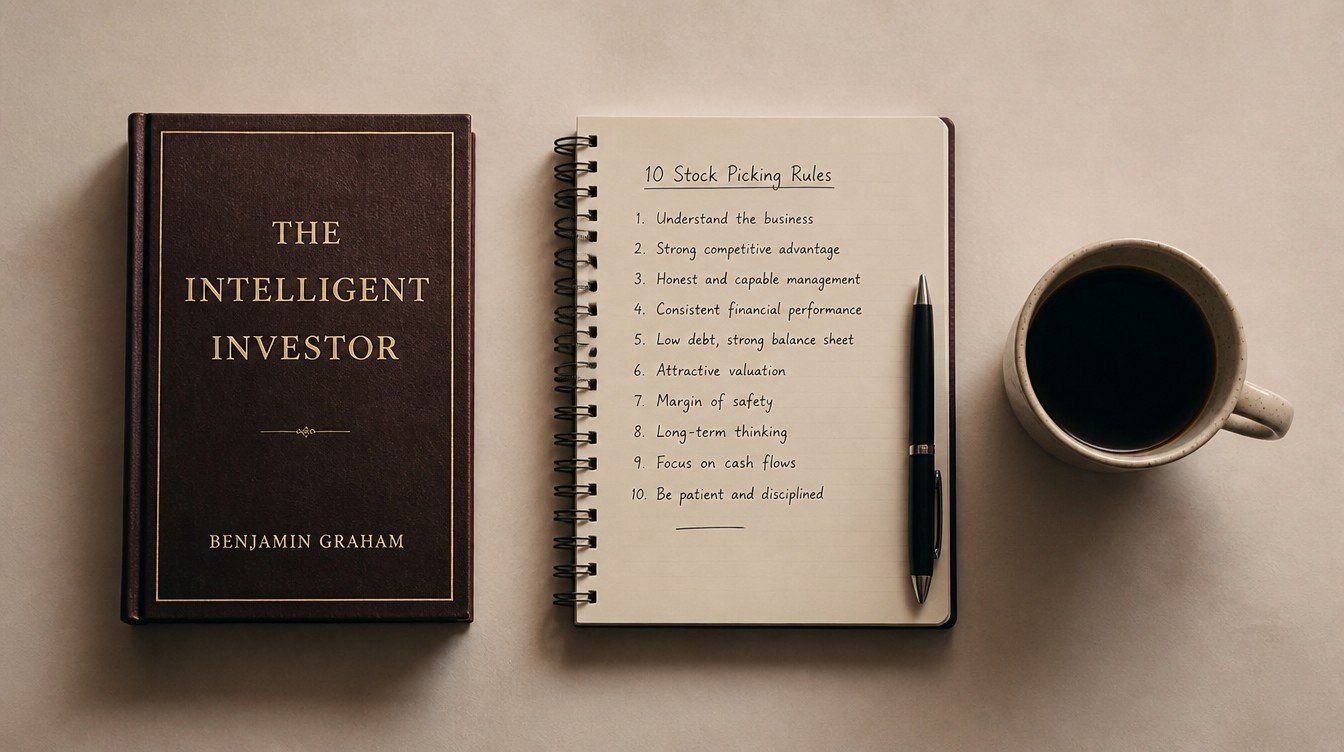

Warren Buffett’s 10 Rules for Picking Stocks: A Practical Guide for Indian Investors

Warren Buffett has never published a formal stock-picking checklist. But across 60 years of shareholder letters, interviews, and publicly documented investment decisions, a consistent set of Warren Buffett stock-picking rules has emerged that serious students of his method can reconstruct and apply. This article distils those rules into practical criteria, illustrated with examples from Indian markets, so that investors working with NSE and BSE stocks can apply the same framework that Buffett uses at Berkshire Hathaway.

Rule 1: Only Buy Businesses You Understand

Buffett’s first and most fundamental rule is the circle of competence principle: never invest in a business whose economics you cannot explain clearly to a reasonably intelligent teenager. If you can’t explain in two or three sentences what the business does, how it makes money, and why customers choose it over competitors, you don’t understand it well enough to own it.

Applied to Indian markets: an investor who uses Pidilite adhesives regularly, understands why Fevicol dominates the carpenter segment, and can articulate why a new entrant cannot easily dislodge it has a genuine understanding of the business. An investor who buys a specialty chemicals company because it appeared in a screener’s top performers list does not, regardless of how much of the annual report they have read. The circle of competence framework explains how to test whether your understanding is genuine.

Rule 2: Demand a Durable Competitive Advantage

Buffett looks for businesses with what he calls an “economic moat” – a structural advantage that protects the business from competitors over long periods. The moat must be durable, not just current. A business that is profitable today because it has the lowest cost or the best product currently is not a moat business unless that advantage is protected by something structural: brand loyalty, switching costs, network effects, regulatory protection, or cost advantages that are genuinely difficult to replicate.

In India, strong moat businesses include HDFC Bank (two decades of superior asset quality and operational discipline that competitors have consistently failed to match), Asian Paints (distribution depth in 80,000+ outlets that took 30 years to build), and Bajaj Finance (risk management infrastructure in consumer lending that represents a decade of learning). A well-funded competitor cannot replicate these structural moats in two or three years.

Rule 3: Insist on Management with Integrity

Buffett has said he looks for honest managers who are passionate about their businesses and act in shareholders’ interests. He has described integrity as more important than intelligence in management assessment a brilliant manager without integrity will use their intelligence against shareholders. His preferred managers are those who treat minority shareholders as partners, not as a necessary nuisance.

For Indian investors, management integrity assessment requires examining promoter pledging levels (high pledging signals financial stress and potential misalignment), related-party transaction patterns (are transactions with promoter-owned entities at arm’s-length prices?), and the history of minority shareholder treatment through capital allocation decisions. Buffett would pass on a business with excellent economics if the management had demonstrated a willingness to extract value from minority shareholders through any of these mechanisms.

Rule 4: Buy at a Sensible Price

Buffett is explicit that he will not overpay for even the best business. His concept of intrinsic value – the present value of all future cash flows that the business will generate – is the anchor for every investment decision. He buys when the market price is meaningfully below his intrinsic value estimate, which provides a margin of safety: if his estimate is wrong, the gap between price and value cushions the error.

His rough practical rule for growth businesses: do not pay more than a PE ratio that is twice the business’s long-term earnings growth rate. A business that grows earnings at 15% annually is fairly valued at approximately 30 times earnings. At 45x or 50x, the investor is making a bet on continued growth acceleration, which requires perfect execution and benign market conditions conditions that rarely persist.

Rule 5: Think in Long-Time Horizons

Buffett’s famous line is that his preferred holding period is “forever.” He means this literally for businesses where the economics remain excellent over time Coca-Cola, American Express, and Apple have all held their positions for decades. He argues that the compounding mathematics of great businesses, which are run by excellent management, only become fully visible over very long periods. Selling a genuinely exceptional business because it has returned 5x in three years is one of the most expensive mistakes a long-term investor can make.

Applied to Indian markets: an investor who bought Asian Paints or HDFC Bank in 2000 and held to 2025 earned returns that dwarf any strategy involving switching between stocks based on shorter-term valuation or momentum signals. The compounding of earnings per share in genuinely exceptional businesses does most of the work. The mathematics of long-term compounding are most powerful when applied to businesses with consistently high returns on equity.

Rule 6: Concentrate in Your Best Ideas

Buffett has said that diversification is protection against ignorance useful for investors who do not know what they own. Investors who do know what they own, who have genuinely high conviction in a small number of businesses, should concentrate their capital on those ideas. His view: if you have 30 ideas in your portfolio, your 30th idea is almost certainly worse than your first idea. Holding it is a drag on returns, not a risk management tool.

Throughout its history, Berkshire has concentrated its listed equity portfolio. At various points, 5-6 stocks represented 80% of the portfolio’s value. Buffett has described this approach as intellectual honesty you are allocating capital to your best ideas in proportion to your conviction, rather than spreading it thinly to avoid being wrong in any single position.

Rule 7: Ignore the Market’s Short-Term Noise

Buffett describes Mr. Market Benjamin Graham’s metaphor for the stock market as a manic-depressive business partner who quotes a buy or sell price every day. Some days Mr. Market is euphoric and quotes prices far above intrinsic value. Other days he is despairing and quotes prices far below it. The intelligent investor uses these quotes opportunistically buying when Mr. Market is depressed and ignoring him otherwise rather than treating market price movements as information about business value.

This rule has direct application to how Indian retail investors respond to market corrections. Buffett’s view, consistent throughout his career, is that a 20-30% market correction is not a warning sign – it is a buying opportunity. The investors who generate long-term wealth are those who add to great businesses during corrections rather than selling in panic. Loss aversion and recency bias are the cognitive obstacles that prevent most investors from applying this rule effectively.

Rule 8: Never Use Leverage in Long-Term Equity Investing

Buffett has made this point emphatically across multiple decades of shareholder letters. Leverage – borrowed money used to amplify investment returns – introduces the risk of forced selling at the worst possible time. A leveraged investor who faces a margin call during a market downturn must sell their positions regardless of whether selling is strategically sensible. This transforms a temporary paper loss into a permanent capital loss.

His insurance businesses at Berkshire provide what he describes as “free float” – premium income that they hold before claims are paid and that functions as low-cost leverage. But this type of leverage is structural, not discretionary leverage, and it is matched against a portfolio of businesses Berkshire owns entirely or controls, not against listed equity positions that can be called against in a downturn. The lesson for individual investors is straightforward: equity investing with borrowed money – margin accounts, pledged shares, and personal loans invested in equities – introduces a category of risk that makes long-term compounding impossible.

Rule 9: Reinvest in the Business When Returns Are High

Buffett distinguishes sharply between businesses that can reinvest their earnings at high rates of return and those that cannot. A business earning a 25% return on equity that can reinvest all its earnings into projects earning 25% is worth far more than a business earning a 25% ROE that must return all its earnings to shareholders because it has no high-return reinvestment opportunities. The former compounds intrinsic value at 25% annually; the latter depends on the investor’s ability to find equivalent reinvestment opportunities elsewhere.

This is why Buffett has historically preferred businesses with high reinvestment rates over those that pay high dividends. Businesses like Bajaj Finance in India that can grow their loan book at 25-30% annually with high ROE are compounding machines their intrinsic value grows at roughly the rate they earn on retained capital. Businesses in mature, slow-growth industries that generate cash but have no high-return reinvestment options should return that cash to shareholders rather than destroying value through low-return capital expenditure or acquisitions.

Rule 10: Know When to Sell and When Not To

Buffett’s sell discipline is as instructive as his buy discipline. He sells for three reasons: the business fundamentals have deteriorated permanently; a significantly better use of the capital has been identified; or he made an error in the original thesis and the business was never as good as he believed. He does not sell because the stock has risen significantly, because the PE multiple seems high, or because macroeconomic conditions are uncertain.

The practical implication: investors should have a written thesis for each holding that specifies the conditions under which the thesis would be invalidated. If those conditions arise the moat is genuinely eroded, management has demonstrated dishonesty, and the total addressable market has structurally shrunk that is the moment to sell, regardless of the price. If those conditions have not arisen, holding is almost always the right answer. Buffett’s complete investment framework treats premature selling as one of the most reliably value-destructive investor behaviors.

Applying the 10 Rules as a Unified Framework

These ten rules are not independent criteria – they form an integrated framework in which each rule reinforces the others. Rule 1 (understand the business) enables Rule 2 (assess the moat), which enables Rule 3 (evaluate management), and then enables Rule 4 (price correctly). Rule 5 (long time horizon) only works if Rules 1-3 are applied correctly you can only hold a business for a decade with confidence if your original understanding was deep and honest.

For Indian investors applying this framework in 2026, the starting point is brutal self-assessment: for each current holding, can you satisfy all ten rules? Most investors will find they hold some positions that fail Rule 1 (bought on a tip without genuine understanding), some that fail Rule 3 (management quality was never seriously examined), and some that fail Rule 4 (bought during a momentum phase at prices that embedded growth assumptions that haven’t materialized). The framework serves as a diagnostic tool for the existing portfolio before investors use it as a screen for new investments. Building the kind of portfolio that generates financial independence requires exactly this kind of honest portfolio-level analysis as a foundation.

Frequently Asked Questions

What are Warren Buffett’s main stock-picking rules?

Buffett’s core stock picking rules are: understand the business completely, insist on a durable competitive moat, require management integrity, buy at a sensible price below intrinsic value, hold for very long periods, concentrate capital in your best ideas, ignore short-term market noise, avoid leverage, prefer high-reinvestment-rate businesses, and sell only when the fundamental thesis is broken rather than when prices rise.

How does Buffett find stocks to invest in?

Buffett reads extensively annual reports, industry publications, competitor filings and has built up knowledge over decades that allows him to recognize businesses with durable competitive advantages when he encounters them. He does not use screens or algorithmic filters as primary tools. His process is qualitative first: Does this business have the characteristics of a remarkable business? Then quantitatively, does the current price offer a margin of safety against intrinsic value?

What PE ratio does Warren Buffett prefer?

Buffett does not use a fixed PE target. His principle is that the PE should be reasonable relative to the business’s long-term earnings growth rate and the quality of its competitive position. As a rough guideline derived from his investment history, he tends to avoid businesses trading above 30-40x earnings unless the earnings growth rate is meaningfully above 15% and the competitive moat is exceptionally strong. He has paid higher multiples for genuinely exceptional businesses but regards high-PE investing as requiring a much higher margin of certainty about future growth.

Does Buffett’s method work for small-cap Indian stocks?

The framework applies directly to Indian small-caps, with additional emphasis on management integrity screening. Small-cap Indian businesses frequently fail Rule 3 – promoter pledging, related-party transactions, and opaque accounting are more common in this segment. Buffett’s framework would concentrate on the small-cap businesses that pass all ten rules, accepting that the list will be shorter than a screen-based approach would suggest and that the quality premium is worth paying for the governance certainty it provides.

What is Buffett’s biggest investment mistake?

Buffett has publicly described his acquisition of Berkshire Hathaway’s original textile operations as his most expensive mistake not because he paid too much, but because he kept the business running long after it was clear that the economics were structurally impaired. He estimates that the opportunity cost of the capital tied up in textiles over the years it operated was enormous. The lesson he draws: even at a low price, a bad business will destroy more value over time than the discount saves at entry.

Related Articles

- Warren Buffett Investment Strategy: The Complete Value Investing Guide for India

- Warren Buffett Circle of Competence: Know Before You Invest

- Charlie Munger Mental Models: 25 Thinking Tools Every Indian Investor Needs