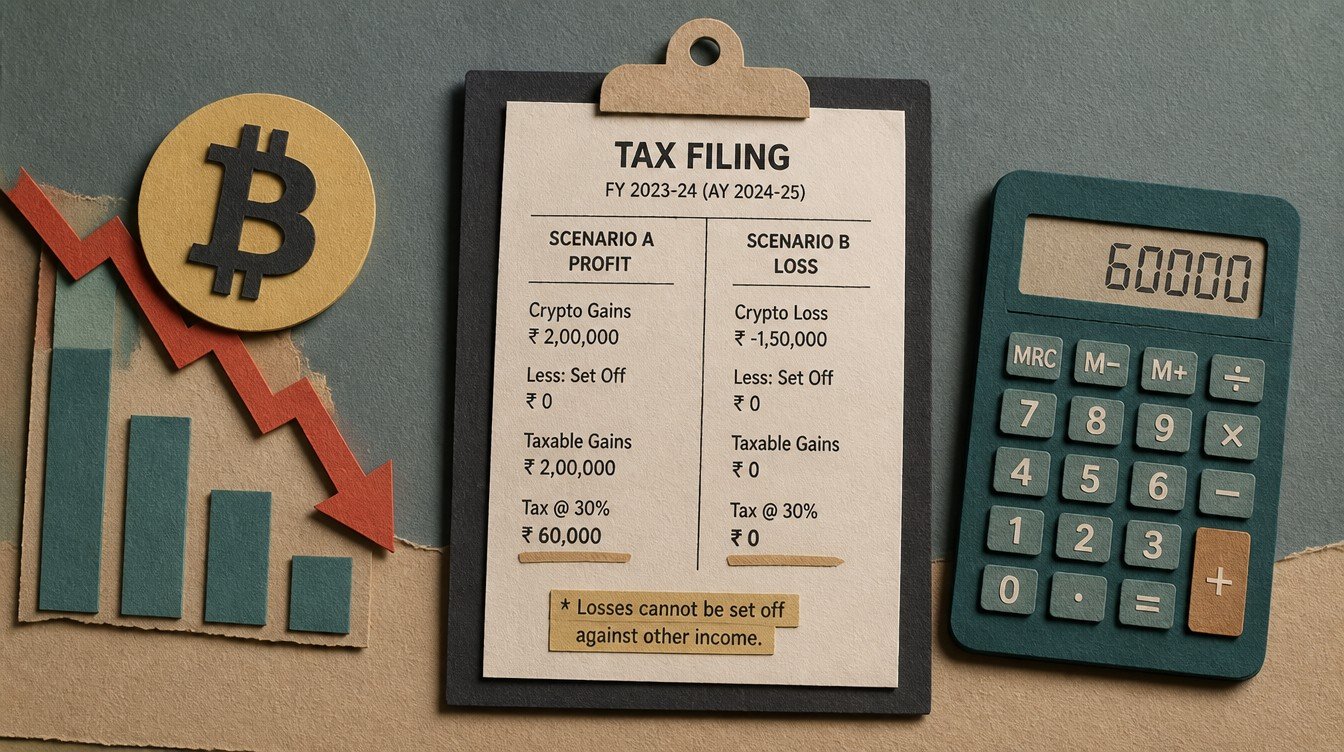

| Item | Karthik’s expectation | Section 115BBH reality |

|---|---|---|

| Net economic gain | Rs.50,000 | Rs.50,000 |

| Taxable income (VDA) | Rs.50,000 | Rs.1,00,000 |

| Tax at 30% | Rs.15,000 | Rs.30,000 |

| Cess at 4% | Rs.600 | Rs.1,200 |

| Total tax | Rs.15,600 | Rs.31,200 |

| Effective rate on net economic gain | 31.2% | 62.4% |

The takeaway

Karthik’s effective tax on his real-economy Rs.50,000 of profit is 62.4%, twice the headline 31.2%. This is not a bug in the system; it is the statute working exactly as designed. The implication for portfolio behaviour is that every losing position should be considered a “permanent” loss for tax purposes, never a tax shield.

Same-Coin Crypto Loss Set Off: Not Allowed Either

The next question every investor asks is whether two trades in the same coin can be netted. The answer is more nuanced than the headline suggests, and the nuance matters.

Multiple lots, same coin, one financial year

The CBDT’s clarifying guidance treats each transfer as a separate event, with its own cost of acquisition. If you bought Bitcoin in two tranches and sold both in the same year, you compute the gain or loss on each tranche separately. A loss on one tranche cannot offset a gain on another tranche, even though both are Bitcoin.

FIFO vs specific identification

Where multiple lots of the same coin have been acquired at different prices, the cost of acquisition for a given sale must follow the FIFO (first-in-first-out) method unless the exchange supports specific-identification matching. Most domestic exchanges default to FIFO. The choice can change the per-transaction gain or loss, but it does not break the no-set-off rule.

What this means in practice

An investor who built a Bitcoin position through 50 small DCA buys cannot blend the gains and losses across those 50 buys when selling 10 coins. Each sold lot pairs with one specific buy lot under FIFO, and each pairing is its own taxable event. Profitable lots are taxed at 30%; loss lots produce a non-deductible loss.

Cross-Coin Set-Off: Strictly Forbidden

The cross-coin case is the cleaner of the two and the rule is absolute.

The rule

A loss on Ether cannot offset a gain on Bitcoin, Solana, USDT, or any other VDA. A loss on a stablecoin trade cannot offset a gain on a major coin. A loss on an NFT cannot offset a gain on a fungible token.

Why this matters more than it sounds

Active retail traders running a basket of five to fifteen coins typically end the year with a mix of winners and losers. Under equity-market rules, the basket nets out and tax is paid only on the residual gain. Under Section 115BBH, every winner is taxed in full and every loser is irrelevant. The strategy implication is to run fewer, more deliberate positions, because adding “diversifying” trades only multiplies the asymmetric tax.

The DeFi corner case

In DeFi protocols, where a single transaction can simultaneously deposit one asset and mint another, both legs are reportable as separate transfers. A loss on the deposited asset’s deemed sale cannot offset a later gain on the minted asset’s eventual sale. Multi-leg DeFi sequences should be modelled in INR per leg before entering them.

How Crypto Set-Off Compares to Equity LTCG and STCG

The asymmetry between crypto and equity is the single most useful contrast for Indian investors trying to internalise the rule.

Equity set-off rules (Section 70, 71, 74)

Short-term capital loss on equity can offset short-term capital gain on equity, and can also offset long-term capital gain on equity. Long-term capital loss on equity can only offset long-term capital gain. Unabsorbed equity losses can be carried forward for eight assessment years and used against future capital gains.

Crypto set-off rules (Section 115BBH)

No intra-VDA set-off (across different coins or across lots of the same coin). No inter-head set-off (against salary, business income, capital gains on equity, or anything else). No carry-forward to future years. Only the cost of acquisition is deductible from the sale value.

| Feature | Equity LTCG/STCG | Crypto under 115BBH |

|---|---|---|

| Tax rate | 12.5% LTCG above Rs.1.25 lakh / 20% STCG | Flat 30% (no holding-period distinction) |

| Cost inflation indexation | Limited (only for certain assets pre-2024 rules) | Not allowed |

| Intra-head set-off | Allowed within capital gains head | Not allowed |

| Carry-forward of losses | Up to 8 years | Not allowed |

| Deductible expenses | Brokerage, STT (partial), demat charges (partial) | Only cost of acquisition |

| Holding-period treatment | STCG vs LTCG split | No distinction |

What the contrast tells investors

Equity is treated as a long-term wealth-building instrument under the IT Act, with rules that smooth out volatility through indexation, set-off, and carry-forward. Crypto is treated as a speculative gain category with none of those smoothing mechanisms. Whether one agrees with the policy or not, the design choice is consistent: every profitable VDA transaction is a discrete tax event.

Common Misunderstandings and How to Avoid Them

Across two filing seasons, chartered accountants and tax helplines have catalogued a familiar set of mistakes. Recognising them early is cheaper than fixing them in a notice response.

“My exchange portal shows a net loss for the year”

Exchange dashboards display economic P&L, which legitimately nets winners and losers. The Income Tax Act does not allow that netting. The number on the dashboard is informational; the number on Schedule VDA is the sum of profitable transactions only.

“I will adjust the loss against my salary”

Section 115BBH(2) explicitly bars inter-head set-off. A VDA loss cannot reduce salary income, business income, house property income, or any other capital gain. The bar is two-way: salary loss (if any, which is rare) cannot reduce VDA gain either.

“The loss will carry forward to next year”

It will not. Even if you incurred a Rs.5,00,000 loss on a single token in FY 2025-26, that loss is permanently lost for tax purposes. You cannot use it against a Rs.5,00,000 gain on the same token in FY 2026-27. The 30% applies in full to the next year’s gain.

“I will reclassify trading as business income to claim expenses”

The argument is sometimes made that high-frequency trading should fall under Section 28 (business income) rather than Section 45 (capital gains), allowing trading expenses. Section 115BBH overrides both, however. Income from the transfer of VDA is taxed at 30% irrespective of whether classified as business or capital gains, and the expense deduction remains limited to the cost of acquisition.

Portfolio Construction Implications

The tax rule changes what a rational portfolio looks like. Several adaptations have become standard practice among Indian retail crypto investors who file cleanly.

Fewer, larger, longer-held positions

Because every trade is taxed without netting, churn is doubly expensive: once in fees, once in tax. Investors who hold a small number of conviction positions for longer pay less tax than equally-skilled traders who rotate.

Avoid taking small losses to “cycle” capital

A common equity habit is to sell a losing position, book the loss for set-off, and rotate into another instrument. That habit destroys value in crypto, because the booked loss is non-deductible. The rational move is either to hold the losing position until conviction returns or to exit it as part of a planned reduction, not as a tax move.

Track cost of acquisition obsessively

Cost is the only deduction the law allows, so accurate cost-basis records are the only lever left. For crypto-to-crypto swaps, the cost of the newly acquired token is the INR-equivalent fair market value of the token given up at the swap timestamp. Maintain that ledger in real time, not at year-end, because exchange records sometimes lose granularity beyond 12 months.

Step-by-Step: Filing With Losses in Schedule VDA

Even though losses do not reduce tax, they still need to be disclosed correctly in Schedule VDA. Under-reporting losses creates the same AIS mismatch as under-reporting gains.

- List every transfer of every VDA during FY 2025-26, including losing trades, swaps, and gifts.

- For each row, fill date of acquisition, date of transfer, cost of acquisition, consideration received, and the resulting gain or loss.

- For loss rows, fill the loss figure but expect the schedule to compute zero set-off; do not try to net it against another row.

- Compute total income from VDA as the sum of positive-gain rows only.

- Apply the flat 30% to the total, add 4% cess, add surcharge if total income crosses the surcharge threshold.

- Claim the 1% TDS deducted under Section 194S as a credit in Schedule TDS.

- Reconcile the final Schedule VDA total against the AIS summary before submitting.

Advanced: When the No-Set-Off Rule Hurts the Most

The rule bites unevenly. Certain investor profiles feel the pain more than others, and recognising the pattern helps frame allocation decisions.

The active “10-coin basket” trader

An investor running a diversified basket of ten coins, taking moderate profits on three and moderate losses on seven, may end the year with a small net economic gain but a large taxable gain. This is the worst-case profile for the no-set-off rule and the strongest argument for concentrating exposure.

The arbitrage trader

Cross-exchange arbitrage often involves dozens of small offsetting trades that net to a thin margin. The 30% applies on every profitable leg independently, while losing legs offer no relief. Most arbitrage strategies become uneconomic after the 30% and 1% TDS stack.

The accidental NFT collector

NFT collectors who buy ten pieces and sell three at a gain, while six become illiquid and one is sold at a loss, face full 30% tax on the three winners with no offset from the loser. Illiquid pieces sit on the balance sheet at cost until they are actually sold.

The Bottom Line on Crypto Loss Set-Off in India

The crypto loss set off India rule is one of the strictest provisions in the Income Tax Act, and it is unlikely to soften before Budget 2027 at the earliest. The pragmatic response is to design a portfolio that minimises the asymmetric drag.

Three principles for the disciplined investor

First, treat every trade as taxed at 30% on the gain leg with no relief on the loss leg, and size positions accordingly. Second, hold conviction positions for longer to delay the 30% event and to avoid generating booked losses that cannot be used. Third, file Schedule VDA row by row, disclosing every trade, because the new April 1, 2026 exchange-reporting framework removes any benefit from selective omission.

One final reality check

Crypto carries leveraged volatility risk; do not invest more than you can afford to lose. Layer on the no-set-off rule, the 1% TDS, the 30% flat rate, and the exchange-reporting regime, and crypto becomes an asset class to size conservatively, document obsessively, and report transparently.

Frequently Asked Questions

Can I offset my crypto losses against crypto gains in the same year?

No. Section 115BBH(2) explicitly bars set-off of any loss against income from the transfer of a virtual digital asset. A Rs.50,000 loss on Ether cannot offset a Rs.1,00,000 gain on Bitcoin, even if both occur in the same financial year and on the same exchange.

Can I carry forward a crypto loss to next year?

No. Section 115BBH bars carry-forward as well. A loss incurred in FY 2025-26 cannot be used against any gain in FY 2026-27 or any subsequent year. The loss is permanently extinguished for tax purposes.

Can I claim my crypto loss against my salary or business income?

No. The provision overrides both Section 70 (intra-head set-off) and Section 71 (inter-head set-off). A crypto loss cannot reduce salary, business income, house property income, or capital gains on equity. The bar is comprehensive.

Is the no set-off rule the same for NFTs and stablecoins?

Yes. Any asset that meets the CBDT-notified VDA definition, including NFTs, stablecoins, and most fungible tokens, falls under Section 115BBH. The no set-off rule applies uniformly across the category. Losses on NFTs cannot offset gains on Bitcoin and vice versa.

How is crypto set-off different from equity capital-loss rules?

Equity capital losses under Section 74 can offset capital gains of the same type and can be carried forward for up to eight years. Crypto losses under Section 115BBH cannot be set off against anything and cannot be carried forward. The two regimes are intentionally different and have remained so through Budget 2026.

Related LearnFineEdge guides on Section 115BBH math, Schedule VDA filing, and the April 2026 exchange-reporting rule are forthcoming and will be linked here as the cluster goes live.